Understanding Credit Scores & Reports

Managing your financial health begins with understanding two critical components: credit scores and credit reports. These tools are not just numbers and documents; they represent your financial trustworthiness and can significantly influence your ability to secure loans, mortgages, or even rental agreements. This article will delve into what credit scores and reports are, how they are calculated, their importance, and practical tips to improve your credit score.

What is a Credit Score?

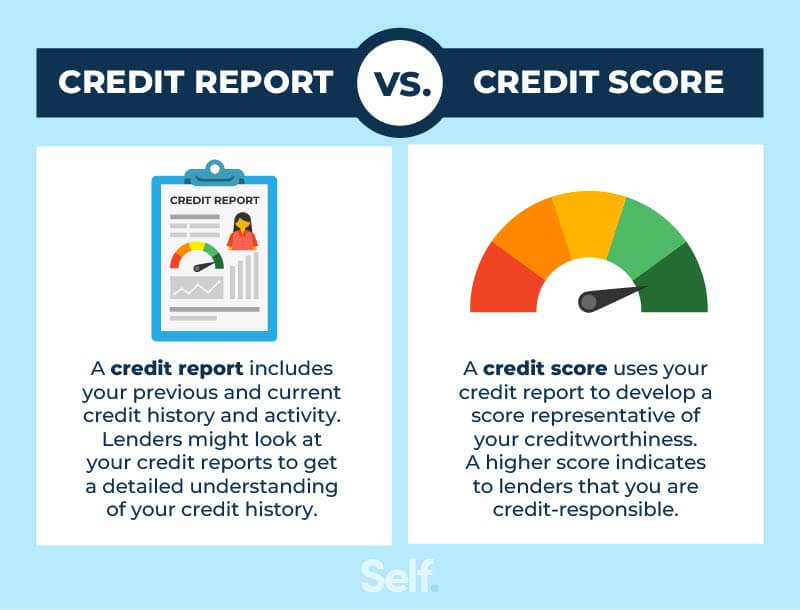

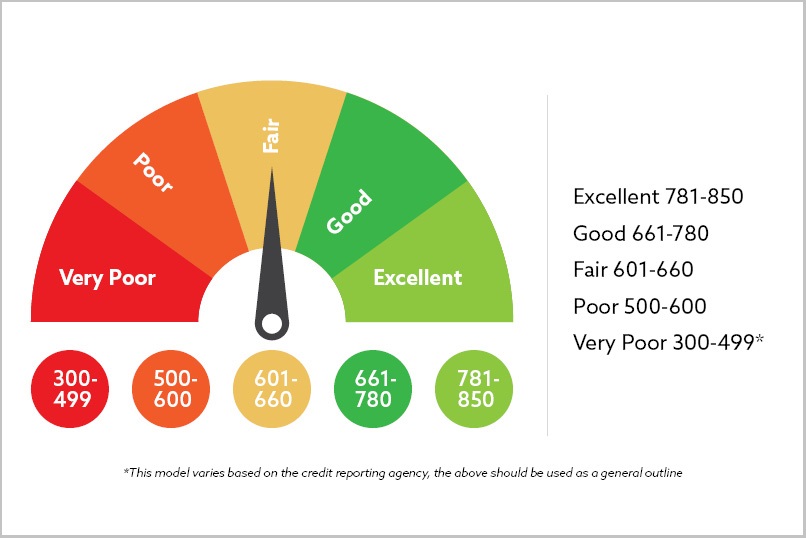

A credit score is a numerical representation of your creditworthiness. Typically ranging from 300 to 850, this score is determined by various factors that reflect your credit history. Higher scores indicate a lower risk for lenders, while lower scores suggest potential difficulties in repaying borrowed money.

The Components of a Credit Score

Understanding what influences your credit score is crucial for effective management. Here are the primary components:

- Payment History (35%): Timely payments on loans and credit cards significantly boost your score.

- Credit Utilization (30%): This is the ratio of your current credit card balances to your total credit limits. Keeping it below 30% is advisable.

- Length of Credit History (15%): A longer credit history tends to improve your score.

- Types of Credit (10%): A mix of credit types (credit cards, mortgages, etc.) can positively impact your score.

- New Credit (10%): Opening multiple new accounts within a short period can lower your score due to hard inquiries.

How Credit Scores are Calculated

The calculation of credit scores is typically done through two main scoring models: FICO and VantageScore.

- FICO: This model is the most widely used and emphasizes payment history and credit utilization.

- VantageScore: Developed by the three major credit bureaus, it provides a more comprehensive view by considering a broader range of factors.

For a deeper understanding of these scoring models, you can visit FICO and VantageScore.

Understanding Credit Reports

A credit report is a detailed record of your credit history. It includes information about your credit accounts, payment history, and outstanding debts. Unlike credit scores, which provide a snapshot of your creditworthiness, credit reports offer a comprehensive view of your financial behavior.

What Information is Included in a Credit Report?

Your credit report contains various elements, including:

- Personal Information: Your name, address, Social Security number, and employment history.

- Credit Accounts: Details of your credit cards, loans, and payment history.

- Inquiries: A list of entities that have accessed your credit report, categorized as hard or soft inquiries.

- Public Records: Information on bankruptcies, tax liens, or other financial judgments.

The Importance of Regularly Checking Your Credit Report

Regularly reviewing your credit report is essential for maintaining your financial health. It allows you to:

- Identify Errors: Mistakes can negatively impact your credit score. If you find any, you can dispute them with the credit bureau.

- Prevent Identity Theft: Monitoring your report helps detect unauthorized accounts or inquiries.

- Understand Your Financial Health: A clear view of your credit history can guide your financial decisions.

For more information on obtaining your credit report for free, visit AnnualCreditReport.com.

How Credit Scores Impact Your Finances

Understanding the significance of your credit score can help you make informed financial decisions. Here’s how it impacts various aspects of your financial life:

The Role of Credit Scores in Loan Approvals

Lenders heavily rely on credit scores when deciding whether to approve your loan applications. A higher score typically results in more favorable loan terms, including:

- Lower Interest Rates: With a good credit score, you are likely to receive lower rates, saving you money over the loan’s term.

- Higher Credit Limits: Lenders may offer you higher credit limits, allowing more financial flexibility.

Other Financial Implications of Credit Scores

Your credit score can also influence:

- Insurance Premiums: Many insurers use credit scores to determine premiums. A higher score can lead to lower rates.

- Rental Applications: Landlords often check credit scores as part of their tenant screening process.

- Employment Opportunities: Some employers check credit reports during the hiring process, particularly for financial positions.

By now, you should have a solid understanding of credit scores and reports. Stay tuned for the next section, where we’ll discuss how to improve your credit score with actionable tips and debunk common myths surrounding credit.

Tips for Improving Your Credit Score

Improving your credit score is essential for achieving your financial goals. Here are several actionable tips to help you boost your score over time:

1. Pay Your Bills on Time

Payment history is the most significant factor affecting your credit score. Late payments can have a negative impact for years. To ensure timely payments, consider the following:

- Set Up Autopay: Automate your payments for bills and loans to avoid missing due dates.

- Use Reminders: Set calendar reminders a few days before each payment is due.

2. Keep Credit Utilization Low

Maintaining a low credit utilization ratio (ideally below 30%) can enhance your score. Here’s how to manage it effectively:

- Pay Off Balances: Try to pay your credit card balances in full each month.

- Request Higher Credit Limits: If possible, request an increase in your credit limits, which can help reduce your utilization ratio without changing your spending habits.

3. Diversify Your Credit Mix

A healthy mix of different types of credit (such as credit cards, installment loans, and mortgages) can positively influence your credit score. Consider these steps:

- Consider Different Credit Types: If you have only credit cards, you might explore obtaining an installment loan.

- Avoid Unnecessary Credit Accounts: While diversifying is important, opening too many accounts in a short period can harm your score.

4. Monitor Your Credit Report Regularly

Regularly checking your credit report helps you catch errors or fraud that can negatively impact your score. Here’s how you can keep tabs:

- Free Annual Reports: Obtain a free copy of your credit report at AnnualCreditReport.com.

- Use Credit Monitoring Services: Consider subscribing to a credit monitoring service that alerts you to changes in your report.

5. Limit Hard Inquiries

Every time you apply for credit, a hard inquiry is made on your report, which can lower your score. To minimize the impact:

- Limit Applications: Only apply for new credit when necessary.

- Rate Shopping: If you’re looking for a loan (like a mortgage), try to apply for all loans within a short period. Most scoring models count multiple inquiries as one if done within a certain time frame.

6. Build a Positive Credit History

Establishing a long-term credit history is crucial for improving your credit score. Here are ways to build that history:

- Keep Old Accounts Open: Even if you don’t use them, keeping older credit accounts open can positively impact your average account age.

- Use Secured Credit Cards: If you’re new to credit or rebuilding, secured cards can be a good way to start building your credit.

Common Myths About Credit Scores

There are many misconceptions about credit scores that can lead to poor financial decisions. Here are some common myths debunked:

Myth 1: Checking Your Own Credit Lowers Your Score

Fact: When you check your own credit, it’s considered a soft inquiry and does not impact your score at all.

Myth 2: Closing Old Accounts Improves Your Score

Fact: Closing old credit accounts can actually harm your score by reducing your credit history length and increasing your utilization ratio.

Myth 3: All Debt is Bad

Fact: Not all debt is harmful. Some types of debt, like mortgages or student loans, can contribute positively to your credit history if managed well.

Frequently Asked Questions (FAQs)

Q1: How often should I check my credit report?

It’s recommended to check your credit report at least once a year. You can also monitor it more frequently if you’re planning to apply for major loans or credit.

Q2: How long do negative marks stay on my credit report?

Generally, late payments remain on your report for seven years, while bankruptcies can last for up to ten years.

Q3: Can I improve my credit score quickly?

While substantial improvements often take time, making timely payments, reducing your utilization, and disputing errors can lead to quicker gains.

Conclusion

Understanding and actively managing your credit score and report is crucial for financial success. By implementing the tips outlined above, you can improve your credit score and secure better financial opportunities in the future. Remember, knowledge is power—stay informed, stay proactive, and your financial health will follow.

For further reading, consider exploring articles on credit management and understanding your credit report.