Understanding Workers’ Compensation Insurance: A Vital Protection for Employers and Employees

As a business owner, ensuring the safety and well-being of your employees is one of your top priorities. However, accidents happen, and when they do, workers’ compensation insurance is there to help protect both you and your employees. Whether it’s a minor injury or something more serious, this type of insurance provides financial support during the recovery process.

In this article, we will explore workers’ compensation insurance, what it covers, why it’s essential, how it works, and how to determine if it’s required for your business. We will also answer some common questions to help clarify any doubts you may have.

:max_bytes(150000):strip_icc()/workers-compensation.asp-final-f97e35419bc74ee4b5d52b66799da153.png)

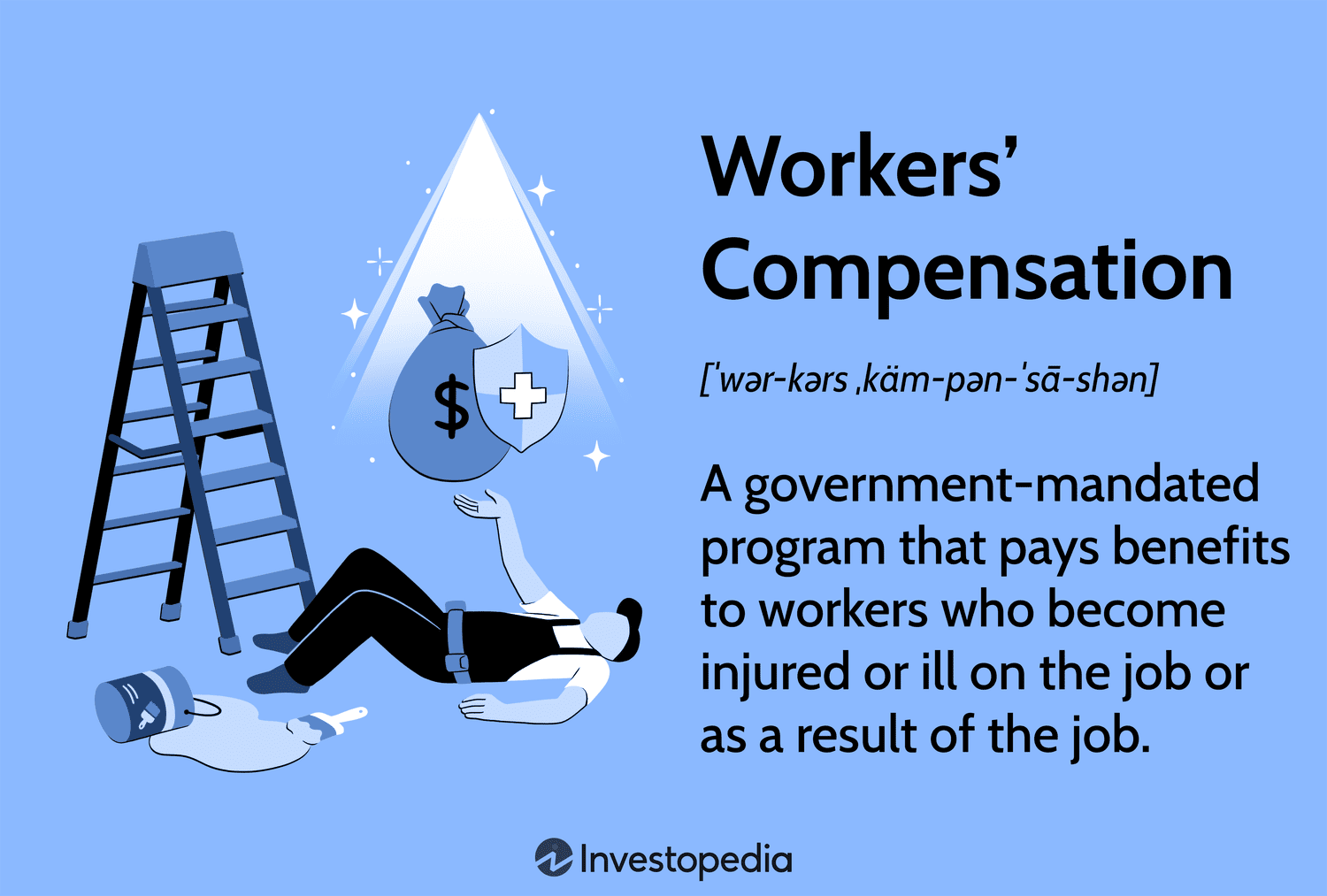

What is Workers’ Compensation Insurance?

Workers’ compensation insurance is a state-mandated program that provides financial and medical benefits to employees who suffer job-related injuries or illnesses. This insurance helps cover medical expenses, lost wages, and rehabilitation costs for employees who are hurt while performing their work duties.

At the same time, workers’ compensation insurance protects employers by reducing the likelihood of expensive lawsuits from injured employees. It’s a no-fault system, meaning the employee does not have to prove the employer was negligent to receive benefits, and the employer is generally immune from lawsuits related to workplace injuries.

Why is Workers’ Compensation Insurance Important?

1. Protects Employees

The primary benefit of workers’ compensation insurance is the financial protection it offers employees who suffer injuries or illnesses while on the job. These benefits help cover medical expenses, lost wages, and sometimes even disability benefits for employees who are unable to work due to their injuries. Without this coverage, employees could be left without support during a difficult time.

2. Shields Employers from Lawsuits

By having workers’ compensation insurance in place, employers are generally protected from lawsuits filed by injured workers. In exchange for the benefits provided through the workers’ compensation system, employees generally waive their right to sue their employer for workplace injuries. This helps reduce the risk of costly legal fees and settlements for businesses.

3. Compliance with State Laws

In most states, having workers’ compensation insurance is a legal requirement. Failure to provide this coverage can result in severe penalties, fines, and even criminal charges in some cases. Employers who comply with workers’ compensation laws ensure they meet legal obligations, avoiding legal complications.

4. Employee Satisfaction and Retention

Offering workers’ compensation insurance helps foster a positive work environment by showing employees that their safety is a priority. This can improve morale, increase productivity, and lead to higher employee retention rates. Employees are more likely to feel secure in their job if they know they are protected in case of injury or illness.

What Does Workers’ Compensation Insurance Cover?

Workers’ compensation insurance provides several types of benefits to employees who experience work-related injuries or illnesses:

1. Medical Expenses

Medical coverage is one of the most important aspects of workers’ compensation insurance. It covers the costs of medical treatment related to an injury or illness sustained at work. This includes doctor visits, hospitalization, surgeries, medications, physical therapy, and other related medical expenses.

2. Lost Wages

If an employee is unable to work due to their injury, workers’ compensation can provide wage replacement benefits. These benefits typically cover a percentage of the employee’s salary, ensuring they have financial support during their recovery.

3. Disability Benefits

If an employee is permanently or temporarily disabled due to a work-related injury, workers’ compensation insurance provides disability benefits. These benefits are categorized into:

– Temporary Total Disability (TTD): Benefits for workers who are temporarily unable to work.

– Permanent Partial Disability (PPD): Benefits for workers who experience lasting disabilities but can still work in some capacity.

– Permanent Total Disability (PTD): Benefits for workers who are permanently unable to work in any capacity.

4. Rehabilitation Costs

Workers’ compensation also covers the cost of rehabilitation services to help injured employees return to work as quickly and safely as possible. This may include vocational training, physical therapy, and other services designed to restore the employee’s ability to perform their job duties.

5. Death Benefits

In tragic cases where an employee’s injury or illness results in death, workers’ compensation provides death benefits to the employee’s family. These benefits can help cover funeral expenses and provide compensation for lost income for dependents.

How Does Workers’ Compensation Insurance Work?

The process of workers’ compensation insurance typically follows these steps:

1. Injury or Illness Occurs

An employee is injured or falls ill due to a work-related incident. In most cases, the employee must report the injury to the employer as soon as possible to ensure the claim is filed promptly.

2. Medical Treatment and Evaluation

The employee receives medical treatment for the injury. The employer or insurance company may direct the employee to specific healthcare providers for evaluation and treatment. The medical provider will assess the injury and recommend an appropriate course of treatment.

3. Filing a Claim

Once the injury has been reported, the employee or employer must file a workers’ compensation claim with the insurance provider. The insurance company will review the claim and determine if it is valid based on the details provided.

4. Compensation and Benefits

If the claim is approved, the employee will begin receiving the benefits outlined in the workers’ compensation policy. This may include coverage for medical expenses, wage replacement, disability benefits, and rehabilitation services.

5. Return to Work

Once the employee has recovered sufficiently, they can return to work. If they are unable to resume their previous duties, the workers’ compensation system may assist with vocational training or other services to help them transition into a new role.

Do You Need Workers’ Compensation Insurance?

In the majority of states, workers’ compensation insurance is a legal requirement for most businesses with employees. However, the rules vary depending on your state and the number of employees you have. Even if it’s not legally required, it’s still a wise investment to protect your employees and your business.

Some of the factors that determine whether or not you need workers’ compensation insurance include:

– Number of Employees: Some states only require workers’ compensation insurance for businesses with a certain number of employees, typically between 3-5.

– Type of Work: Certain industries with higher risks, such as construction, healthcare, and manufacturing, often have stricter requirements for workers’ compensation coverage.

– State Laws: Each state has its own laws regarding workers’ compensation insurance. Some states allow businesses to self-insure, while others require insurance through a licensed carrier.

Consequences of Not Having Workers’ Compensation Insurance

Failure to comply with workers’ compensation laws can result in significant penalties. Employers may face:

– Fines

– Legal action

– Increased insurance premiums in the future

– Potential civil lawsuits

Frequently Asked Questions (FAQs)

1. How much does workers’ compensation insurance cost?

The cost of workers’ compensation insurance varies depending on factors such as the size of your business, industry, number of employees, and the risk level of the work being performed. On average, businesses can expect to pay between $0.75 to $2.74 per $100 of payroll.

2. Does workers’ compensation insurance cover emotional distress or mental health issues?

Yes, in some cases, workers’ compensation insurance can cover mental health issues such as work-related stress, depression, or anxiety if they are caused by the work environment or a traumatic event at work. Each case is evaluated individually based on the circumstances.

3. Is workers’ compensation insurance required for independent contractors?

Typically, workers’ compensation insurance is not required for independent contractors since they are considered self-employed. However, if an independent contractor is injured while working under your direction, you may still be responsible for providing some form of compensation depending on the situation.

4. How long does workers’ compensation insurance last?

The duration of benefits depends on the severity of the injury or illness. Temporary benefits typically last until the employee is able to return to work, while permanent disability benefits may last for the rest of the employee’s life if they are permanently disabled.

Conclusion

Workers’ compensation insurance is a vital protection for both employees and employers. It ensures that employees are taken care of in the event of a work-related injury or illness while also protecting employers from costly lawsuits and legal claims. By understanding how this insurance works and the benefits it provides, you can make informed decisions that safeguard the well-being of your workforce and your business.

As a business owner, investing in workers’ compensation insurance not only helps you comply with state regulations but also fosters a supportive and safe work environment for your employees, ultimately contributing to the long-term success of your business.