Why Getting Out of Debt Quickly is Important

Image source: Lantern by SoFi

Image source: Lantern by SoFi

The Financial Burden of Debt

The financial burden of debt can profoundly impact your life. Individuals drowning in debt often experience a cascade of problems stemming from late fees, elevated interest rates, and the stress of managing multiple payment schedules. According to a report by the Federal Reserve, household debt in the United States reached $16.5 trillion in the third quarter of 2023, further emphasizing the urgency of addressing this issue. This persistent financial strain can hinder your ability to build savings, invest in opportunities, or even maintain a healthy credit score.

To illustrate, let’s consider a person with credit card debt. If the total amount owed is $10,000 with an interest rate of 20%, they face not only the inability to utilize those funds but also the risk of accruing significant additional costs over time. Thus, prioritizing debt repayment can lead to substantial savings and financial liberation. By addressing debt immediately, you can free yourself from the endless cycle of payments and fees, enabling you to redirect your finances towards goals like home ownership or retirement. For more information, you can explore the Federal Reserve’s latest economic data.

The Emotional and Mental Impact of Debt

The emotional and mental impact of debt is often overlooked but can manifest in numerous detrimental ways. The stress associated with owing money can lead to anxiety, depression, and a constant sense of worry. Many individuals report feeling overwhelmed by their financial obligations, which can detract from their overall quality of life. According to the American Psychological Association, money is one of the leading sources of stress for adults in the United States.

The pressure of debt can also affect relationships and diminish your overall well-being. It’s not uncommon for discussions about finances to lead to tension and conflict. This emotional toll often discourages individuals from seeking solutions, creating a vicious cycle that can prolong their financial struggles. Therefore, getting out of debt quickly is not merely a financial decision but a crucial aspect of ensuring emotional health as well. Individuals who manage to pay off their debt tend to report higher levels of happiness and improved mental clarity, reflecting the importance of tackling debt head-on.

By recognizing the substantial emotional weight of debt, you can better appreciate the urgency of creating a solid plan for debt elimination. This proactive approach is essential not only for financial stability but also for enhancing personal well-being, allowing you to enjoy life without the heavy burden of financial insecurity.

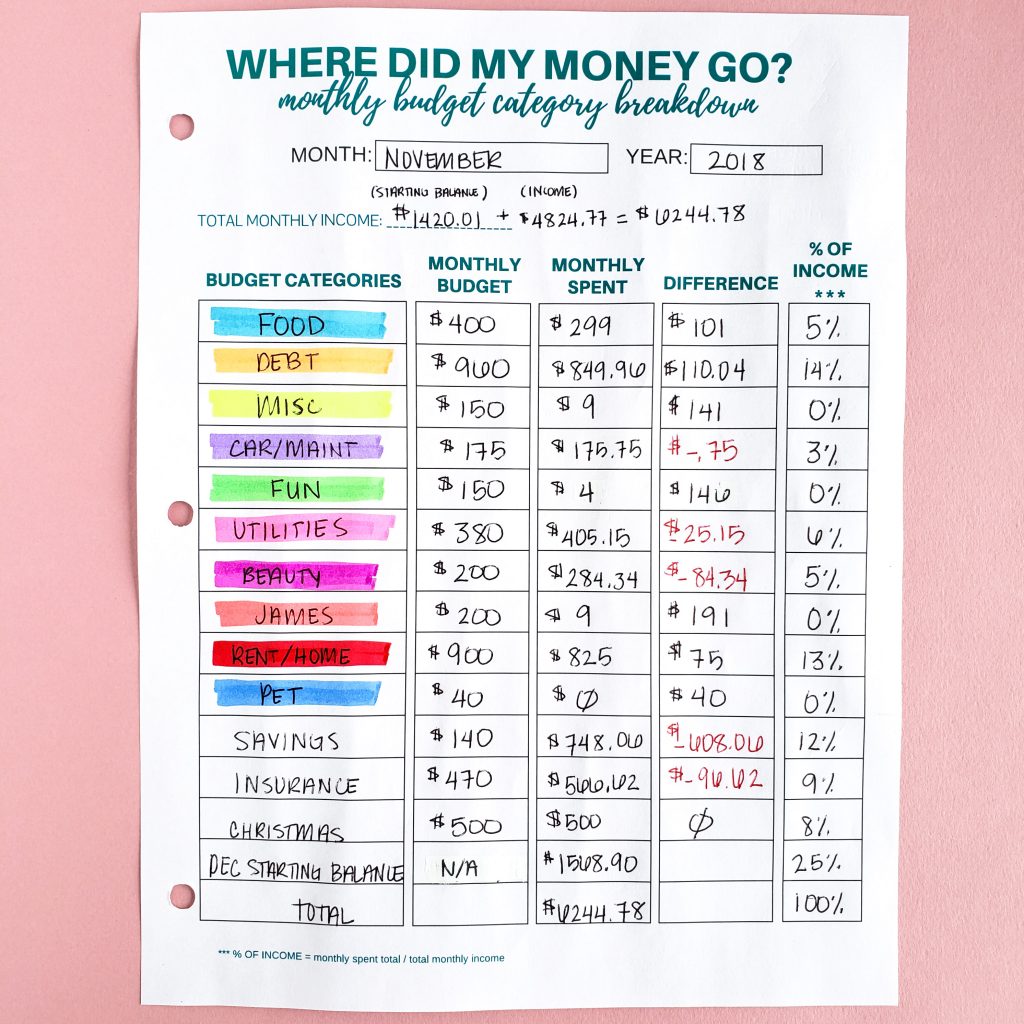

Step 1: Assess Your Financial Situation

Image source: IFEC

Image source: IFEC

List All Your Debts and Interest Rates

To effectively tackle your debt, the first step is to list all your debts alongside their corresponding interest rates. This creates a clear view of your financial obligations and identifies which debts require urgent attention. Start by gathering monthly statements from your creditors.

Consider creating a simple spreadsheet or document that includes the following:

- Name of the creditor

- Total amount owed

- Interest rate (APR)

- Minimum monthly payment

- Due date

Organizing this information will help you prioritize your debts. For example, debts with higher interest rates should typically be prioritized to minimize total interest paid over time.

Additionally, if you’re unsure of your interest rates or need detailed information, reputable sources like the Consumer Financial Protection Bureau (CFPB) can guide you on understanding your rights and responsibilities regarding debt management.

Understand Your Monthly Budget

The second crucial aspect of assessing your financial situation is to understand your monthly budget. Knowing your income and expenses allows you to see how much money you can allocate towards debt repayment. Follow these steps to gain clear insight into your budget:

- Track Your Income: Document all sources of income including salaries, bonuses, and side hustles.

- List Monthly Expenses: Include all fixed (rent, utilities) and variable expenses (groceries, entertainment).

- Identify Discretionary Spending: Highlight areas where you can cut back to free up more cash for debt repayment.

By calculating the difference between your total income and total expenses, you can see how much money is left (or how much is needed). This calculation will guide your decisions moving forward, ensuring you maintain control of your financial situation.

Utilizing budgeting tools or apps, such as Mint or YNAB (You Need a Budget), can simplify this process. These tools help you visualize your spending habits and identify areas for potential savings, further assisting in your journey to becoming debt-free.

Image source: The Budget Mom

Image source: The Budget Mom

Assessing your financial situation is a vital first step that equips you with the necessary insights to devise a tailored debt repayment strategy. By being aware of your debts and understanding your monthly budget, you are laying the groundwork for a solid financial future.

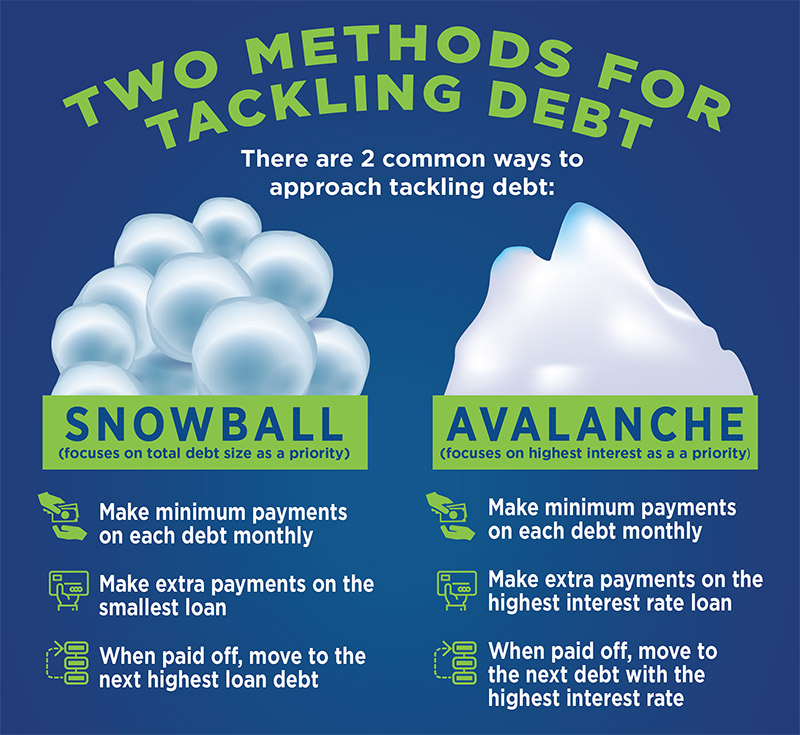

Step 2: Choose a Debt Repayment Strategy

Debt Snowball Method: Paying Smallest Balances First

The Debt Snowball Method is a popular strategy designed to help you eliminate debt efficiently and psychologically. The approach involves listing your debts from smallest to largest, regardless of the interest rates. You focus on paying off the smallest debt first while making minimum payments on the others. Once the smallest debt is cleared, you move on to the next smallest.

This method’s power lies in its psychological benefits. Successfully paying off smaller debts provides you with quick wins, motivating you to tackle larger debts. As you eliminate each debt, you redirect the payments you were making to the smaller debt towards the next one, creating a “snowball” effect.

Image source: CRCU

Image source: CRCU

Debt Avalanche Method: Prioritizing Higher Interest Debts

On the other hand, the Debt Avalanche Method takes a more mathematical approach by focusing on debt with the highest interest rates first. You list your debts from highest to lowest interest rate and prioritize paying off the high-interest debts while making minimum payments on the others.

This method can save you money in interest over time, as you eliminate the most costly debts first. However, it may take longer to see significant progress in reducing the number of debts, which can be demotivating for some individuals.

Choosing the Avalanche Method is beneficial if you are focused on minimizing overall interest payments and can handle the longer wait for psychological victories.

Which Strategy is Right for You?

Deciding between the Debt Snowball and Debt Avalanche methods depends on your personality and financial situation. Here are some considerations:

- If you need motivation: If you struggle with discouragement or need quick wins to stay motivated, the Debt Snowball method may be more suitable.

- If you’re disciplined: If you can stay focused without needing immediate gratification, the Debt Avalanche method can save you the most money in the long run.

- Consider mixed strategies: Some individuals find success using a combination of both methods, focusing on a few small debts to build momentum while still prioritizing high-interest debts.

Ultimately, there is no one-size-fits-all answer. Exploring both strategies allows you to find the best fit for your personal financial journey. For additional insights on these methods, consider reading from reliable sources, such as Investopedia.

Make sure to review your financial situation and choose a strategy that aligns with your goals and emotional needs. Achieving control over your debts requires both strategy and perseverance, but with the right approach, you can pave the way to financial freedom.

Step 3: Cut Unnecessary Expenses

How to Identify Unnecessary Expenses

Identifying unnecessary expenses is crucial in your journey towards financial freedom and debt repayment. Start by examining your monthly budget to pinpoint areas where you can easily cut back. Here are some steps to help you identify those expenses:

- Track Your Spending: Utilize budgeting tools or apps that allow you to track every dollar spent for at least one month. This will give you a clear picture of your spending habits.

- Categorize Your Expenses: Break down your expenses into essential and non-essential categories. Essentials include housing, utilities, and groceries, while non-essentials might cover dining out, subscriptions, and luxury purchases.

- Review Your Subscriptions: Check for subscriptions or memberships you no longer utilize. Whether it’s streaming services or gym memberships, canceling unused subscriptions can lead to significant savings.

- Assess Lifestyle Choices: Consider lifestyle changes that could reduce costs. For instance, cooking at home instead of dining out not only saves money but can also be healthier.

- Be Mindful of Small Expenses: Small purchases, like daily coffee runs or snacks, can add up quickly. Evaluate whether these daily treats are worth the sacrifice in your overall budget.

Remember, the aim is to cultivate a mindset of financial awareness. By utilizing resources from reputable sites like The Balance, you can gain further insights on identifying unnecessary expenses and effective budgeting strategies.

Image source: InCharge Debt Solutions

Image source: InCharge Debt Solutions

Redirecting Savings Toward Debt Repayment

Once you’ve identified and cut down on unnecessary expenses, the next smart move is to redirect those savings toward your debt repayment strategy. Here’s how to make this transition effective:

- Allocate Savings Wisely: Determine how much you have saved by cutting expenses and decide on a portion to allocate towards your debt. Even small contributions can add up and significantly shorten repayment time.

- Make Extra Payments: Use your newfound savings for extra payments on your debts. Consider focusing on the debt with the highest interest rate first or following the debt repayment method that suits you best (debt snowball or avalanche).

- Create an Emergency Fund: It might be tempting to use all your savings for debt, but having a small emergency fund (around $500 to $1,000) can prevent you from accumulating more debt in unforeseen situations.

- Set Up Automatic Transfers: To ensure you stick to your plan, set up automatic transfers from your checking account to your debt account. This strategy helps maintain consistent payments.

- Monitor Progress: Keep track of your reduced debt balance and celebrate milestones along the way. Regularly reviewing your accomplishments reinforces the motivation to stay on course.

By taking these strategic steps, you can ensure that every dollar saved is working towards a debt-free future. Being proactive in managing your expenses reflects a commitment to transforming your financial situation for the better.

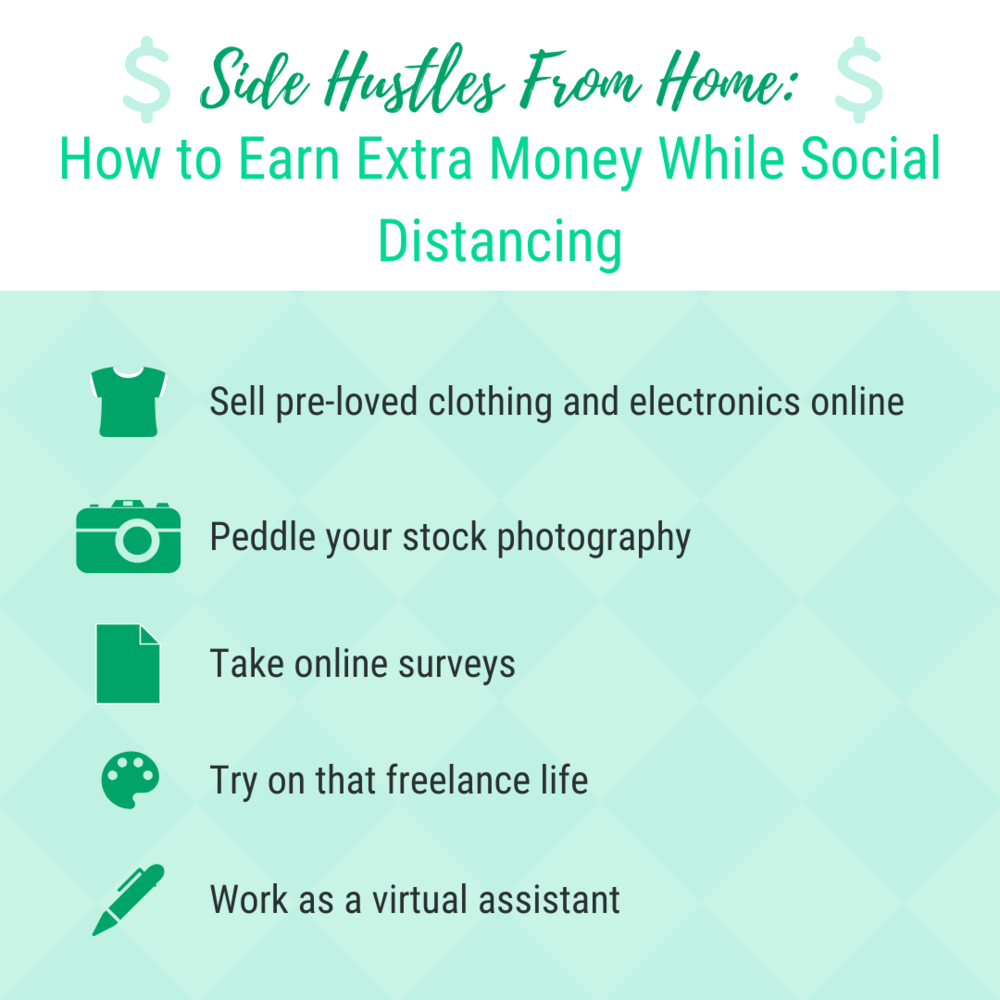

Step 4: Increase Your Income

Side Hustles to Earn Extra Money

In today’s gig economy, side hustles have become an increasingly popular and viable way to supplement your income. Engaging in side projects can not only help you pay off debt faster but also provide you with the financial cushion you need for unexpected expenses. Here are a few side hustle ideas to consider:

- Freelance Work: Utilize your skills in graphic design, writing, or coding on platforms like Upwork and Fiverr. These platforms allow you to find clients quickly and set your own rates.

- Online Tutoring: If you’re proficient in a subject area, consider online tutoring. Services like Chegg Tutors or VIPKid allow you to teach students from the comfort of your home.

- Delivery Services: Companies like Uber Eats, DoorDash, and Postmates offer opportunities to earn money by delivering food or groceries, often on your own schedule.

These side hustles provide flexible working conditions, enabling you to manage your time effectively while significantly increasing your income. For more insights on profitable side hustles, consider reading this article from Forbes on the best side jobs to boost your earnings.

Image source: Squarespace

Image source: Squarespace

Selling Unused Items for Quick Cash

Selling items you no longer need is an effective way to generate quick cash. Whether it’s old electronics, clothing, or furniture, there are various platforms that make it easy to sell your unused items:

- eBay: List items for auction or fixed prices, targeting a wide audience. Ensure you take clear photos and write accurate descriptions to attract buyers.

-

Facebook Marketplace: A local selling platform that connects you directly with buyers in your community, allowing for face-to-face transactions.

-

Poshmark: Perfect for selling clothing and accessories, Poshmark allows you to manage sales directly through their app.

These sales not only declutter your living space but also yield extra money that can be allocated towards paying off your debts. To delve deeper into maximizing your sales, check out this article on Good Housekeeping about how to sell your stuff online efficiently.

Negotiating Your Salary or Finding a Better Job

Negotiating your salary is often overlooked, yet it is an effective way to boost your income significantly. Here are some strategies to prepare for successful salary negotiations:

- Do Your Research: Understand the market rate for your position and experience level. Websites like Glassdoor and Payscale provide valuable data on industry salary standards.

-

Prepare Your Pitch: Highlight your achievements and contributions to your company. Articulating your value can make a compelling case for a salary increase.

-

Don’t Hesitate to Walk Away: Being willing to consider job offers elsewhere can give you leverage in negotiations. Sometimes, simply expressing interest in other opportunities can motivate your current employer to offer a better salary.

If you’re currently unhappy at your job, consider exploring job-search platforms like LinkedIn or Indeed, which allow you to find new opportunities that may offer better salaries and benefits.

Implementing these strategies can lead to an increase in your income, ultimately supporting your goal of paying off debt faster.

Step 5: Stay Consistent and Track Progress

Celebrate Small Wins

As you embark on your debt repayment journey, celebrating small wins becomes crucial. Recognizing and rewarding yourself for each milestone—whether it’s paying off a single debt or hitting a savings target—can boost your morale and perseverance. Small victories instill a sense of accomplishment and reinforce the belief that your goals are achievable.

Consider implementing a reward system for yourself. For example:

- Treat Yourself: After paying off a minor debt, indulge in a small treat. This could be as simple as a favorite dessert, a movie night, or even a day out.

- Share Your Progress: Celebrate milestones with friends or family who support your journey. Their acknowledgment can significantly elevate your motivation.

- Create a Vision Board: Visualizing your goals and celebrating each step can keep you excited about the process.

Tracking your progress not only helps you stay accountable but also empowers you to see how far you’ve come. You might consider using apps like Mint or YNAB (You Need a Budget) to help you monitor your debts and expenses, making it easier to celebrate when you achieve those small wins. For more insights on how to celebrate progress effectively, check out this article from NerdWallet.

How to Keep Yourself Motivated

Maintaining motivation while tackling debt can sometimes feel overwhelming. Here are some strategies to keep your spirits high during your repayment journey:

- Set Clear Goals: Define specific, measurable, achievable, relevant, and time-bound (SMART) goals. For instance, aim to pay off a certain amount within a set period. This clarity can be extremely motivating.

-

Stay Informed: Educate yourself on personal finance. Understanding how crushing debt can affect your future and learning about the benefits of financial freedom can keep your motivation alive. Books such as “The Total Money Makeover” by Dave Ramsey or blogs like The Budget Mom offer substantial insights.

-

Create Accountability: Share your financial journey with others. Consider joining a support group or engaging with communities online (like forums or social media pages dedicated to financial freedom). Knowing that others are walking a similar path can inspire you to stay consistent.

-

Visualize Your Debt-Free Life: Imagine the benefits of being debt-free—like financial security, reduced stress, and the ability to pursue your dreams. Maintaining a clear vision of your future self can serve as a strong motivating factor.

-

Reflect on Your Achievements: From time to time, take a moment to review your progress. Reflecting on where you started compared to where you are now can provide the boost you need to keep going.

Staying consistent and tracking your progress may be challenging, but the rewards of financial freedom are well worth it. Celebrate the journey as much as you celebrate the destination. Don’t hesitate to create a supportive environment that continually motivates you to achieve your financial goals.

Common Mistakes to Avoid When Paying Off Debt

Relying Too Much on Credit While Paying Down Debt

One of the most prevalent mistakes individuals make when attempting to pay off debt is relying too much on credit. It may seem convenient to use credit cards, especially when unexpected expenses arise, but this behavior can significantly impede your debt repayment progress.

Using credit while trying to pay off existing debt can lead to an endless cycle of borrowing, known as “debt stacking.” Instead of reducing your outstanding balances, each new charge adds to the amount you owe, prolonging your journey to financial freedom. Furthermore, it often results in accruing additional interest, which can create a larger financial burden than originally anticipated.

Instead of reaching for a credit card, consider utilizing a dedicated savings account for emergency expenses or small, unexpected costs. Building this fund helps you avoid the temptation to use credit and allows you to manage your expenses effectively without accruing more debt. For a detailed understanding of the impact of credit under these circumstances, take a look at this comprehensive guide on credit card management from NerdWallet.

Not Having an Emergency Fund

Not having an emergency fund is another critical mistake when tackling debt. Life is unpredictable, and unexpected expenses can arise at any time, whether that’s a medical bill, a car repair, or a job loss. Without an emergency fund, you may find it all too easy to revert to credit options to cover these costs, which once again can spiral your finances out of control.

An emergency fund serves as a financial safety net, allowing you to address unforeseen expenses without jeopardizing your debt repayment efforts. Financial experts usually recommend saving three to six months’ worth of living expenses. Over time, this fund provides peace of mind and stability, enabling you to focus entirely on reducing your debt without the fear of sudden costs.

Creating an emergency fund doesn’t have to be overwhelming; starting small and gradually increasing your contributions can make it more manageable. For more detailed steps on establishing and maintaining an emergency fund, visit The Balance.

“By avoiding these common mistakes, you can streamline your debt repayment strategy and work towards a debt-free life more efficiently.”

Conclusion: Take Control of Your Financial Future

Final Thoughts on How to Get Out of Debt Quickly

In conclusion, taking control of your financial future is essential for achieving lasting peace of mind and a more secure lifestyle. Successfully getting out of debt quickly involves a proactive approach that requires perseverance, strategic thinking, and commitment. Here are some final insights to guide you on your journey to financial freedom:

- Assess Your Financial Situation: Start by understanding the full extent of your debt. Create a comprehensive list of all your debts and their respective interest rates. This will help you prioritize which debts to tackle first.

-

Choose the Right Repayment Strategy: Whether you opt for the Debt Snowball Method, focusing on paying off the smallest balances first, or the Debt Avalanche Method, which prioritizes higher interest rates, choose a strategy that resonates with your personal habits and motivations.

-

Cut Unnecessary Expenses: Take a hard look at your monthly budget and identify any expenditures that can be trimmed. Redirect those savings towards your debt repayment, which can substantially accelerate your path to being debt-free.

-

Increase Your Income: Look for side hustles or part-time opportunities that can supplement your income. Selling unused items can also provide a quick financial boost, aiding in faster debt repayment.

-

Stay Consistent and Track Your Progress: Regularly monitor your debt repayment journey. Celebrate small wins and milestones. This can keep you motivated and reinforce your commitment to financial independence.

-

Avoid Common Mistakes: Be mindful of pitfalls such as relying too much on credit and neglecting the importance of an emergency fund. Both can derail your progress and reinforce a cycle of debt.

Getting out of debt does not merely alleviate financial stress; it empowers you to make better financial decisions in the future. You’ve taken the first step towards financial security—now it’s crucial to stay the course. For more in-depth financial strategies and guidance, consider exploring resources available at NerdWallet, which provides a wealth of information on managing debt effectively.

Taking control of your financial future starts today. Embrace these strategies, remain steadfast in your efforts, and enjoy the liberation that comes from financial independence.