Key Person Insurance: Safeguarding Your Business from Uncertainty

In the world of business, the unexpected loss of a key individual can cause significant disruption. Whether it’s a founder, executive, or any employee whose expertise is vital to the success of the company, their absence can create financial instability. Key person insurance is a valuable tool to protect your business from such risks by providing financial security in the event of the loss of a key employee.

In this article, we’ll explore everything you need to know about key person insurance, including what it is, why it’s important, how it works, and how to choose the right policy for your business. Additionally, we will examine some real-life scenarios where key person insurance can be a lifesaver for businesses.

:max_bytes(150000):strip_icc()/keypersoninsurance.asp-final-8b538bb0719d4861ae2ebfcf53c898ad.png)

What is Key Person Insurance?

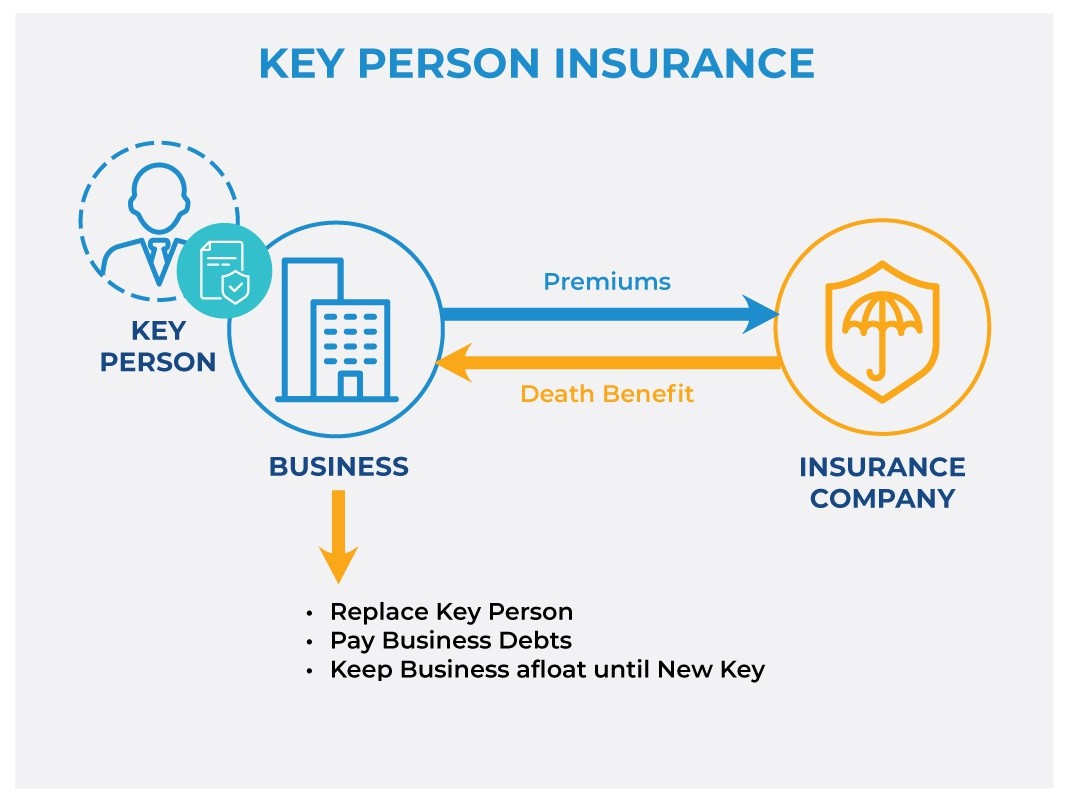

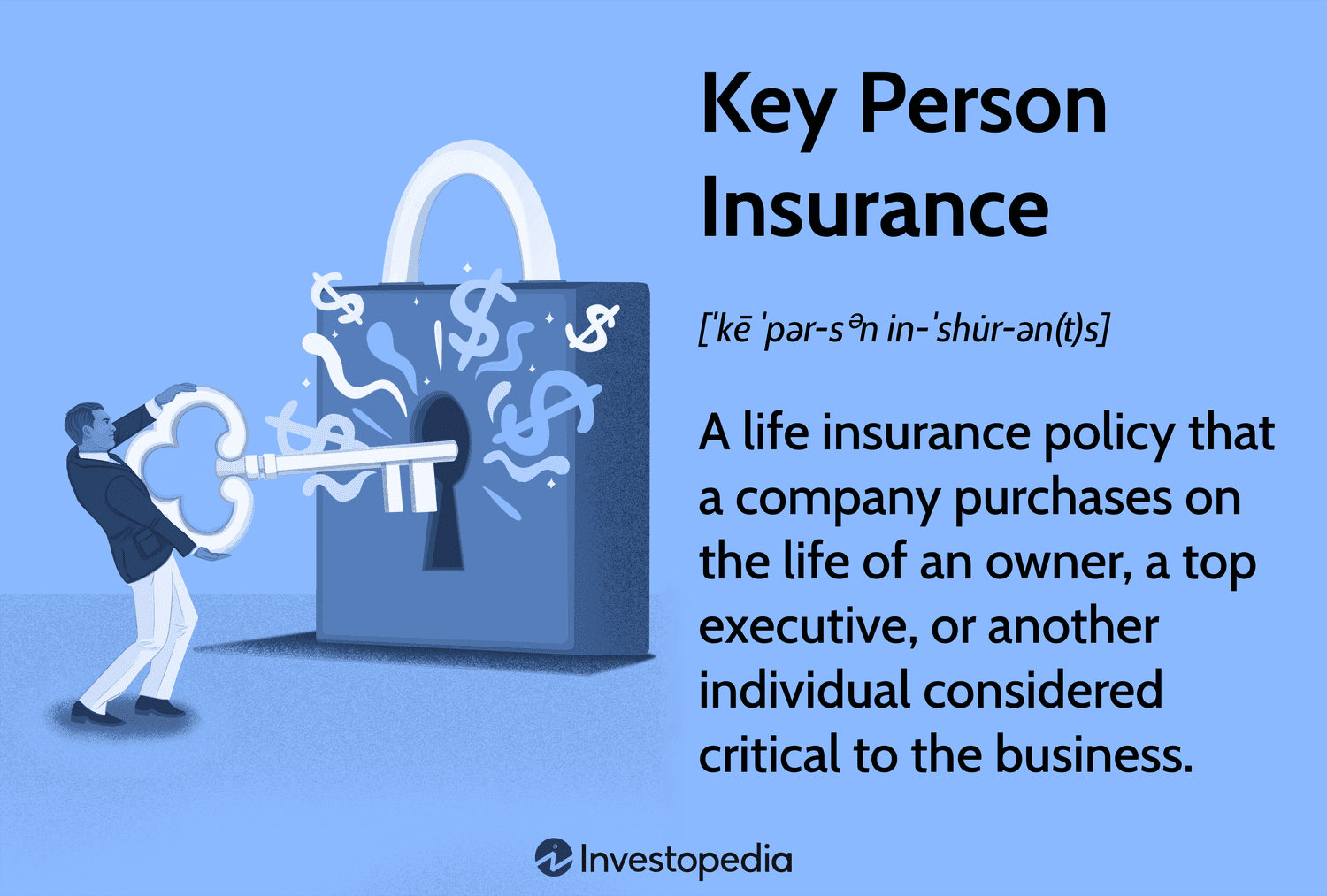

Key person insurance (also known as key man insurance) is a life insurance policy taken out by a business on the life of an individual crucial to the company’s operations. The company is the beneficiary of the policy, and in the event of the key person’s death, the company receives a lump sum payout. This payout can help cover the financial loss caused by the individual’s absence and ensure the company can continue to operate smoothly.

Who Is Considered a Key Person?

A key person is typically someone whose skills, experience, or leadership are critical to the success of the business. They may include:

- Founders or CEOs who drive the vision and direction of the company.

- Top salespeople who bring in a large portion of the revenue.

- Technical experts or engineers whose expertise is vital to the product or service.

- Managers or leadership team members whose strategic decisions directly impact the company’s growth.

For smaller companies or startups, the loss of even one employee can be devastating. For larger corporations, it may be a C-suite executive or a senior vice president.

Why Is Key Person Insurance Important?

Key person insurance serves as a safeguard for businesses against the unexpected death or disability of an essential team member. It can help in several ways:

1. Financial Stability During Transition

The sudden loss of a key person can cause financial strain as businesses may have to hire a replacement, reorganize, or delay operations. The insurance payout can cover these costs, enabling the company to maintain operations during the transition.

2. Preserving Company Value

Investors, lenders, and stakeholders often value companies based on their leadership team’s strength. If a key person dies unexpectedly, the company’s value may decline. Key person insurance can provide the capital needed to reassure stakeholders and preserve the company’s market value.

3. Managing Business Continuity

Without a key person, critical functions like decision-making, project management, and client relationships can come to a halt. The insurance payout can help maintain business continuity by giving the company financial resources to manage day-to-day operations while adjusting to the loss.

4. Debt Repayment

If the key person was responsible for generating income or securing loans for the business, their loss could result in significant debt. Key person insurance can be used to cover outstanding business loans or pay off creditors, reducing the financial pressure on the business.

How Does Key Person Insurance Work?

Key person insurance functions similarly to other types of life insurance, but the policy is purchased by the business rather than the individual. Here’s how it works:

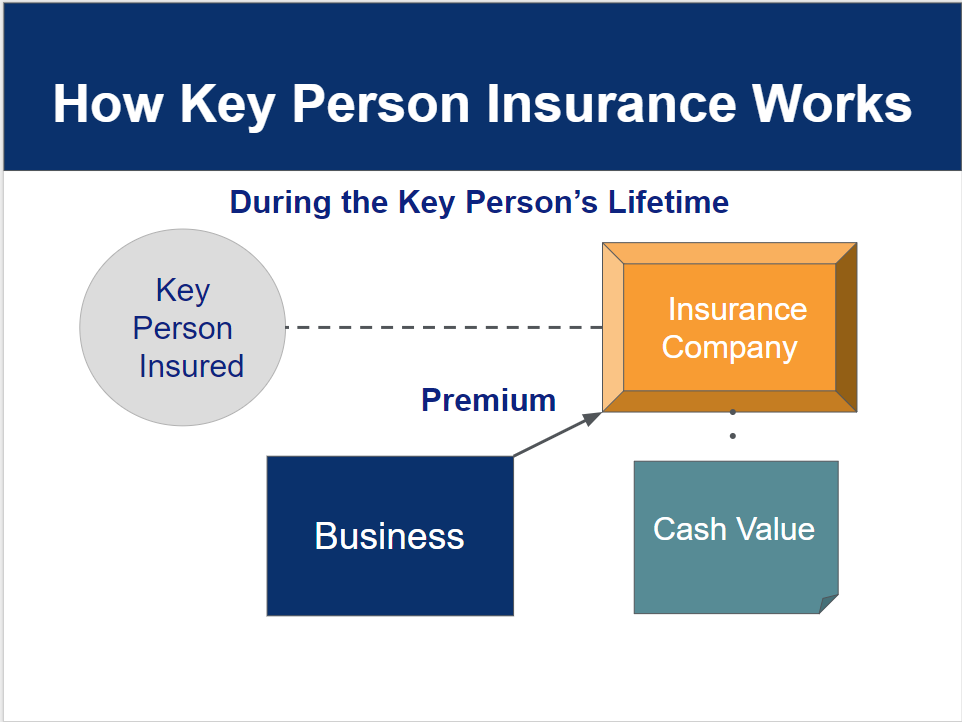

- Application Process: The company applies for life insurance coverage on the key person’s life. The business is the policyholder, pays the premiums, and is the beneficiary.

-

Premium Payments: Premiums are paid by the business, which can vary depending on the age, health, and role of the key person.

-

Payout: If the key person passes away, the insurance company pays the death benefit to the business. The company can then use the payout to cover financial losses, hire a replacement, or manage other business-related expenses.

Key Considerations When Purchasing Key Person Insurance

Before purchasing key person insurance, businesses should consider the following:

- Value of the Key Person: How much would the company lose if the key person were no longer around? This includes revenue loss, the cost of hiring a replacement, and the potential decline in company value.

-

Duration of Coverage: A startup may need key person insurance for the short term, while an established company may want it for a longer period.

-

Policy Type: There are two main types of key person insurance policies:

- Term Life Insurance: Provides coverage for a set number of years, typically 10 to 20 years. It’s often used for specific business purposes like securing a loan.

- Permanent Life Insurance: Provides lifelong coverage and includes a cash value component that can be used by the business as collateral or for other financial needs.

- Cost of the Premiums: Premium costs depend on several factors, such as the key person’s health, age, and the amount of coverage the business wants. The business must balance the cost of premiums with the value the insurance provides.

Choosing the Right Amount of Coverage

Determining the appropriate amount of coverage is crucial. If the coverage is too low, it may not provide enough financial protection. If it’s too high, the business may be paying for more insurance than it needs.

To calculate the right amount of coverage, businesses should consider:

- The key person’s role in generating income or managing major clients.

- The potential cost of hiring and training a replacement.

- The impact on the company’s financial stability and value.

Real-Life Scenarios for Key Person Insurance

Here are a few examples of businesses where key person insurance could be critical:

1. A Tech Startup

In a tech startup, the founder’s expertise and leadership are often crucial for the company’s survival. If the founder unexpectedly passes away, the startup might lose its direction, investor confidence, and customers. With key person insurance, the company can use the payout to hire a replacement and ensure business continuity.

2. A Family-Owned Business

In a family-owned business, the death of a key family member, like the CEO or business founder, can cause tension and instability. Key person insurance can provide the resources needed to manage the transition, secure the company’s assets, and buy time until a new leader can take charge.

3. A Law Firm

In law firms, senior partners or leading attorneys often generate a significant portion of the firm’s revenue. The loss of one of these individuals could result in a loss of clients and income. Key person insurance can mitigate the financial risk and ensure the firm’s stability during the transition period.

Frequently Asked Questions (FAQs)

1. How much key person insurance do I need?

The amount of coverage needed depends on the role of the key person and the financial impact their loss would have on the business. Consider the income they generate, the cost of hiring a replacement, and the potential disruption to the business.

2. Can I get key person insurance for more than one person?

Yes, a business can purchase key person insurance for multiple employees, especially if those individuals hold crucial roles in the company.

3. How long does it take to get key person insurance?

The application process for key person insurance can take several weeks, depending on the insurer and the health of the key person. However, once the policy is in place, it provides long-term protection.

4. Is key person insurance taxable?

The death benefit from a key person insurance policy is typically not taxable. However, the premiums paid by the business may not be deductible, as they are considered a business expense.

5. Can key person insurance be used for a business loan?

Yes, key person insurance can be used as collateral for a business loan. Lenders may require a business to have key person insurance to ensure they can repay the loan in case of the loss of an essential person.

Conclusion

Key person insurance is a vital tool that provides peace of mind to business owners, safeguarding their companies against the unexpected loss of a critical individual. Whether it’s a founder, CEO, or any essential employee, the financial payout from a key person insurance policy ensures that the business can weather the storm and continue operations smoothly.

If you’re considering purchasing key person insurance for your business, consult with a financial advisor or insurance specialist to determine the right coverage amount and policy type. By protecting your most valuable asset—your people—you’re investing in the long-term stability and success of your business.