Understanding Microinsurance Models: A Key to Affordable Coverage

In today’s world, microinsurance models have emerged as a critical tool in bridging the gap between insurance providers and underserved populations. These innovative frameworks are tailored to provide affordable and accessible insurance products, ensuring financial inclusion for low-income individuals. This article delves into the types, benefits, challenges, and global examples of microinsurance models, highlighting their transformative impact on communities worldwide.

What is Microinsurance?

Microinsurance refers to insurance products designed to protect low-income individuals and families against specific risks such as health, agriculture, or property loss. Unlike traditional insurance, microinsurance policies are affordable, have simplified terms, and are often distributed through non-conventional channels.

Did you know? Microinsurance can help protect over 4 billion people globally who live on less than $5 per day.

Key Microinsurance Models

1. Community-Based Models

Community-based models operate on a principle of solidarity and trust, often managed by local organizations or cooperatives.

- How it works: Community members pool their resources to create a collective fund.

- Advantages:

- Promotes ownership and trust.

- Low administrative costs.

- Challenges:

- Limited risk diversification.

- Often dependent on external support for sustainability.

For example, in India, community health insurance schemes cater to rural households, offering coverage for essential health services at nominal costs.

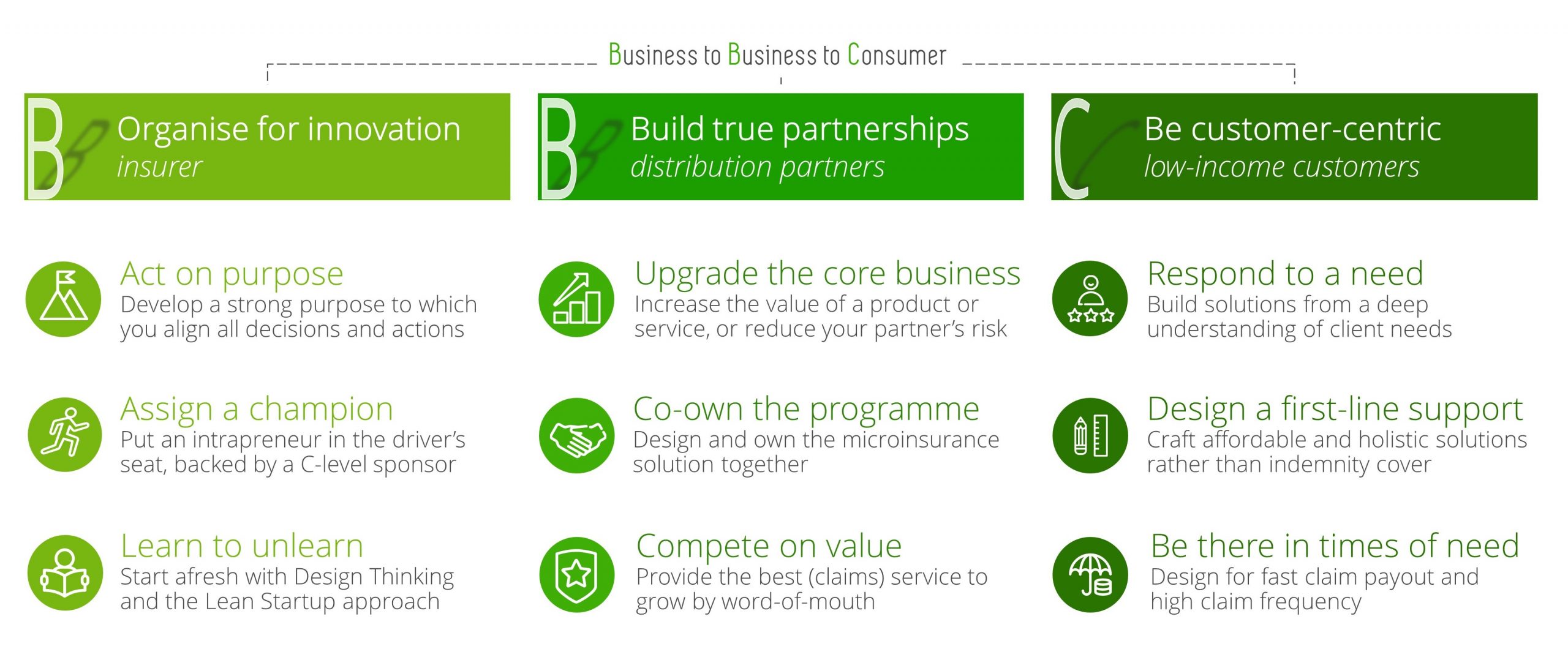

2. Partner-Agent Models

In the partner-agent model, an insurance company collaborates with a local organization or NGO to distribute microinsurance products.

- How it works: The insurer underwrites the risks, while the agent handles distribution and client relations.

- Advantages:

- Combines the expertise of insurers and agents.

- Scalable and replicable.

- Challenges:

- Potential misalignment of objectives between partners.

- Requires robust training for agents.

Example: MicroEnsure, a global leader in microinsurance, uses this model to offer insurance to millions in Africa and Asia.

3. Full-Service Provider Models

In this model, a single organization handles all aspects of the insurance process, from product design to claims management.

- How it works: The provider is responsible for underwriting, distribution, and servicing.

- Advantages:

- Greater control over processes.

- Ensures uniform service quality.

- Challenges:

- High operational costs.

- Limited outreach without partnerships.

Grameen Bank’s microinsurance initiatives in Bangladesh exemplify this approach, offering coverage for health, life, and property risks.

4. Peer-to-Peer (P2P) Models

The P2P model leverages technology to connect individuals who pool their resources and share risks.

- How it works: Members contribute to a digital fund used to cover claims collectively.

- Advantages:

- Transparent and cost-effective.

- Leverages digital platforms for outreach.

- Challenges:

- Limited adoption in rural areas due to technology barriers.

For more on how technology is transforming insurance, check out this article on digital insurance innovations.

Key Benefits of Microinsurance

- Financial Security for Low-Income Groups

- Protects against unexpected risks like medical emergencies or crop failures.

- Promotes Social Inclusion

- Encourages financial independence and reduces reliance on informal credit.

- Boosts Economic Stability

- Safeguards livelihoods, enabling economic growth at the grassroots level.

- Encourages Risk Mitigation

- Instills a culture of preparedness among vulnerable communities.

Challenges in Microinsurance

Despite its potential, microinsurance faces several challenges:

- Low Awareness: Many potential beneficiaries are unaware of microinsurance benefits.

- High Distribution Costs: Reaching rural and remote areas can be costly.

- Adverse Selection: High-risk individuals are more likely to enroll, impacting the risk pool.

- Regulatory Hurdles: Lack of consistent regulations across countries can limit growth.

Overcoming Challenges

Collaboration between governments, NGOs, and private insurers can help address these barriers. Innovative technologies like blockchain and mobile platforms are also reshaping distribution strategies, making microinsurance more efficient.

Real-World Examples

1. PhilHealth in the Philippines

The PhilHealth Insurance Program provides affordable health coverage to low-income households, funded by government subsidies.

2. Kilimo Salama in Kenya

A weather-indexed crop insurance scheme protecting farmers against climate risks, distributed via mobile technology.

3. VimoSEWA in India

Run by the Self-Employed Women’s Association (SEWA), this program offers life, health, and asset insurance to women workers.

FAQs

1. What is the difference between microinsurance and traditional insurance?

Microinsurance is specifically designed for low-income individuals, offering smaller coverage amounts, simplified processes, and affordable premiums compared to traditional insurance.

2. How do technology and microinsurance intersect?

Technology enhances microinsurance by enabling mobile-based enrollment, automating claims, and utilizing data analytics for product design.

3. Who regulates microinsurance?

Microinsurance is typically regulated by national insurance authorities, though some countries have dedicated microinsurance policies.

Conclusion

Microinsurance models play a pivotal role in achieving financial inclusion and resilience for underserved populations. By understanding and adopting these innovative frameworks, stakeholders can make insurance products more affordable, accessible, and impactful. The future of microinsurance lies in public-private partnerships, technological advancements, and community-driven initiatives. Together, these can ensure a world where no one is left vulnerable to financial shocks.

For more information on microinsurance trends, visit Microinsurance Network.

End of Article