IoT and Insurance: Revolutionizing the Industry with Smart Technology

The Internet of Things (IoT) has transformed nearly every industry, and insurance is no exception. IoT technology, which connects everyday devices to the internet, has brought about a new wave of innovation in the way insurers collect data, assess risk, and provide coverage. In the insurance industry, IoT has introduced smart solutions that enable better decision-making, personalized pricing, and faster claims processing.

In this article, we’ll explore how IoT is reshaping the insurance sector, the benefits it brings to both insurers and customers, and the types of IoT devices used in insurance today.

What is IoT and How Does it Relate to Insurance?

The Internet of Things (IoT) refers to the network of interconnected devices that can collect, share, and exchange data through the internet. These devices range from smart thermostats and wearables to connected cars and smart home devices.

In the context of insurance, IoT enables companies to gather real-time data, which helps them understand risk more accurately and provide tailored insurance policies. With IoT devices tracking everything from driver behavior to home security and even health metrics, insurers can offer more personalized products that reward good habits and reduce risks.

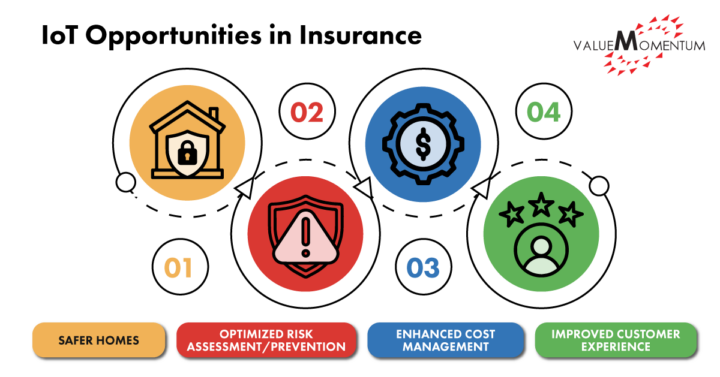

IoT and Insurance: Key Benefits

- Personalized Pricing: IoT enables insurers to create policies tailored to individual risk profiles by analyzing data from connected devices.

- Risk Mitigation: By tracking real-time data, insurers can spot potential risks before they escalate, reducing claims and improving loss prevention.

- Faster Claims Processing: IoT devices can automatically alert insurers of an incident (e.g., a car crash or home break-in), speeding up the claims process.

- Improved Customer Experience: IoT empowers customers with insights about their own behavior (e.g., safe driving habits), which can lead to lower premiums.

How IoT is Transforming the Insurance Sector

1. Connected Cars and Auto Insurance

The auto insurance industry is one of the most impacted by IoT technology. Telematics devices installed in vehicles collect data on driving behavior, including speed, braking patterns, and mileage. This data is then analyzed to provide usage-based insurance (UBI), which offers personalized premiums based on how safely someone drives.

- Pay-as-you-drive (PAYD): This model allows drivers to pay for their insurance based on the actual miles they drive, rewarding low-mileage drivers with lower premiums.

- Pay-how-you-drive (PHYD): Here, premiums are adjusted based on driving behavior, such as smooth acceleration and braking.

With connected cars, insurers can more accurately assess risk, reducing the likelihood of fraudulent claims and offering fairer premiums for safe drivers.

2. Smart Homes and Home Insurance

IoT devices in smart homes are another key area where insurers are leveraging technology. Devices such as smart thermostats, security cameras, and water leak detectors provide real-time data that can help prevent property damage or theft. For example:

– Smart thermostats can alert homeowners when temperatures drop to dangerous levels, potentially preventing pipe bursts.

– Security cameras and motion detectors help reduce the risk of theft and vandalism.

– Water sensors can notify homeowners of leaks, preventing costly water damage.

By collecting and analyzing this data, insurers can offer discounts or adjust premiums based on the level of risk associated with each home. Those with more advanced smart systems can receive lower premiums, encouraging further adoption of IoT devices for home protection.

3. Health and Life Insurance

Wearable devices, such as smartwatches and fitness trackers, are helping life insurers to gain insights into an individual’s health and activity levels. These devices track metrics like heart rate, steps taken, and calories burned. By offering health monitoring incentives, insurers can promote healthy behaviors among policyholders, which in turn can lead to reduced premiums for low-risk individuals.

For example:

– Wellness programs: Insurance companies may offer premium reductions or rewards for policyholders who meet fitness goals or track their health data through connected devices.

– Chronic condition management: IoT enables insurers to monitor and manage chronic conditions like diabetes or hypertension by tracking vital signs, leading to better health outcomes and lower insurance costs.

The Role of IoT in Claims Processing

One of the most impactful ways IoT is transforming the insurance industry is through claims processing. Traditionally, filing a claim involves a lengthy process that includes paperwork, inspections, and assessments. With IoT, this process can be streamlined, allowing insurers to receive real-time data that can automatically trigger claims.

For example:

– Connected cars can automatically report accidents to insurers, with data on the severity and location of the incident.

– Smart homes can send alerts when damage occurs, such as water leaks or fire detection, allowing insurers to quickly assess the situation and provide compensation without the need for an on-site inspection.

This integration of IoT into the claims process not only speeds up the resolution time but also reduces fraud, as the data from the connected devices provides a verifiable record of events.

Benefits of IoT in Claims:

- Faster claims resolution due to real-time data sharing.

- Reduced fraud through verifiable data and evidence.

- Lower administrative costs by automating parts of the claims process.

Challenges and Considerations of IoT in Insurance

While IoT holds immense promise for the insurance industry, there are still challenges to address:

1. Data Privacy and Security

The collection of vast amounts of personal data through IoT devices raises concerns about data privacy and security. Insurers must ensure that they comply with regulations such as the GDPR (General Data Protection Regulation) and HIPAA (Health Insurance Portability and Accountability Act) when handling sensitive information. Strong encryption, secure data storage, and transparency are crucial in maintaining customer trust.

2. Device Reliability

The reliability and accuracy of IoT devices are also a concern. If a device malfunctions or provides incorrect data, it could affect the accuracy of claims processing or risk assessment. Insurance companies must work with reliable manufacturers and continuously update their systems to ensure data integrity.

3. Consumer Adoption

While IoT devices are increasingly popular, not all consumers are ready to adopt them. There may be cost concerns, privacy fears, or simply a lack of understanding about how these devices benefit them. Insurers will need to invest in education and offer incentives to encourage customers to integrate IoT devices into their homes, cars, and personal health monitoring.

The Future of IoT in Insurance

As IoT technology continues to evolve, it will likely play an even larger role in reshaping the insurance industry. The future of IoT in insurance could include:

– Fully automated claims processing, where IoT devices automatically trigger claims based on data inputs, reducing human intervention.

– Dynamic pricing models that adjust premiums in real-time based on continuous data from connected devices.

– Advanced AI-driven analytics to better predict risk and offer more accurate pricing based on a person’s lifestyle, behavior, and health data.

FAQs About IoT and Insurance

1. What is IoT in insurance?

IoT in insurance refers to the use of connected devices such as smart cars, homes, and wearables that collect and transmit real-time data. This data helps insurers assess risk, offer personalized premiums, and streamline claims processing.

2. How does IoT affect insurance premiums?

IoT allows insurers to offer usage-based insurance (UBI) where premiums are based on real-time data. For example, safe driving or having smart home devices could lead to lower premiums.

3. What are the benefits of IoT in claims processing?

IoT improves claims processing by providing real-time data from connected devices, reducing fraud, speeding up claims resolution, and lowering administrative costs.

4. Is IoT data secure in insurance?

Data privacy and security are key concerns. Insurers must ensure they use secure methods to collect, store, and process data, following regulations like GDPR and HIPAA.

Conclusion

The integration of IoT technology in the insurance industry is unlocking new opportunities for both insurers and customers. By leveraging real-time data from connected devices, insurers can offer more personalized coverage, improve risk management, and streamline claims processing. While there are challenges related to privacy, security, and adoption, the future of IoT in insurance looks incredibly promising. With continuous advancements in IoT technology, the insurance landscape is set to become smarter, faster, and more efficient.

As IoT continues to evolve, we can expect insurance products to become more customized, providing greater value and peace of mind for consumers.