Understanding Parametric Insurance: A Modern Approach to Risk Management

In today’s unpredictable world, parametric insurance has emerged as a groundbreaking solution for risk management. Unlike traditional insurance policies, parametric insurance offers pre-agreed payouts based on predefined triggers, making claims processes faster, simpler, and more efficient.

In this article, we’ll explore the concept of parametric insurance, how it works, its benefits, and why it’s rapidly gaining traction across industries.

What is Parametric Insurance?

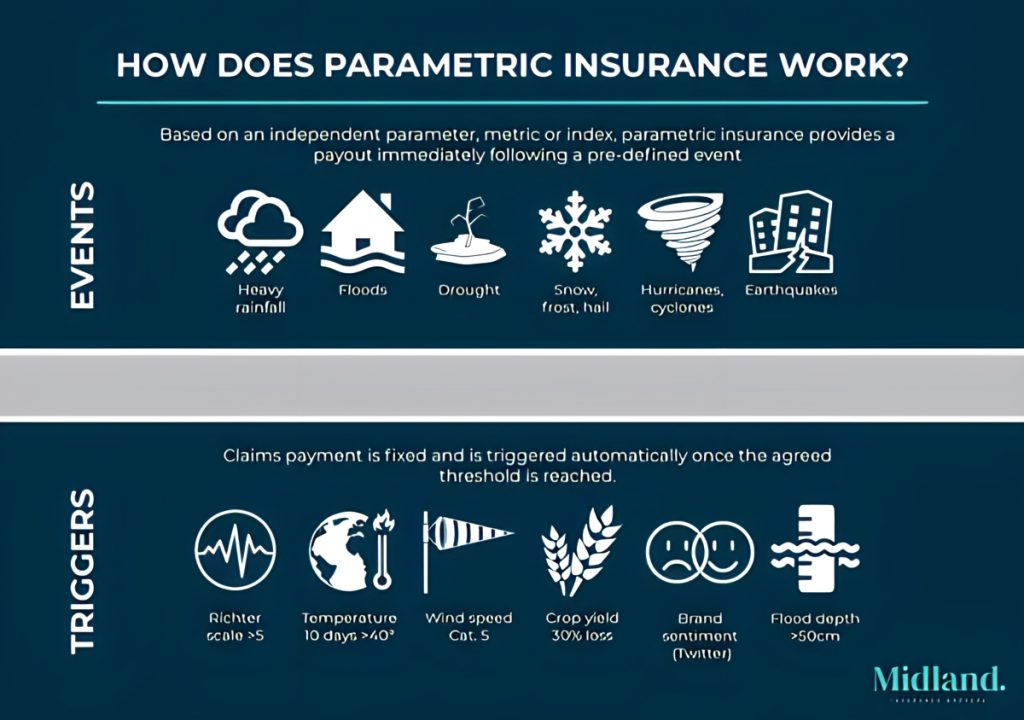

Parametric insurance is a type of insurance coverage that pays out based on a specific parameter or index trigger rather than the actual loss incurred. For example, a policy might pay if a hurricane’s wind speed exceeds a certain threshold or if rainfall falls below a defined level during a particular time.

Key Features:

- Predefined Triggers: Coverage activates based on measurable events like rainfall, temperature, or seismic activity.

- Quick Payouts: As long as the trigger conditions are met, payouts are disbursed without a lengthy claims process.

- Customizable Policies: Tailored solutions based on the insured’s unique risk exposure.

“Parametric insurance isn’t about compensating losses—it’s about providing immediate financial relief to manage risk proactively.”

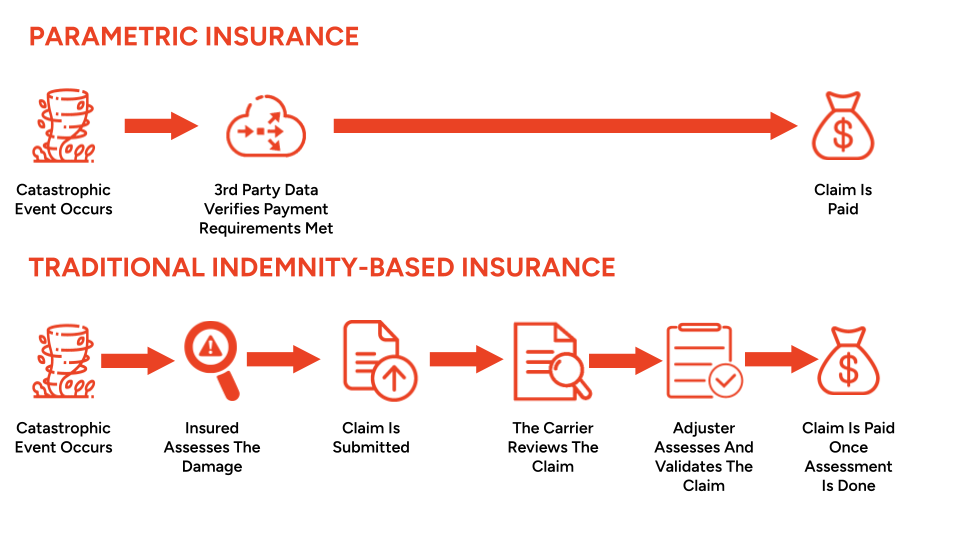

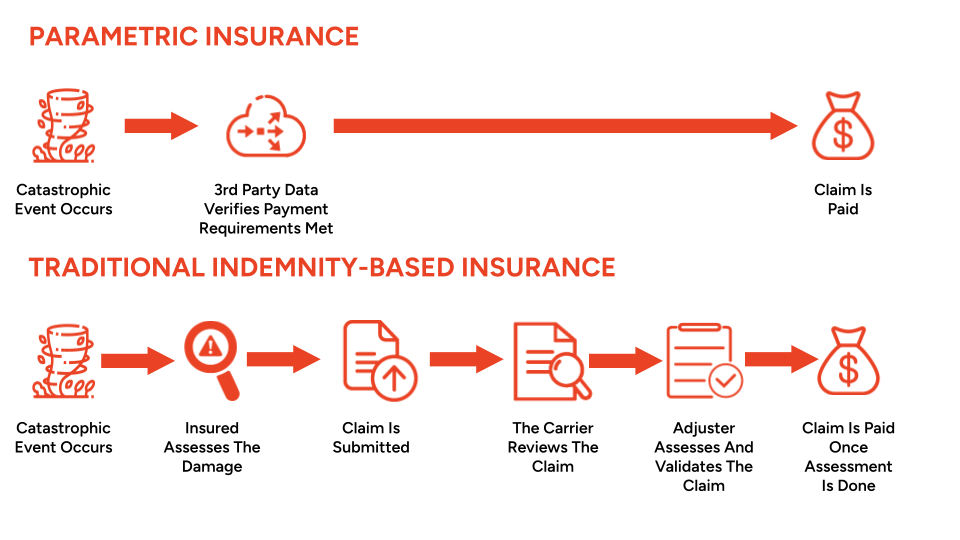

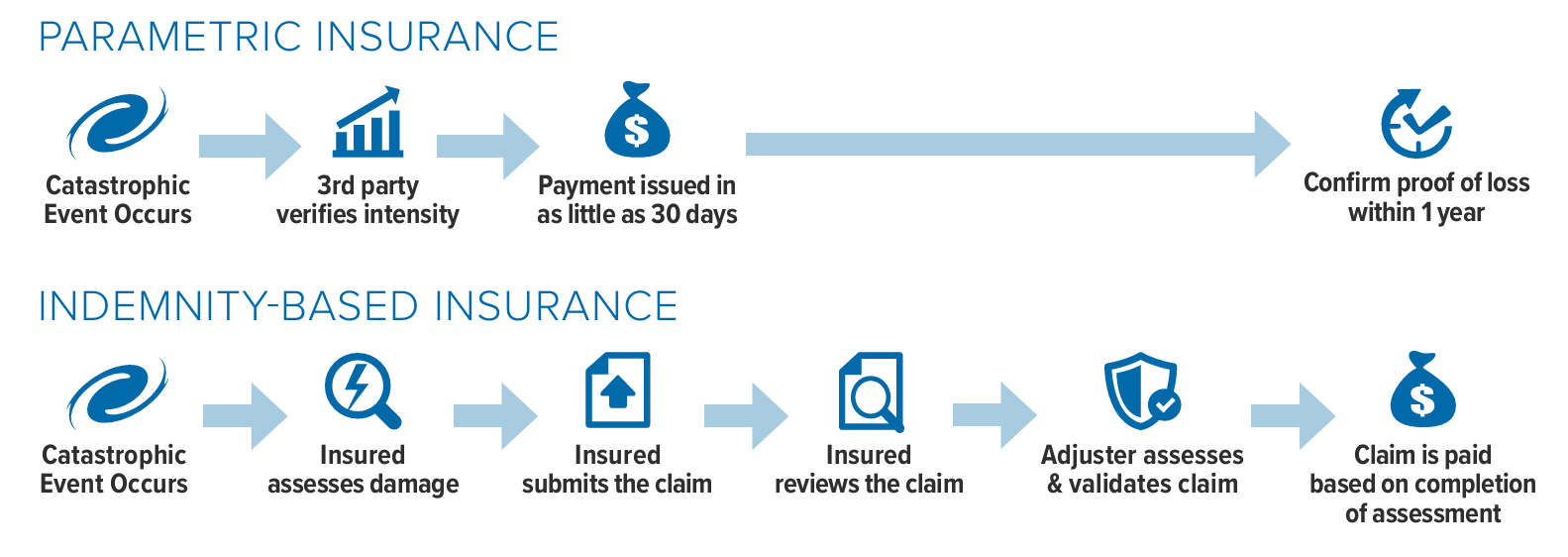

How Parametric Insurance Works

1. Establishing the Trigger

The policy begins by identifying an objective parameter (e.g., earthquake magnitude, wind speed). This parameter is measured using reliable data sources like weather stations or satellite data.

2. Setting the Coverage

Policyholders and insurers agree on a payout structure based on the severity of the event. For example:

– 5.0 magnitude earthquake: $50,000 payout

– 6.0 magnitude earthquake: $100,000 payout

3. Monitoring the Event

When an event occurs, data is collected from third-party sources. If the parameter meets or exceeds the trigger, the insurer releases the payout.

Benefits of Parametric Insurance

1. Faster Claims Settlement

Traditional insurance often involves lengthy claims investigations. Parametric insurance removes this step, offering instant payouts when triggers are met.

2. Transparent and Objective

Since triggers are based on measurable data, there’s no ambiguity in claims. This transparency strengthens trust between insurers and policyholders.

3. Cost-Effective Coverage

Lower administrative costs make parametric policies more affordable, especially for regions prone to natural disasters.

4. Covers Uninsurable Risks

Parametric insurance addresses risks like droughts or business interruption that are challenging for traditional insurers to underwrite.

“With parametric insurance, businesses can plan better and respond faster, ensuring continuity even in the face of adversity.”

Applications of Parametric Insurance

Parametric insurance is revolutionizing multiple industries, including:

1. Agriculture

Farmers can insure against droughts or floods, ensuring financial stability when weather patterns disrupt crop yields.

2. Energy

Energy companies use parametric policies to mitigate risks from weather-related disruptions, such as hurricanes affecting offshore drilling operations.

3. Tourism

Resorts and event planners protect themselves against adverse weather conditions that could affect bookings or attendance.

4. Climate Change

Governments and NGOs use parametric insurance to address extreme weather events, protecting vulnerable communities from financial devastation.

Challenges and Limitations

While parametric insurance offers unique advantages, there are some considerations:

1. Basis Risk

This occurs when the payout doesn’t fully match the loss. For example, a farmer may experience crop damage even if rainfall exceeds the policy trigger.

2. Limited Customization

Although flexible, parametric policies may not cover all risks comprehensively, leaving gaps in protection.

3. Data Dependency

The effectiveness of parametric insurance relies on accurate and reliable data sources. Poor data quality can lead to disputes or inaccurate payouts.

Comparing Parametric Insurance with Traditional Insurance

| Feature | Parametric Insurance | Traditional Insurance |

|---|---|---|

| Trigger | Predefined parameter | Actual loss incurred |

| Claims Process | Automated, instant payout | Lengthy investigation and documentation |

| Cost | Often more affordable | Higher due to administrative expenses |

| Coverage | Event-based | Comprehensive, loss-based |

Future of Parametric Insurance

The parametric insurance market is set to grow significantly, driven by technological advancements and increasing climate-related risks. Key trends include:

1. Integration with IoT

Internet of Things (IoT) devices can provide real-time data for more accurate and dynamic policies.

2. Expansion to Emerging Markets

Developing countries are adopting parametric insurance to address vulnerabilities like droughts, floods, and cyclones.

3. Use of AI and Big Data

Artificial intelligence and big data analytics will enhance the precision of trigger parameters and risk assessments.

“As climate change intensifies, parametric insurance offers a sustainable solution to manage complex risks.”

FAQs About Parametric Insurance

1. What makes parametric insurance different from traditional policies?

Parametric insurance pays based on predefined events, whereas traditional insurance compensates actual losses.

2. Can parametric insurance cover personal risks?

While primarily used in commercial settings, some insurers are exploring personal parametric policies for travel or home insurance.

3. Is parametric insurance regulated?

Yes, parametric insurance follows the same regulatory frameworks as traditional insurance, ensuring fairness and compliance.

4. How is the trigger data verified?

Trigger data is obtained from trusted third-party sources like weather agencies, seismic monitors, or satellite systems.

How to Choose a Parametric Insurance Policy

When selecting a parametric insurance policy, consider the following:

- Understand Your Risks: Identify the specific risks you want coverage for (e.g., hurricanes, droughts).

- Evaluate Trigger Parameters: Ensure the trigger aligns closely with your potential losses to reduce basis risk.

- Check Data Sources: Reliable and transparent data sources are essential for effective claims processing.

- Compare Providers: Research insurers offering parametric policies tailored to your industry or region.

Conclusion

Parametric insurance is reshaping the insurance industry by offering speed, simplicity, and reliability. It’s not just a policy—it’s a proactive approach to managing risks in an uncertain world. From agriculture to energy and climate resilience, parametric insurance empowers individuals and organizations to weather the storm—literally and figuratively.

As the demand for innovative risk management grows, embracing parametric insurance could be your key to financial stability and peace of mind.

“In the face of unpredictable risks, parametric insurance provides certainty when you need it most.”