Image source: Simmons Bank

Image source: Simmons Bank

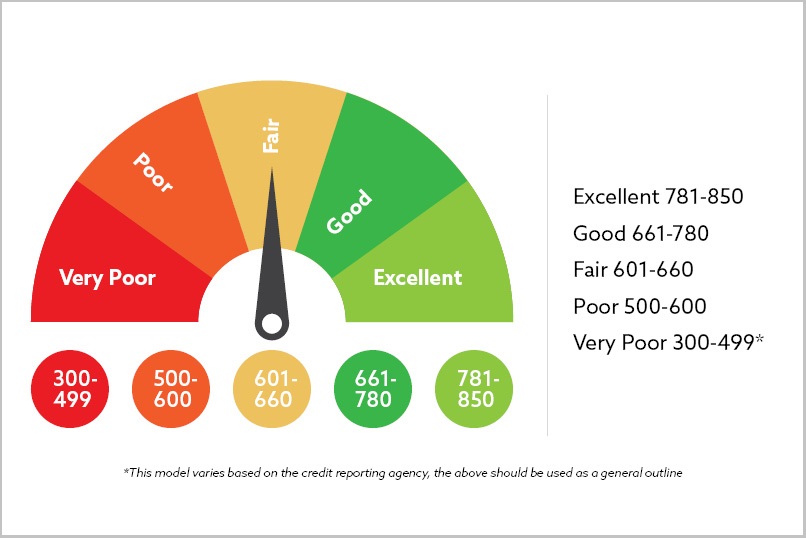

Why Your Credit Score Matters

The Importance of Credit Scores in Financial Decisions

Your credit score is more than just a three-digit number; it’s a crucial component of your financial health. Lenders, landlords, insurers, and even employers often rely on this score to make decisions that can significantly affect your financial future. Understanding the importance of your credit score can empower you to take control of your financial decisions.

- Loan Approval and Interest Rates: A higher credit score simplifies the loan approval process and results in lower interest rates for mortgages, car loans, and credit cards. For instance, individuals with excellent credit scores may qualify for interest rates that are substantially lower than those offered to individuals with poor credit scores. This can mean saving thousands of dollars over the term of the loan.

- Rental Applications: Landlords frequently check credit scores during the tenant selection process. A strong credit score can enhance your chances of being approved for a lease, while a lower score may lead to rejection or higher security deposits. This factor can make it more difficult to find suitable housing.

- Insurance Premiums: Many insurance companies use credit scores to determine premium rates for auto and homeowners insurance. A better credit score can lead to lower premiums, resulting in significant savings over time.

- Employment Opportunities: Some employers may review candidates’ credit scores as part of their hiring process, particularly for roles that involve financial responsibilities. A poor credit history can hinder job prospects in certain fields.

-

Negotiating Power: A strong credit score provides you with greater negotiating leverage when discussing terms with lenders and service providers. Those with better scores can often secure more favorable terms, from lower interest rates to higher credit limits.

In summary, being proactive about improving and maintaining a healthy credit score is vital for accessing various financial opportunities. Regularly monitoring your credit report, understanding the factors that influence your score, and addressing any inaccuracies can put you on the path to a stronger financial future. For further insights on how credit scores impact financial decisions, visit Investopedia.

Image source: DPS Network

Image source: DPS Network

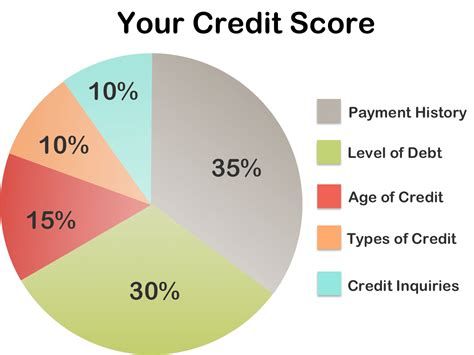

Payment History: The Key Driver of Credit Scores

Payment history is the most significant factor influencing your credit score, accounting for approximately 35% of most scoring models. Lenders want to know how reliably you pay back debt, which makes your track record crucial. Consistent on-time payments demonstrate to lenders that you are a responsible borrower. On the flip side, missed or late payments can severely impact your score, sometimes resulting in a drop of 100 points or more.

To maintain a strong payment history, it is critical to pay your bills on time, whether they are for loans, credit cards, or other financial obligations. Set reminders or automate payments when possible to help avoid late fees and damage to your credit standing. For further details on how payment history affects credit scores, refer to this comprehensive article from Experian.

Credit Utilization: How it Affects Your Rating

Credit utilization, or the ratio of your current credit card balances to credit limits, represents about 30% of your credit score. Keeping your credit utilization low indicates that you are not overly reliant on credit, which is a positive signal to lenders. A recommended benchmark is to keep your utilization below 30%—the lower, the better—for optimal impact on your score.

For example, if you have a total credit limit of $10,000, aim to keep your balance under $3,000. High utilization can not only affect your score but also could lead lenders to see you as a higher-risk borrower. Regularly monitoring your credit utilization can help you manage your scores effectively. For detailed strategies on maintaining a healthy credit utilization ratio, check out this resource from NerdWallet.

Length of Credit History and Its Impact

The length of your credit history contributes approximately 15% to your credit score. This factor considers how long your credit accounts have been active and how long it’s been since you used those accounts. In general, a longer credit history provides more data about your spending habits and payment behavior for lenders to evaluate.

While you can’t control the age of your oldest accounts, you can influence this factor by keeping older accounts open, even if they aren’t used frequently. Closing older accounts can shorten your average account age, which could negatively affect your score. To deepen your understanding of how the length of credit history impacts your credit score, consult this insightful article by Credit Karma.

In conclusion, understanding the factors that influence your credit score is essential for managing your financial health effectively. By focusing on payment history, credit utilization, and the length of your credit history, you can take active steps to improve your score and open up new financial opportunities in the future.

Step-by-Step Guide to Improve Your Credit Score in 6 Months

Image source: Cal Coast Credit Union

Image source: Cal Coast Credit Union

Step 1: Check and Review Your Credit Report

The first step in improving your credit score is to check and review your credit report. Everyone is entitled to one free credit report per year from each of the three major credit bureaus: Experian, TransUnion, and Equifax. You can obtain your reports at AnnualCreditReport.com.

Review your report for any errors or discrepancies. Negative information can stay on your report for up to seven years, so it is crucial to dispute inaccuracies promptly. If you find errors, follow the bureau’s process to dispute them. Maintaining a clean credit report can have a significant positive impact on your credit score.

Step 2: Pay Bills on Time Consistently

One of the most significant factors in your credit score is your payment history. To positively impact your score, commit to paying all your bills on time. Set up reminders or automate payments where possible. A single missed payment can remain on your credit record for up to seven years, potentially lowering your score by 100 points or more. Develop a budget that allows you to meet your obligations promptly and consistently.

Step 3: Reduce Outstanding Debt Strategically

To boost your score, focus on reducing your outstanding debt. Start by prioritizing high-interest debts, such as credit cards. Aim to lower your credit utilization ratio—preferably below 30% of your total available credit. Create a repayment plan that allocates a certain amount each month toward paying down your debts. Consistent payments will not only improve your credit utilization but also demonstrate responsible credit behavior.

Step 4: Avoid Opening Too Many New Credit Accounts

While it may be tempting to open new credit accounts, avoid doing so in rapid succession. Each application triggers a hard inquiry on your credit report, which can negatively impact your score. Instead, focus on maintaining your current accounts and improving your overall credit profile before applying for new credit. Consider spreading out any necessary applications over several months to mitigate the effects on your score.

Step 5: Keep Older Credit Accounts Open

The length of your credit history plays a role in determining your credit score. Older accounts contribute positively because they show stability. Even if you no longer use an old credit account, keep it open to maintain a longer average credit history. Just remember to make occasional small purchases to ensure the account remains active.

Step 6: Dispute Inaccuracies on Your Credit Report

If you spot any inaccuracies on your credit report, take action immediately by disputing them. Common issues include outdated information, incorrect account statuses, or even accounts that don’t belong to you. Use the guidelines provided by the credit bureaus for disputes, as they typically have 30 days to investigate claims. Clearing up inaccuracies can lead to a higher credit score over time.

In conclusion, by following these steps, you can systematically improve your credit score over the next six months. Each action taken adds up, leading to a more robust financial profile and greater opportunities for the future. For more resources and tips on managing your credit, visit Experian’s Credit Education.

Image source: FMG Suite

Image source: FMG Suite

Missing Payments or Paying Late

One of the most detrimental mistakes that can impact your credit score is missing payments or making them late. Payment history accounts for approximately 35% of your overall credit score, which means that timely payments are crucial. When you fail to pay a bill on time, it can lead to late fees, increased interest rates, and most importantly, a negative mark on your credit report.

To avoid these pitfalls, consider setting up automatic payments for your bills or using reminders on your calendar to track due dates. According to the Consumer Financial Protection Bureau, keeping your accounts in good standing and making payments on time can significantly enhance your credit profile. For more details, refer to this Consumer Financial Protection Bureau resource.

Maxing Out Your Credit Limits

Another common mistake that can harm your credit score is maxing out your credit limits. Your credit utilization ratio—which is the amount of credit you are using relative to your total available credit—plays a crucial role in determining your score. Ideally, keeping your credit utilization under 30% is recommended.

When you utilize too much of your available credit, lenders may perceive you as a higher risk, which can lead to a decrease in your credit score. To improve your credit utilization ratio, consider the following tips:

- Pay off balances regularly rather than waiting until the due date.

- Request a higher credit limit from your credit card issuer to improve your utilization ratio, as long as you don’t increase your spending.

- Spread out expenses over multiple cards to keep balances low on each one.

Being aware of your spending habits and managing your credit responsibly can help maintain a healthy credit score.

Applying for Too Many Loans Simultaneously

Lastly, applying for too many loans simultaneously can hurt your credit score. Each time you apply for credit, a hard inquiry is generated on your credit report, which can account for up to 10% of your credit score. Multiple inquiries in a short period can signal to lenders that you are in financial distress, potentially leading to lower creditworthiness in their eyes.

To minimize the impact of hard inquiries, consider these steps:

- Plan your credit applications rather than applying impulsively. Research and determine the best time to apply based on your financial circumstances.

- Limit applications to necessary ones. Ensure you genuinely need the loan or credit before proceeding with an application.

- Shop within a specific time frame. If you’re rate shopping for mortgages or auto loans, make your applications within a short period (usually 30 days) to limit the effect on your credit score.

By being mindful of your credit activity, you can protect your score from unnecessary drops and maintain a solid financial reputation.

How Improved Credit Scores Open Up Financial Opportunities

Image source: Welch State Bank

Image source: Welch State Bank

Lower Interest Rates on Loans and Credit Cards

One of the most significant benefits of having a high credit score is the access to lower interest rates on loans and credit cards. Lenders view individuals with higher scores as less risky, which often results in reduced borrowing costs. For example, a person with a credit score of 720 may receive a lower interest rate compared to someone with a score of 580.

This difference can translate to substantial savings over time. For instance, consider a $20,000 car loan: at a low-interest rate of 3% versus a high-interest rate of 8%, the total interest paid over five years could differ by thousands of dollars. This can significantly affect your monthly budget, allowing you the financial flexibility to invest or save towards your future goals. Learn more about how credit scores impact loan rates at The Balance.

Better Approval Chances for Renting or Mortgages

When searching for a new home or an apartment, your credit score can play a crucial role in the approval process for renting or obtaining a mortgage. Landlords and mortgage lenders utilize your credit history to evaluate your ability to make timely payments. With a higher credit score, your chances of securing a lease or mortgage significantly improve.

For example, mortgage lenders may require a minimum credit score of 620 to qualify for conventional loans, while lower scores could lead to either rejection or higher down-payment requirements. By maintaining a strong credit score, potential renters and homebuyers can access a wider array of options, including more competitive rental agreements and mortgage products. This not only broadens your choices but also potentially puts you in a better position to negotiate favorable lease terms or mortgage rates.

Enhanced Negotiating Power with Creditors

Another advantage of having an improved credit score is the increased negotiating power it gives you with creditors. When vendors or lenders see a high credit score, they may be more willing to offer you better terms. This includes lower rates for credit cards, better payment plans, and even waiving late fees or penalties.

Moreover, if you’re struggling with high-interest debt, a good credit score can enable you to negotiate a lower interest rate or even consolidate debt into a payment plan with more favorable terms. This can lead to significant financial relief and pave the way for improved financial health. For additional insights on negotiating strategies with creditors, check out NerdWallet.

In summary, an improved credit score opens up numerous financial opportunities, such as lower interest rates, increased rental and mortgage approval chances, and enhanced negotiating power with creditors. Taking active steps to improve your credit score not only positions you for success today but also sets the stage for a more secure financial future.

Conclusion: Take Control of Your Financial Future

In today’s increasingly competitive financial landscape, taking control of your financial future is more crucial than ever. A good credit score not only opens doors to lower interest rates but also enhances your chances of loan approvals and strengthens your bargaining power with creditors. Having a solid understanding of what drives your credit score can empower you to make informed financial decisions.

As you reflect on your financial practices, consider the following strategies to improve your credit score and pave the way for better opportunities:

- Regular Monitoring: Review your credit report regularly to ensure its accuracy and catch any discrepancies early on. You can obtain a free copy of your credit report from AnnualCreditReport.com.

- Timely Payments: Cultivating the habit of paying bills on time can significantly affect your payment history, which is the most influential factor in your credit score.

- Debt Management: Systematically reduce your debt and avoid maxing out your credit limits, as credit utilization plays a significant role in your rating.

- Limit New Applications: Be mindful of how often you apply for new credit, as multiple inquiries can negatively impact your score.

By implementing these practices, you can gradually elevate your credit profile, positioning yourself for a more secure financial future. Remember, the journey to excellent credit is a marathon, not a sprint. Invest the time and effort necessary to cultivate your financial health, and the rewards will undoubtedly follow.

In conclusion, take control of your financial future today by prioritizing your credit health. For further insights and detailed tips on understanding and improving your credit score, refer to the resources available on Consumer Financial Protection Bureau to enrich your knowledge and empower your decision-making process.

Image source: Welch State Bank