Why Financial Literacy is Essential for Teenagers

Image source: In Education Online

Image source: In Education Online

The Importance of Building Money Habits Early

Financial literacy is not just a beneficial skill; it’s an essential foundation for teenagers as they embark on their journey into adulthood. Building money habits early allows young individuals to develop a strong financial foundation that can lead to successful adult lives. Starting early gives teenagers the opportunity to experiment with different financial practices – like budgeting, saving, and investing – while mistakes are less costly.

By establishing healthy money habits at a young age, teenagers learn discipline and foresight. For example, managing an allowance or earnings from part-time jobs can teach them how to allocate money for needs versus wants, thereby fostering prioritization skills. Moreover, early engagement in financial topics can lead to increased confidence in making significant financial decisions later in life, such as buying a car or a home. By nurturing these skills now, teens are more equipped to avoid pitfalls like excessive debt and poor spending choices.

Resources such as the Jump$tart Coalition for Personal Financial Literacy provide valuable frameworks and tips for parents and educators to help instill these habits in teenagers. Empowering teenagers with these skills equips them to navigate a complex financial landscape with ease.

Understanding Financial Responsibility Before Adulthood

Understanding financial responsibility is critical as teenagers transition into adulthood. This knowledge provides them with the necessary tools to manage their finances effectively and make informed decisions. As teenagers prepare to enter college or the workforce, awareness of concepts like credit scores, interest rates, and financial planning becomes crucial.

For instance, many young adults underestimate the importance of maintaining a good credit history. By educating teenagers on how their financial actions impact their credit scores, they can make wise borrowing decisions when the time comes. Additionally, understanding the implications of student loans and personal debt will help them weigh options carefully and reduce financial strain in adulthood.

Teenagers should also grasp the significance of setting financial goals. Whether saving for a special purchase or planning for college, goal-setting fosters a mindset geared towards financial foresight. Encouraging them to start thinking about potential future expenses and savings as part of their everyday financial decision-making instills a sense of responsibility and planning.

This proactive approach can be bolstered with valuable information available from trusted institutions, such as the National Endowment for Financial Education (NEFE). By providing insights into budgeting, saving, and investing, these resources pave the way for a financially savvy generation prepared to take on adult responsibilities confidently.

Core Money Lessons Every Teenager Should Learn

Budgeting Basics: Managing Allowance or Part-Time Earnings

Learning the basics of budgeting is a cornerstone of financial literacy for teenagers. Whether managing an allowance from parents or income from part-time jobs, understanding how to track income and expenses is crucial.

- Track Your Income: Start by listing all sources of income. This usually includes allowances, babysitting, or other side jobs.

- Identify Expenses: Categorize spending into needs (like school supplies) and wants (like snacks or games).

- Allocate Funds: Use the 50/30/20 rule: 50% on needs, 30% on wants, and 20% for savings. This encourages a balanced approach, ensuring responsible spending while allowing for enjoyment and saving.

For more detailed guidelines on effective budgeting, check out this comprehensive resource from NerdWallet.

The Concept of Saving: Start Small, Think Big

Saving is not just about putting money aside; it’s about creating a mindset for financial growth. Start small by setting attainable savings goals.

- Establish a Savings Goal: This could be for a new gadget, clothes, or even a larger expense like a trip.

- Open a Savings Account: Once you have a steady amount saved, consider opening a bank account to maximize interest earnings.

- Automate Savings: If possible, automate transfers to your savings account. This reinforces the habit without requiring willpower.

By adopting these saving strategies early, teenagers can cultivate the habit of saving for the long term, as highlighted in this insightful article from Investopedia.

Understanding the Value of Money Through Spending Wisely

Understanding the value of money involves more than just knowing how much something costs. It’s about making informed choices regarding spending.

- Research Before You Buy: Encourage teens to compare prices and reviews before making purchases. This builds strong decision-making skills.

- Delay Gratification: Teach the importance of waiting before spending—sometimes the initial desire fades, leading to fewer impulse purchases.

- Budget for Fun: Allocate a fun budget for outings with friends. This teaches accountability while still enjoying life.

Making wise spending decisions can not only save money but also help discern what truly matters, reinforcing the importance of conscious consumerism.

An Introduction to Smart Investing for Beginners

Starting to invest early can be a game-changer for financial future. Here’s how teenagers can begin their journey into smart investing:

- Learn the Basics: Understand fundamental concepts such as stocks, bonds, and mutual funds. The more informed they are, the safer their investment choices will be.

- Start with a Mock Portfolio: Use platforms that allow simulations of investing without real money, helping teenagers to practice.

- Explore Investment Apps: Many apps are designed for beginners, allowing low-cost investments with educational tools to enhance understanding.

Even small investments can grow exponentially with time due to compound interest, as explained in this article from The Motley Fool.

Debt and Credit Cards: What Teens Need to Know

Understanding debt and credit cards is essential for any teen gearing up for adulthood. Here are some important points to consider:

- The Function of Credit Cards: Teach that credit cards can be a useful tool for building credit history but must be used wisely to avoid debt.

- Understanding Debt: Discuss the consequences of debt, such as interest rates and credit scores, and emphasize the importance of paying off balances in full each month.

- Know the Fees: Different credit cards come with various fees; understanding these aspects can prevent unnecessary spending.

It’s crucial to inform teens about responsible credit practices early on to help them avoid pitfalls later, supported by the guidelines available from Credit Karma.

Conclusion: Equipping Teenagers with Financial Knowledge

Financial literacy is pivotal for setting a secure future. By instilling essential money lessons during teenage years—budgeting, saving, wise spending, investing basics, and debt awareness—teens can navigate their financial landscapes with confidence and responsibility, paving the way for long-term success.

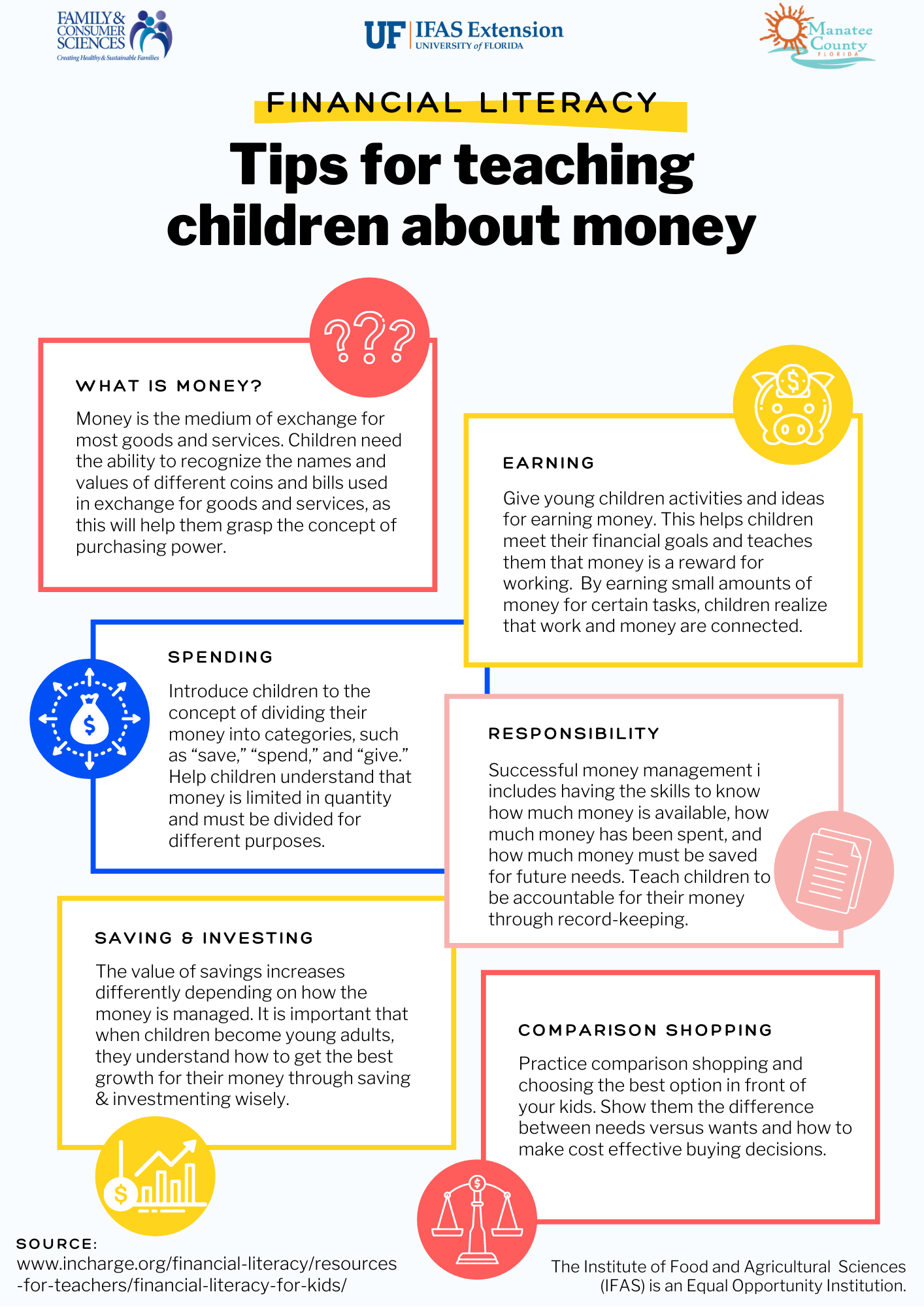

Practical Strategies for Teaching Financial Literacy to Teens

Image source: UF/IFAS Extension

Image source: UF/IFAS Extension

Using Real-Life Scenarios for Money Management Practice

Teaching financial literacy to teens can be greatly enhanced by incorporating real-life scenarios that provide practical experience. By simulating everyday financial situations, such as managing a household budget or planning a shopping trip, teens can learn how to apply mathematical concepts and critical thinking to real-world problems. For instance, role-playing scenarios can pressure-test their decision-making skills under different circumstances, like determining whether to buy a desired item now or save for something bigger in the future.

Moreover, you can initiate discussions around common situations teens face, like saving for a smartphone or a concert ticket. Engage them in conversations that require budgeting, comparing prices, and making spending decisions based on their financial goals. This approach not only solidifies their understanding of money management but also makes learning interactive and impactful.

If you seek additional resources to implement these activities effectively, check out Jump$tart Coalition for dynamic ideas and tools that support financial education.

Encouraging Goal-Setting to Inspire Financial Planning

Another effective strategy in teaching financial literacy is to encourage goal-setting among teens. Setting financial goals, whether short-term (like saving for a video game) or long-term (like funding a college education), helps teens understand the value of delayed gratification and gives them a sense of purpose when it comes to managing their finances.

Encourage teens to create a vision board that visually represents their financial goals. This could include images of items they want to buy, places they wish to visit, or other accomplishments. By regularly revisiting these goals and tracking their progress, teens will learn the importance of planning, saving, and budgeting effectively. This structured approach reinforces the direct correlation between their actions today and their financial future.

Consider leveraging tools and resources such as goal-setting worksheets or apps that help teens visualize their savings journey. For a comprehensive guide on financial goal-setting, the National Endowment for Financial Education provides valuable insights.

Leveraging Technology: Money Management Apps for Teens

In today’s technologically driven world, leveraging money management apps can significantly enhance the financial literacy of teens. Apps designed for budgeting, tracking expenses, or even simulating investment scenarios can make financial learning engaging and relatable.

Encourage teens to explore apps such as Mint, which helps users track their spending habits and budget effectively. Alternatively, apps like Qapital focus on savings through gamification, turning setting aside money into a fun challenge. Using these tools, teens can gain firsthand experience in managing their finances, understand their spending patterns, and learn important principles like saving and investing through user-friendly interfaces.

These technology solutions not only teach necessary skills but also accommodate the digital savviness of today’s youth, making the learning process enjoyable and worthwhile. Check out the comprehensive list of recommended apps available at NerdWallet.

Incorporating these practical strategies can build a solid foundation in financial literacy for teenagers, preparing them for responsible financial decision-making in adulthood.

The Long-Term Impact of Teaching Financial Skills Early

How Financial Literacy Builds Confidence and Independence

Teaching financial literacy to teenagers fundamentally changes their relationship with money, fostering a sense of confidence and independence that can last well into adulthood. As they learn the basics of budgeting, saving, and investing, teens begin to develop a healthier mindset towards finances. Understanding concepts such as managing expenses and planning for future purchases empowers them to make informed choices, providing them with a solid foundation.

Effective financial education does not merely lay the groundwork for more prudent spending; it also cultivates self-sufficiency. When teenagers grasp the implications of their financial decisions, they are less likely to rely on external sources like parents or loans for basic financial needs. This autonomy is crucial for their overall development, allowing them to make choices rooted in informed understanding rather than impulse.

Moreover, early exposure to financial responsibility builds resilience. As young individuals learn to navigate financial challenges, they build problem-solving skills, which are transferable to various aspects of life, including academics and career pursuits. By reinforcing these learning experiences, we help them cultivate an enduring confidence that benefits them across multiple domains. For a deeper exploration into the impact of financial literacy on self-confidence and independence, visit the National Endowment for Financial Education.

Setting the Foundation for Financial Stability in Adulthood

The groundwork laid during teenage years significantly influences financial stability in adulthood. Financial literacy prepares individuals to face the complexities of modern financial systems, equipping them with necessary skills like budgeting and investing. This preparation can lead to responsible financial behavior, such as avoiding crippling debt and making informed investment choices, ultimately resulting in long-term wealth accumulation.

For instance, individuals who learn the importance of saving early are more likely to establish emergency funds and contribute to retirement accounts consistently. This proactive approach can make a substantial difference in their financial resilience during unexpected life events, such as job loss or medical emergencies. Understanding the mechanics of interest and compounding also encourages smarter long-term savings habits, positioning them better for future financial opportunities.

Additionally, financial literacy fosters a mindset geared towards setting and achieving financial goals. This clarity in vision can lead to prudent decisions regarding education, home ownership, and retirement planning, establishing a cycle of financial well-being that benefits not only the individuals but also their families and communities. By investing in financial education for teenagers, we essentially invest in a more stable and prosperous future. For more insights into the importance of financial planning for adults, check out Investopedia.

Image source: Medium

Image source: Medium

Conclusion: Equipping Teenagers with Financial Knowledge

Equipping teenagers with financial knowledge is not merely an educational endeavor; it is a vital investment in their future. As we have explored throughout this article, understanding money management from an early age can have profound implications on a teenager’s financial literacy, confidence, and long-term stability.

The core financial lessons, such as budgeting, saving, and responsible spending, are crucial in fostering a sense of financial responsibility. When teenagers learn to manage their finances, they’re better prepared to face the challenges of adulthood. By instilling money habits early, we not only prepare them to make informed decisions but also empower them to take charge of their economic well-being.

Moreover, practical strategies like leveraging technology and using real-life scenarios can significantly enhance their understanding of financial concepts. Tools such as money management apps provide an engaging platform for teenagers to practice responsible spending and saving, making learning both enjoyable and effective. As these skills become ingrained, they lay a solid foundation for future independence and confidence.

In conclusion, the journey towards financial literacy is essential for teenagers, shaping not just their financial landscape but also their personal growth. As they navigate the complexities of money management, educators, parents, and mentors play a pivotal role in guiding them. By prioritizing financial education, we can ensure that the next generation is well-equipped to achieve financial stability and success.

For more in-depth information on the importance of financial literacy for youth, consider visiting Jump$tart Coalition, a high-trust resource dedicated to promoting financial literacy among students.