Introduction: Why Tax Planning Matters for Young Professionals

Image source: Tax Planning Tips

Image source: Tax Planning Tips

Tax planning is essential for young professionals who are often navigating the complexities of financial independence for the first time. As you embark on your career, understanding the various aspects of taxation can significantly impact your take-home pay, savings potential, and overall financial health.

Effective tax planning allows you to maximize your deductions and credits, thereby increasing your potential tax refund and allowing you to allocate more funds towards critical investments like retirement savings, travel, or home purchases. With the right strategies in place, you can take proactive steps to ensure that your taxes are managed efficiently.

Here are a few compelling reasons why tax planning should be high on your priority list:

- Financial Stability: Young professionals typically face student loans, housing costs, and other financial responsibilities. By implementing smart tax strategies, you can alleviate some of this burden.

- Avoiding Surprises: By planning ahead, you can avoid unexpected tax bills that can arise from underestimating your tax liability or failing to claim available deductions.

- Long-Term Growth: Understanding how tax credits and deductions work not only helps you save money now but also lays the foundation for better financial planning in the future.

- Leveraging Opportunities: The tax code offers various incentives, especially for young professionals, such as education credits and deductions for work-related expenses. Utilizing these can greatly enhance your financial position.

As you continue to climb the career ladder, taking the time to invest in tax planning can lead to significant benefits, both in your current lifestyle and your long-term financial goals. Therefore, familiarize yourself with the tax regulations that apply to you, stay organized, and seek professional advice if necessary to ensure you’re on the right track.

Taking control of your tax planning is not just a prudent financial strategy; it’s an essential practice that empowers you to build a prosperous future.

Understanding Tax Basics

What Are Tax Deductions and Credits?

Tax deductions and credits are essential tools that can significantly reduce your tax liability, making them vital for young professionals navigating financial responsibilities.

- Tax Deductions reduce your taxable income, allowing you to pay taxes on a lower amount. Common deductions include those for student loan interest, mortgage interest, and charitable contributions. For instance, if you earn $50,000 and have $5,000 in deductions, your taxable income drops to $45,000. This decrease directly translates to a lower tax bill.

-

Tax Credits, on the other hand, provide a dollar-for-dollar reduction in the amount of tax you owe. For example, if you qualify for a $1,000 tax credit and owe $3,000 in taxes, your tax bill will be reduced to $2,000. Tax credits can be particularly valuable as they directly lower your overall payable amount, maximizing your potential refund. Notable tax credits include the Earned Income Tax Credit (EITC) and the Child Tax Credit.

Understanding these distinctions can empower young professionals to optimize their tax filings effectively. For more detailed insights into deductions and credits, you can visit the IRS website.

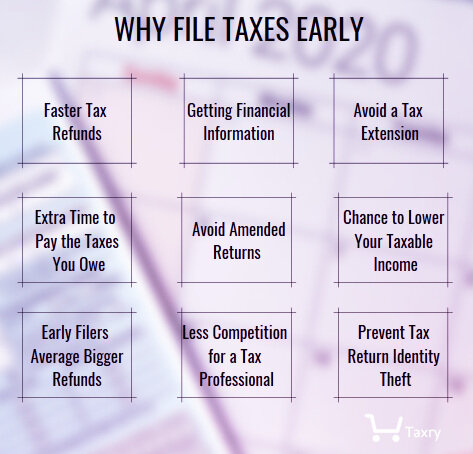

The Importance of Filing Early

Filing your taxes early can offer numerous advantages that young professionals should not overlook.

- Maximize Refund Opportunities: By filing sooner, you enable the IRS to process your return faster, potentially getting your tax refund sooner than if you wait until the deadline.

-

Avoid Last-Minute Stress: Waiting until the last minute can lead to errors or omissions, which could trigger an IRS audit. Filing early gives you ample time to double-check your forms and ensure accuracy.

-

Better Planning for Payment: If you owe taxes, early filing allows you to prepare financially, spreading payments out instead of facing a lump sum right before the deadline.

-

Fewer Risks of Identity Theft: Tax identity theft is a growing concern. By filing early, you minimize the risk of someone else filing a return in your name, as your return will be submitted first.

In conclusion, understanding the basics of tax deductions and credits, along with the benefits of filing early, plays a crucial role in effective tax planning for young professionals. This knowledge not only supports financial stability but also enhances overall monetary health in the long run.  Image source: Why File Taxes Early

Image source: Why File Taxes Early

Top Tax Deductions for Young Professionals

Education and Student Loan Interest Deductions

:stripicc()/student-loan-interest-deduction-3193022HL-6a2dfcbfdccb47479d5a544f175feaf1.gif) Image source: The Balance Money

For young professionals navigating the complexities of student debt, understanding how to leverage education-related tax deductions can significantly ease financial burdens. The Student Loan Interest Deduction allows you to deduct up to $2,500 annually from your taxable income for interest paid on qualifying student loans. This deduction can be particularly beneficial for recent graduates who are still managing monthly loan payments while establishing their careers.

To qualify for this deduction, your modified adjusted gross income (MAGI) must be below certain limits, which are updated annually. As of 2023, if your MAGI is above $85,000 (or $175,000 if filing jointly), the deduction begins to phase out. Ensure that you report your interest payment accurately; typically, your loan servicer will send you a Form 1098-E summarizing the interest you’ve paid over the year. Young professionals should also remain aware of potential changes in tax law as new relief options may arise in response to the ongoing discussions about student debt.

For more detailed information, you can visit the IRS website on Student Loan Interest Deduction.

Work-Related Expenses You Can Deduct

When it comes to work-related expenses, young professionals often overlook potential deductions that can save them money on their taxes. Many job-related costs are deductible, especially for those who are not reimbursed by their employer. Some common examples include:

- Home Office Deduction: If you’re working from home, you may qualify for a home office deduction. To utilize this, your space must be used exclusively and regularly for business purposes.

- Supplies and Equipment: Costs incurred for purchasing supplies, tools, and equipment needed for your job can be deducted. This may include anything from computer software to office furniture.

- Education and Training: Courses, seminars, and other training programs that improve your job skills can often be written off. This is particularly relevant for young professionals seeking to rise in their careers.

- Travel Expenses: If your job requires travel, expenses such as transportation, lodging, and meals may be deductible. It’s essential to keep detailed receipts and records for all travel-related expenses.

While the Tax Cuts and Jobs Act suspended many unreimbursed employee expense deductions, some still remain relevant, especially for self-employed individuals or freelancers. Young professionals should track their expenses carefully throughout the year and consider using accounting software to stay organized.

If you’re unsure about what’s deductible, consulting with a tax professional can provide clarity and ensure you’re maximizing your deductions. Remember, planning now can lead to financial benefits when you file your taxes.

For more insights on deductible expenses, see this comprehensive guide on the IRS website.

Maximizing Tax Credits to Boost Your Refund

Understanding the Earned Income Tax Credit (EITC)

The Earned Income Tax Credit (EITC) is a significant tax benefit designed to support low-to-moderate-income working individuals and families. This refundable credit not only reduces the amount of tax you owe but can potentially increase your refund, making it a valuable financial tool for eligible taxpayers.

To qualify for the EITC, you must meet specific income limits and have earned income from employment or self-employment. Here are the key eligibility criteria:

- Filing Status: You can be single, married filing jointly, or head of household. However, married individuals filing separately typically do not qualify.

- Income Limits: Your earned income and adjusted gross income (AGI) must fall below certain thresholds, which can change annually. It’s essential to check the current limits on the IRS website to determine your eligibility.

- Qualifying Children: You may receive a higher credit amount if you have qualifying children. The number of children you claim also affects the credit you can receive.

For 2023, the maximum credit ranges from about $600 for those with no qualifying children to over $7,000 for families with three or more children. The EITC not only aids in providing financial relief but is also a vital part of the social safety net, helping millions of Americans move towards financial stability.

For a detailed breakdown of eligibility requirements and to check your potential credit, visit the IRS EITC page.

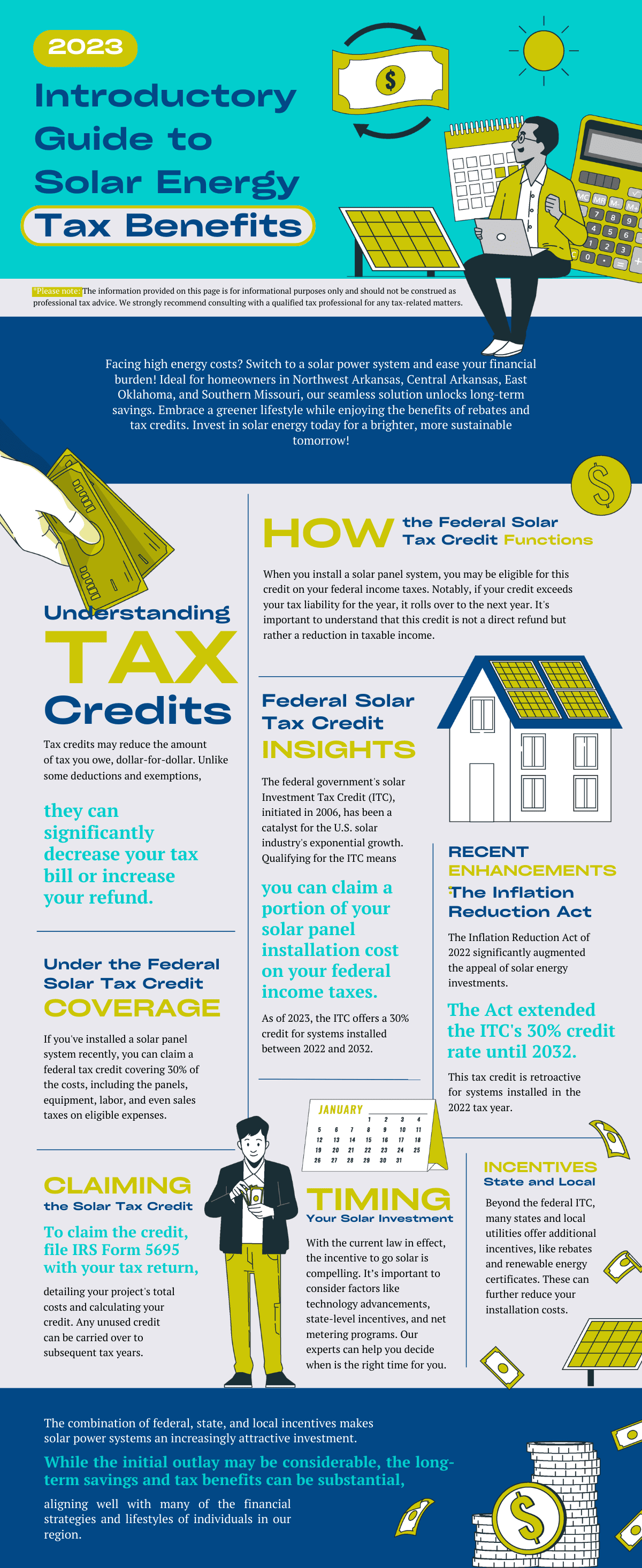

Energy Credits for Sustainable Living

In addition to traditional tax credits, engaging in sustainable living practices can lead to significant savings through energy tax credits. These incentives are designed to encourage homeowners to invest in renewable energy technologies and improve energy efficiency, ultimately benefiting both the environment and your financial bottom line.

- Residential Energy Efficient Property Credit: This credit allows taxpayers to claim a portion of the cost of qualified renewable energy systems, including solar electric, solar water heating, wind, and geothermal heat pumps, directly on their tax return. The credit can cover up to 30% of the costs associated with the installation of these systems.

-

Residential Energy Credit: By making energy-efficient improvements to your home, such as adding insulation, energy-efficient windows, and energy-saving heating and cooling systems, you may be eligible for a tax credit ranging from 10% to 30% of the expenditures, subject to certain limits.

By taking advantage of these energy credits, you’re not only investing in your home but also contributing to a sustainable future. This not only can result in a more substantial tax refund but also promotes long-term savings on energy bills.

To learn more about the specific requirements and eligibility for energy credits, refer to the U.S. Department of Energy for comprehensive resources and updates on available credits.

Image source: Sun City Energy

Image source: Sun City Energy

Smart Tax Strategies for Professionals

Contributing to Retirement Accounts for Tax Benefits

One of the most effective tax strategies for young professionals is to contribute to retirement accounts. This not only supports your future financial stability but also offers immediate tax benefits. There are several retirement accounts available, each with unique advantages:

- Traditional IRA: Contributions to a Traditional IRA may be tax-deductible. This means that the amount you contribute could reduce your taxable income for the year. Additionally, the money in the account grows tax-deferred until you withdraw it in retirement.

-

Roth IRA: While contributions to a Roth IRA are made with after-tax dollars, qualified withdrawals are tax-free. This can be a valuable option for young professionals who expect to be in a higher tax bracket in retirement.

-

401(k) Plans: If your employer offers a 401(k), contributing can be beneficial because many employers match contributions up to a certain percentage. This is essentially free money. In a traditional 401(k), your contributions are made pre-tax, reducing your taxable income, while in a Roth 401(k), qualified withdrawals during retirement are tax-free.

By maxing out contributions to these accounts, you can lower your current tax liability while simultaneously preparing for a financially secure retirement. For more detailed insights on retirement accounts, please visit the IRS Retirement Plans Page.

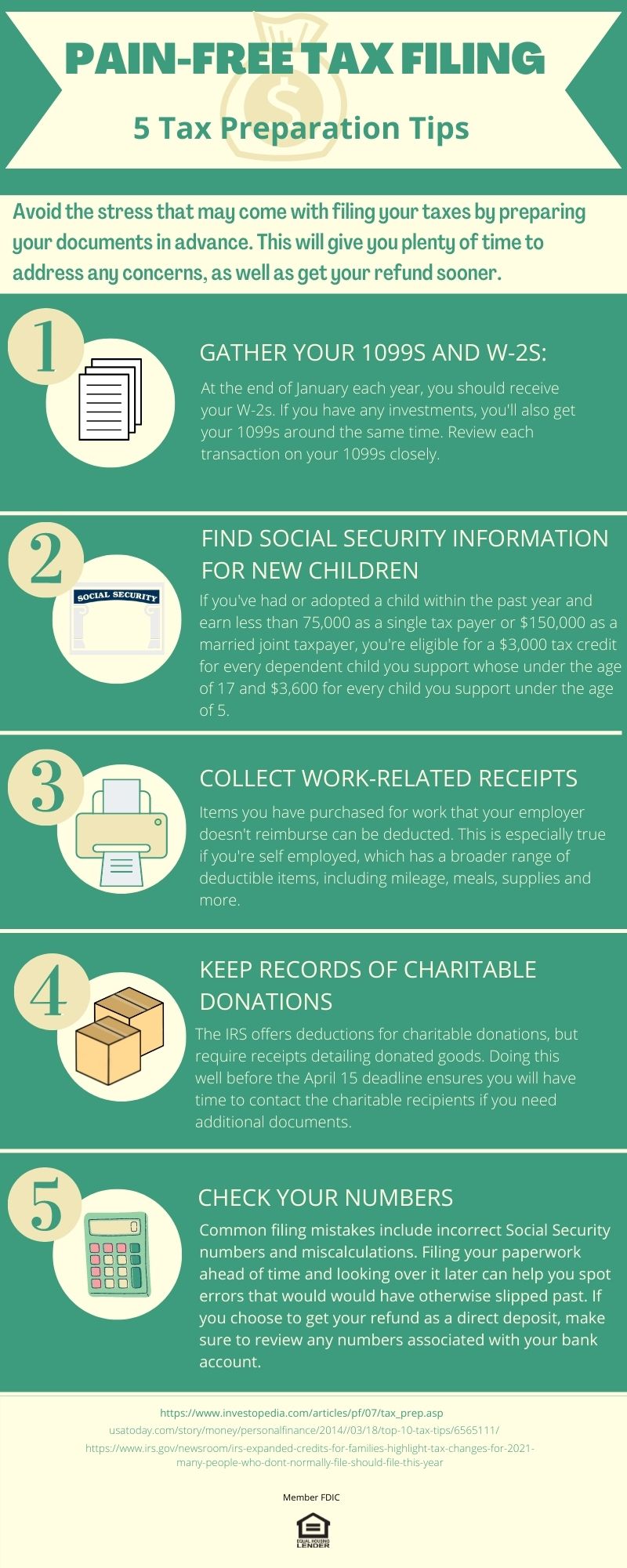

Keeping Digital Records for Easier Tax Filing

Maintaining digital records is essential for an efficient tax filing process. With the rise of technology and the ability to store information online, keeping organized digital records has become simpler than ever. Here are some strategies to ensure your records are efficient and helpful during tax season:

- Use Accounting Software: Consider using software like QuickBooks or FreshBooks to track income and expenses. This can streamline your record-keeping process and allow for easy categorization.

-

Document Expenses: Regularly scan and save receipts and invoices. Tools like Shoeboxed can help digitize your paper trails, ensuring you always have documentation if you need to reference it for deductions.

-

Organize by Category: Create folders for different types of expenses such as medical, educational, or business-related costs. This will make it easier to locate necessary documents when tax season arrives.

-

Secure Cloud Storage: Make use of platforms like Google Drive or Dropbox for secure storage. Cloud services ensure that your records are backed up and accessible from any location.

Adopting a digital approach not only simplifies your tax filing process but also provides peace of mind knowing that all necessary documents are readily available. For additional information about digitizing records, check out this guide from IRS Recordkeeping.

Image source: Central Bank

Image source: Central Bank

Avoiding Common Tax Mistakes

Double-Checking Your Tax Return Before Filing

When it comes to filing your taxes, accuracy is paramount. A simple mistake can lead to delays, penalties, or even an audit by the IRS. That’s why double-checking your tax return before filing is a crucial step that every taxpayer should prioritize. Here are some tips to ensure your return is error-free:

- Verify Personal Information: Ensure that your name, Social Security number, and any other identifying information is entered correctly.

- Income Verification: Cross-verify all your income statements, including W-2s from employers and 1099 forms for freelance work. Missing or incorrect data can lead to significant discrepancies.

- Deductions and Credits: Confirm that you are claiming all the tax deductions and credits you qualify for, such as student loan interest or the Earned Income Tax Credit (EITC). Mistakes in this area can affect your overall tax liability.

- Mathematical Accuracy: Simple math errors can occur easily. Utilize tax software or calculators to ensure that all figures are correct.

- Review for Missing Documents: Make sure all necessary documents are included with your return, preventing any delays in processing.

Taking these steps can save you time and money while providing peace of mind. For more detailed insights into tax preparation, visit The IRS Tax Preparation Page.

Image source: IRS

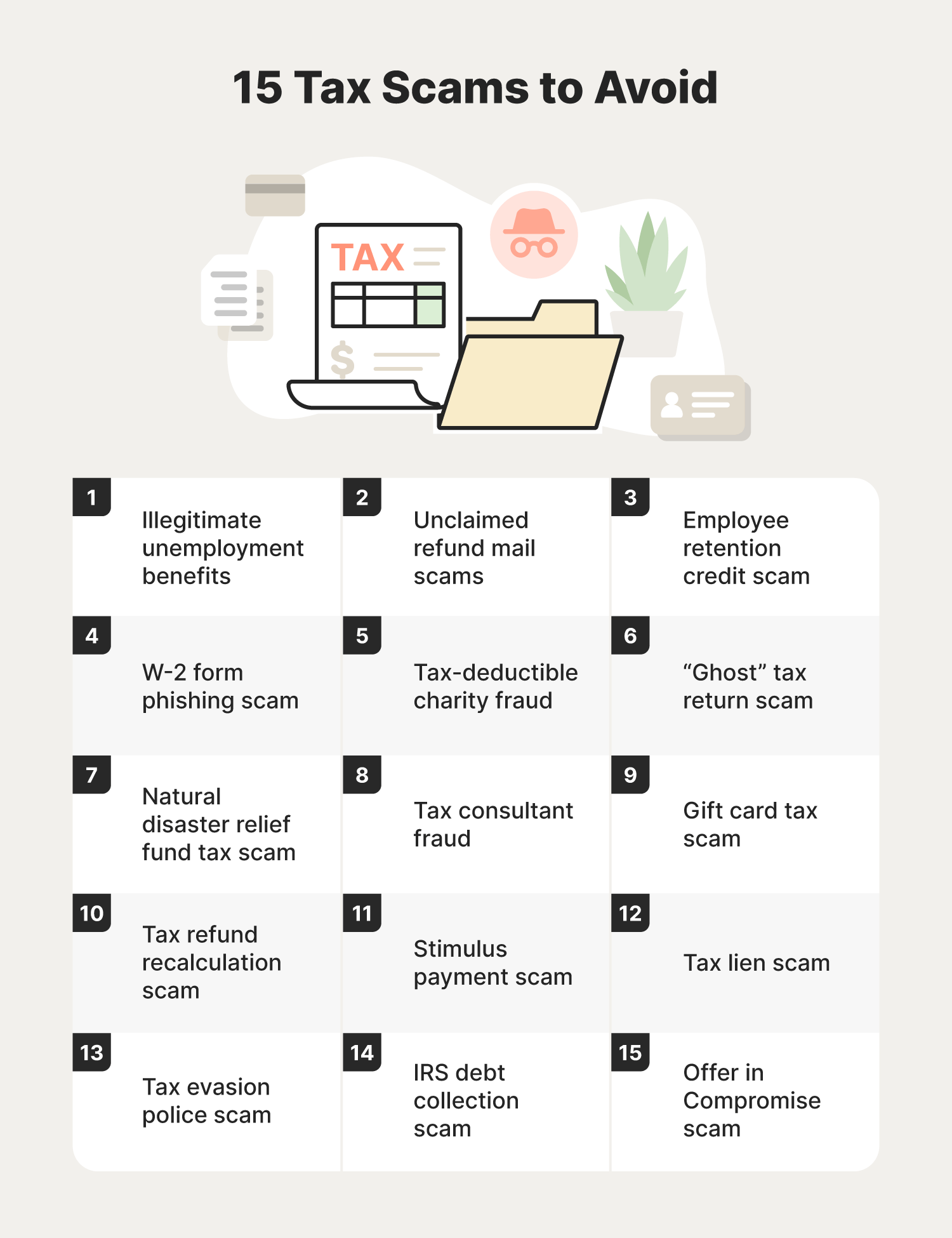

Recognizing the Risk of Tax Scams

As tax season approaches, it’s important to be aware of the rising threat of tax scams. Fraudsters often prey on young professionals and unsuspecting taxpayers, employing various tactics to steal money or personal information. Here’s how to recognize and protect yourself against these scams:

- Phishing Emails and Calls: Be cautious of unsolicited emails or phone calls claiming to be from the IRS or tax authorities. The IRS will never ask for sensitive information via email or phone. Always verify the authenticity by contacting the IRS directly.

- Fake Websites: Scammers may create websites that closely resemble the IRS or legitimate tax preparation firms. Always use trusted and verified links when filing your taxes or seeking assistance.

- Unrealistic Offers: Be wary of tax preparation services that promise unusually high refunds or “guaranteed” results. If it sounds too good to be true, it usually is.

It’s crucial to stay informed and vigilant against these threats. For further reading on identifying tax scams, check out the IRS’s official guidelines on this matter at Avoiding Tax Scams.

Image source: LifeLock

Image source: LifeLock

Conclusion: Taking Control of Your Taxes

Taking control of your taxes is essential for securing your financial future and maximizing your refund potential. By understanding the intricacies of tax deductions and credits, as well as implementing smart tax strategies, you can effectively navigate the complexities of the tax system and ensure that you’re making the most of your hard-earned income.

As a young professional, adopting proactive tax management practices is crucial. Here are several steps you can take to empower yourself when it comes to your taxes:

- Educate Yourself: Familiarize yourself with key concepts, such as tax deductions, tax credits, and tax brackets to make informed decisions. Resources like the IRS website are invaluable for understanding tax laws and updates.

-

Plan Ahead: Regularly assess your financial situation and plan your tax moves throughout the year rather than waiting until tax season. This can help you identify opportunities for deductions and credits.

-

Document Everything: Keep accurate and organized records of your income, expenses, and receipts. Utilizing digital tools can streamline this process, allowing for easier access when filing your taxes.

-

Consult a Tax Professional: Depending on your financial complexity, it may be beneficial to engage a tax advisor or CPA who can provide tailored advice and help you devise a strategy that maximizes your benefits.

Finally, remember that taxes are not just an obligation but also an opportunity. By taking control of your tax planning and utilizing the available resources, you can significantly enhance your financial well-being and pave the way for a brighter financial future. Start today by exploring the options available to you, and make your taxes work for you!