Home Buying & Mortgages: A Comprehensive Guide for First-Time Buyers

Purchasing a home is one of the most significant financial decisions you’ll make in your lifetime. It’s essential to understand the home buying process and the various mortgage options available to you. This comprehensive guide will help you navigate the complexities of home buying and ensure you make informed decisions throughout the process.

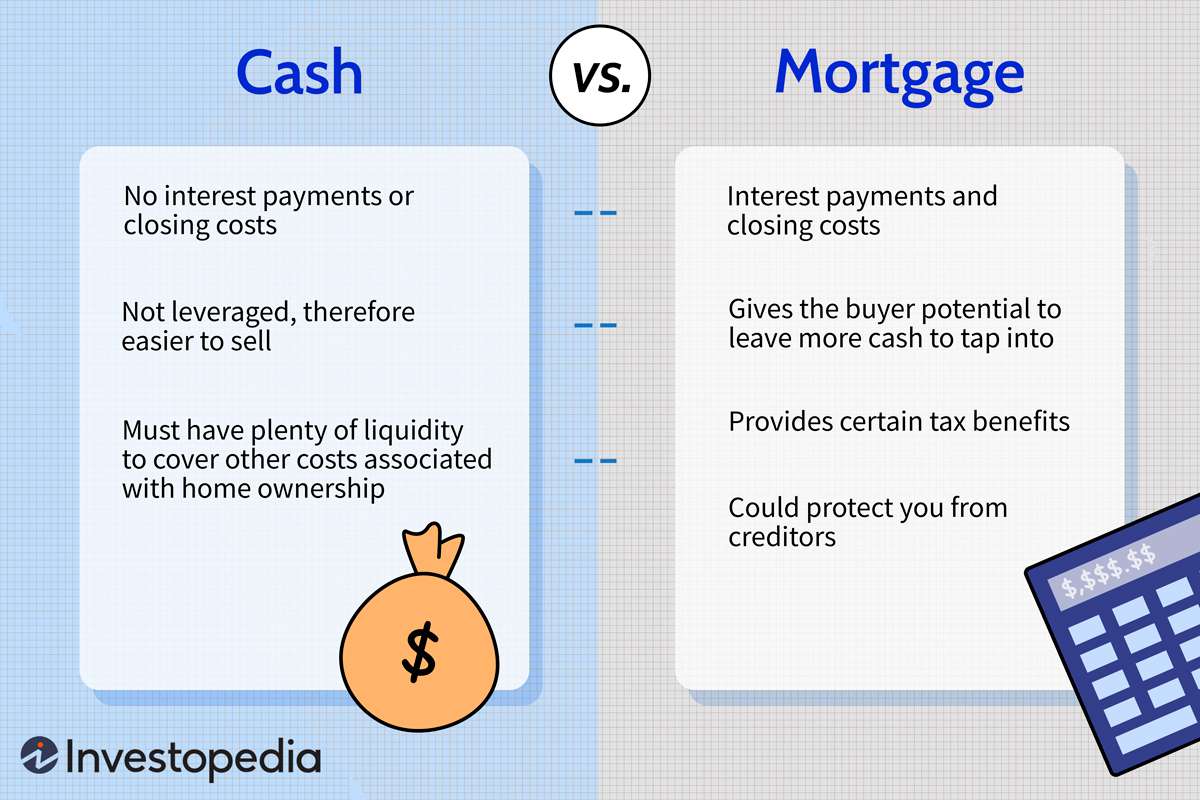

:max_bytes(150000):strip_icc()/dotdash-111214-buying-home-cash-vs-mortgage-v2-325bbfe3ca7343ca904ecaa9d2cb6c67.jpg)

Understanding the Home Buying Process

Buying a home is not just about finding a place to live; it’s a multifaceted journey that requires careful planning and preparation. Here’s a breakdown of the steps you should take to ensure a smooth process.

1. The Importance of Financial Readiness

Before you start house hunting, it’s crucial to assess your financial readiness. This includes evaluating your income, savings, and credit score. A strong financial foundation is essential for securing a mortgage and making a competitive offer.

Assessing Your Financial Situation

- Credit Score: Your credit score plays a significant role in determining your mortgage rates. Generally, a score of 700 or higher will qualify you for better rates. You can check your credit score for free through services like AnnualCreditReport.com.

-

Savings: Aim to save at least 20% of the home’s purchase price for a down payment. This can help you avoid Private Mortgage Insurance (PMI) and reduce your monthly payments.

Creating a Budget for Home Buying

Establish a realistic budget that considers not only the purchase price of the home but also additional costs such as closing costs, moving expenses, and ongoing maintenance.

2. Researching the Real Estate Market

Understanding the current real estate market is essential for making informed decisions.

Understanding Market Trends

Stay informed about local housing market trends, such as average home prices, inventory levels, and market demand. Websites like Zillow and Realtor.com provide valuable insights.

Finding a Real Estate Agent

A knowledgeable real estate agent can be your greatest ally in the home buying process. Look for an agent with a good track record in your desired area. They can guide you through the process, negotiate on your behalf, and help you avoid common pitfalls.

Types of Mortgages

When it comes to financing your home purchase, understanding the different types of mortgages is crucial. Each type has its own set of benefits and drawbacks.

1. Fixed-Rate Mortgages

A fixed-rate mortgage offers a consistent interest rate and monthly payments throughout the life of the loan, typically 15 to 30 years. This predictability can be beneficial for budgeting.

Benefits and Drawbacks

- Benefits: Stability in payments and protection against interest rate increases.

- Drawbacks: Typically, fixed-rate mortgages have higher initial interest rates compared to adjustable-rate mortgages.

2. Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) feature interest rates that may change periodically based on market conditions. Initially, ARMs often have lower rates compared to fixed-rate mortgages.

How They Work

An ARM typically starts with a lower initial rate for a specified period (e.g., 5, 7, or 10 years) before adjusting annually based on market indexes.

3. Government-Backed Loans

Government-backed loans are designed to help first-time homebuyers and those with lower credit scores. They include:

- FHA Loans: Insured by the Federal Housing Administration, these loans require a lower down payment and are accessible to buyers with lower credit scores.

- VA Loans: Available for veterans and active military members, VA loans offer favorable terms, including no down payment and no PMI.

- USDA Loans: For buyers in rural areas, USDA loans provide low-interest financing with no down payment required.

:max_bytes(150000):strip_icc()/mortgage-69f02f04cdae4863806bd0455255106e-f66e51c6b85445cf8e1aa396c1b56c50.png)

The Mortgage Application Process

Once you’ve chosen a home, it’s time to navigate the mortgage application process. Understanding the steps involved can help you prepare effectively.

1. Pre-Approval vs. Pre-Qualification

Before making an offer on a home, it’s wise to obtain a mortgage pre-approval. This process involves a lender evaluating your financial situation and providing a written estimate of how much you can borrow.

- Pre-Approval: A more thorough process that provides a conditional commitment from a lender.

- Pre-Qualification: An informal estimate of your borrowing capacity based on self-reported financial information.

2. Required Documentation

During the application process, you will need to provide several documents, including:

- Income Verification: Recent pay stubs, tax returns, and W-2 forms.

- Credit History: Lenders will pull your credit report to assess your creditworthiness.

By following these steps and understanding the types of mortgages available, you’ll be well on your way to successfully navigating the home buying process. Stay tuned for the second half of this guide, where we’ll delve into closing the deal and provide essential tips for first-time buyers.

Closing the Deal: What to Expect

Once you’ve secured your mortgage and found your dream home, the next step is to close the deal. Understanding the closing process will help you feel more confident and prepared.

1. Understanding Closing Costs

Closing costs can range from 2% to 5% of the home’s purchase price and may include:

- Loan Origination Fees: Fees charged by the lender for processing the loan.

- Title Insurance: Protects against any legal claims on the property.

- Appraisal Fees: Costs for an appraisal to determine the home’s market value.

- Inspection Fees: Charges for a professional inspection of the home’s condition.

Be sure to request a Loan Estimate from your lender, which will outline these costs clearly.

2. The Closing Process

The closing process typically involves several steps:

- Review Closing Documents: Before the closing meeting, review all documentation, including the Closing Disclosure, which provides detailed information about your loan and closing costs.

-

Final Walk-Through: Conduct a final walk-through of the property to ensure that everything is in order before you officially take ownership.

-

Closing Meeting: During this meeting, you will sign various documents, including the mortgage agreement and other necessary paperwork. Be prepared to pay any closing costs that are due at this time.

-

Receive Keys: Once all documents are signed and payments are made, you will receive the keys to your new home!

Homeownership: The Responsibilities That Come with It

Congratulations! You are now a homeowner. However, with homeownership comes a variety of responsibilities that you must manage to maintain your property and its value.

1. Maintenance and Repairs

Home maintenance is crucial to ensuring the longevity of your investment. Regular upkeep can prevent larger, more costly repairs in the future. Here are some essential tasks:

- Regular Inspections: Schedule annual inspections for your roof, plumbing, and HVAC systems.

- Routine Maintenance: Keep up with seasonal maintenance tasks, such as gutter cleaning and HVAC servicing.

2. Understanding Your Mortgage

It’s vital to understand the terms of your mortgage to manage your payments effectively. Make sure you:

- Know Your Interest Rate: Understand whether you have a fixed or adjustable-rate mortgage and how your payments may change over time.

- Consider Refinancing Options: If interest rates drop or your credit improves, refinancing your mortgage could save you money in the long run.

Frequently Asked Questions (FAQs)

What is the difference between pre-approval and pre-qualification?

Pre-approval is a more formal process that involves a lender assessing your financial situation and providing a written commitment for a loan amount. Pre-qualification is an informal estimate based on self-reported financial information.

How much should I save for a down payment?

Aim for at least 20% of the home’s purchase price. However, many loan programs allow for lower down payments, such as 3.5% for FHA loans.

What are some common closing costs I should expect?

Closing costs may include loan origination fees, title insurance, appraisal fees, and inspection fees. These typically range from 2% to 5% of the home’s purchase price.

Tips for First-Time Homebuyers

As a first-time homebuyer, here are some essential tips to keep in mind:

- Stay Within Your Budget: Avoid stretching your finances too thin. Stick to your budget to ensure you can manage mortgage payments and other expenses comfortably.

-

Don’t Rush the Process: Take your time to research and find the right home. Rushing could lead to buyer’s remorse.

-

Consider Future Needs: Think about your long-term plans. Will this home accommodate your future needs, such as a growing family or a home office?

Conclusion

Buying a home is an exciting journey filled with opportunities and responsibilities. By understanding the home buying process, familiarizing yourself with mortgage options, and preparing for the responsibilities of homeownership, you’ll be well-equipped to make informed decisions.

Whether you are just starting to think about buying a home or are ready to make an offer, remember that knowledge is your greatest asset. For further reading, consider checking out resources like NerdWallet for tips and advice tailored to your specific needs.

With careful planning and the right information, you can navigate the home buying process with confidence and ease. Good luck on your journey to homeownership!