Umbrella Insurance for Businesses: Why It’s Essential for Your Protection

When you think about business insurance, you might imagine the standard policies like general liability or property insurance. While these are essential, they only cover specific risks. But what happens if your business faces a lawsuit or claim that exceeds the limits of your existing policies? This is where umbrella insurance for businesses steps in to provide an extra layer of protection.

In this detailed guide, we will explore what umbrella insurance is, how it works, and why it’s a crucial investment for your business. Whether you’re a small startup or a large corporation, understanding how umbrella insurance can safeguard your business from unexpected financial burdens is essential.

:max_bytes(150000):strip_icc()/how-umbrella-insurance-works.asp-final-abbaf8b8db4f4056931adc7e57f40af9.png)

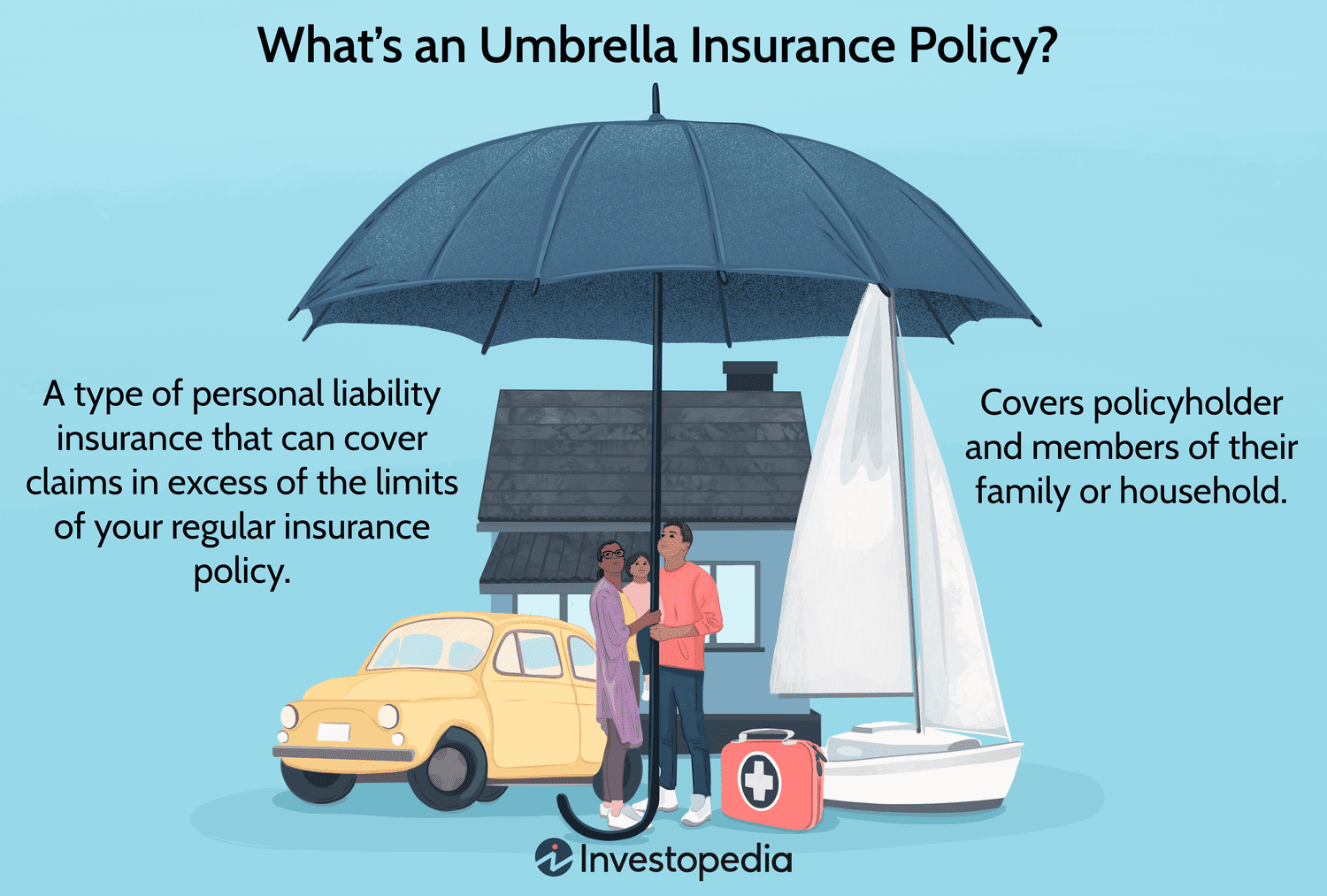

What Is Umbrella Insurance for Businesses?

Umbrella insurance is a type of liability coverage that provides additional protection beyond the limits of your other existing business policies, such as general liability or commercial auto insurance. This extra layer of coverage kicks in when your primary policy reaches its limit, helping cover costs associated with legal fees, medical expenses, and other damages that may arise from lawsuits or claims.

While it’s typically used to extend coverage for liability claims, business umbrella insurance can also protect against a wide range of risks, including property damage, advertising injuries, and certain types of personal injury claims.

Why Should Your Business Consider Umbrella Insurance?

The core reason businesses opt for umbrella insurance is to safeguard their assets. If a significant lawsuit arises or if a settlement exceeds your standard insurance policy’s limits, umbrella insurance will cover the difference, ensuring your company doesn’t bear the entire financial burden.

Key Benefits of Umbrella Insurance:

- Higher Coverage Limits: Provides additional coverage when your primary policies reach their limits.

- Extended Protection: Covers scenarios not included in standard business insurance policies.

- Affordable: Compared to the amount of coverage it provides, umbrella insurance is often a cost-effective solution for businesses.

- Legal Defense: In the event of a lawsuit, umbrella insurance also covers legal fees, ensuring your business isn’t financially drained by defending against a claim.

How Does Umbrella Insurance Work?

Umbrella insurance for businesses works by providing additional coverage once your primary business insurance policies (like general liability or auto insurance) have reached their limits. It acts as an extra cushion to prevent your business from facing significant financial strain due to lawsuits or major claims.

Here’s how it works in a step-by-step manner:

- Step 1: A Claim or Lawsuit Occurs

A customer, vendor, or third party files a claim against your business. This could be due to property damage, bodily injury, or other reasons. -

Step 2: Your Primary Policy Coverage is Used

The first step in resolving the claim involves using your existing business insurance policy. If your general liability coverage is $500,000 and the claim amount is $300,000, your policy will pay for the entire claim. -

Step 3: The Claim Exceeds Your Policy’s Limit

If the claim exceeds your policy’s coverage limit, for example, if the damages are $800,000, your business will be responsible for paying the remaining $300,000, unless you have umbrella insurance. -

Step 4: Umbrella Insurance Kicks In

Once the limits of your primary insurance policy are exhausted, umbrella insurance steps in to cover the remaining costs, up to the policy’s limit.

Real-World Example:

Imagine a situation where a customer slips and falls in your store. If the medical expenses and legal fees related to the incident exceed your general liability coverage, your umbrella policy will help cover the difference, protecting your business from financial strain.

What Does Umbrella Insurance Cover?

Umbrella insurance offers an additional layer of protection for a variety of liability risks. While coverage varies by provider and policy, umbrella insurance typically covers:

1. Bodily Injury Liability

If someone is injured on your business property or due to your business operations, umbrella insurance can help cover the medical expenses, legal fees, and settlement costs that exceed the limits of your regular general liability insurance.

2. Property Damage Liability

If your business causes damage to another person’s property (for example, if your employee damages a client’s property while working on-site), umbrella insurance will cover the additional costs beyond your commercial property insurance.

3. Legal Defense Costs

Legal fees can quickly add up, even if your business is not at fault. Umbrella insurance often covers the cost of legal defense, including lawyer fees and court expenses, associated with a liability claim or lawsuit.

4. Personal and Advertising Injury

Umbrella policies may also cover injuries related to slander, libel, or false advertising that may arise in your business operations.

5. Rental Property Liability

If your business rents or leases property, umbrella insurance can protect against liability claims that arise from accidents or injuries on your leased premises.

What Doesn’t Umbrella Insurance Cover?

While umbrella insurance offers extensive coverage, it doesn’t cover everything. Some of the common exclusions include:

- Employee Injuries: If an employee gets injured while working, workers’ compensation insurance should cover the costs, not umbrella insurance.

- Damage to Your Own Property: Umbrella insurance won’t cover damage to your own business property; this should be covered under your property insurance.

- Criminal Acts or Fraud: Claims arising from illegal activities or fraudulent actions aren’t covered under an umbrella policy.

- Business Loss or Disruption: Umbrella insurance doesn’t cover business interruption or losses due to events like natural disasters.

How Much Umbrella Insurance Does Your Business Need?

The amount of umbrella insurance your business needs depends on several factors, including the nature of your business, its size, and the amount of risk involved. Generally, it’s recommended that you consider:

- The potential value of a lawsuit: If your business deals with high-value transactions, such as in real estate or contracting, you may need higher coverage.

- The size of your current policies: The limits of your existing business insurance policies, like general liability or auto insurance, will help determine how much umbrella coverage you need.

- Assets at risk: Consider how much you have invested in your business, as umbrella insurance will protect your assets in the event of a lawsuit.

Recommended Coverage:

- Small businesses: $1 million to $2 million in umbrella coverage is typically sufficient.

- Medium to large businesses: Depending on the industry, $5 million or more may be necessary to cover the full range of risks.

FAQs About Umbrella Insurance for Businesses

1. Do I need umbrella insurance if I already have general liability insurance?

Yes, if your general liability insurance coverage is exhausted, umbrella insurance can protect your business by covering the remaining costs. It provides an added layer of protection beyond your primary policies.

2. How much does umbrella insurance for businesses cost?

The cost of business umbrella insurance depends on the level of coverage and the type of business you operate. On average, businesses can expect to pay between $400 to $1,500 per year for an umbrella policy with a coverage limit of $1 million.

3. Is umbrella insurance available for all types of businesses?

Yes, umbrella insurance can be customized for most types of businesses, whether you’re a small startup or a large corporation. It’s especially beneficial for businesses that face higher risks of lawsuits or have valuable assets to protect.

4. Can umbrella insurance cover international claims?

Umbrella insurance typically covers global claims, but it’s important to check with your provider to ensure it applies to the specific regions where your business operates.

5. How do I get umbrella insurance for my business?

Contact your current insurance provider to inquire about adding umbrella insurance to your existing policies. They can help you customize a policy that meets your business’s needs.

Conclusion

In conclusion, umbrella insurance for businesses is an essential investment that helps protect your business from unforeseen financial setbacks caused by lawsuits and claims. By providing additional liability coverage beyond your existing policies, umbrella insurance ensures that your business remains financially stable in the face of unexpected legal challenges.

For more information about umbrella insurance, visit Investopedia or consult with your insurance agent to determine the best coverage for your business.

Protecting your business today can save you from significant financial loss in the future. Investing in umbrella insurance is a smart way to ensure that your business stays covered, no matter what happens.