Why Health Insurance Is Essential for Young Adults

Understanding the Importance of Early Coverage

Health insurance is not just a luxury; it is a necessity for young adults stepping into the world of independence. Many young adults often overlook the importance of securing health coverage, mistakenly believing that their youth will protect them from serious health issues. However, accidents and illnesses can occur unexpectedly, making early coverage essential.

Having health insurance at a young age allows individuals to access necessary preventive care, which is crucial for maintaining long-term health. According to the Centers for Disease Control and Prevention (CDC), preventive services like vaccinations, screenings, and annual check-ups are vital for early detection and management of potential health issues. By utilizing these services, young adults can avoid extensive medical costs in the future and promote overall well-being.

Furthermore, investing in health insurance early can yield lower premiums. Insurance companies often base costs on age and health status; hence, the younger you start, the less you pay. This proactive approach not only safeguards your health but also positions you for financial benefits over time.

Image source: cdn.prod.website-files.com

Image source: cdn.prod.website-files.com

Protecting Your Finances with Health Insurance

One of the most compelling reasons to obtain health insurance as a young adult is financial protection. Medical emergencies can lead to unexpected bills that may overwhelm even the best-laid financial plans. According to a report from the Kaiser Family Foundation, nearly 25% of young adults aged 18-29 reported difficulty paying medical bills in the past year. Without insurance, these costs can spiral out of control and result in significant debt.

Health insurance mitigates these financial risks by covering a substantial portion of medical expenses. For example, an unexpected visit to the emergency room for treatment of a sports injury could cost thousands of dollars. However, with adequate health coverage, you would only be responsible for a copay or certain deductibles, making the situation far more manageable.

Moreover, health insurance often provides access to essential mental health services. In an age where mental wellness is prioritized, having coverage ensures that young adults can seek professional help without the looming fear of exorbitant costs. This holistic assurance of mental and physical health not only fosters overall well-being but empowers young adults to thrive in every aspect of their lives.

In summary, early coverage through health insurance is a strategic investment in both health and financial security for young adults. From facilitating access to preventive care to offering financial protection during medical emergencies, the benefits far outweigh the costs. You can learn more about the importance of health insurance and find resources through the HealthCare.gov website, which offers tailored advice on navigating insurance options.

Image source: image.isu.pub

Image source: image.isu.pub

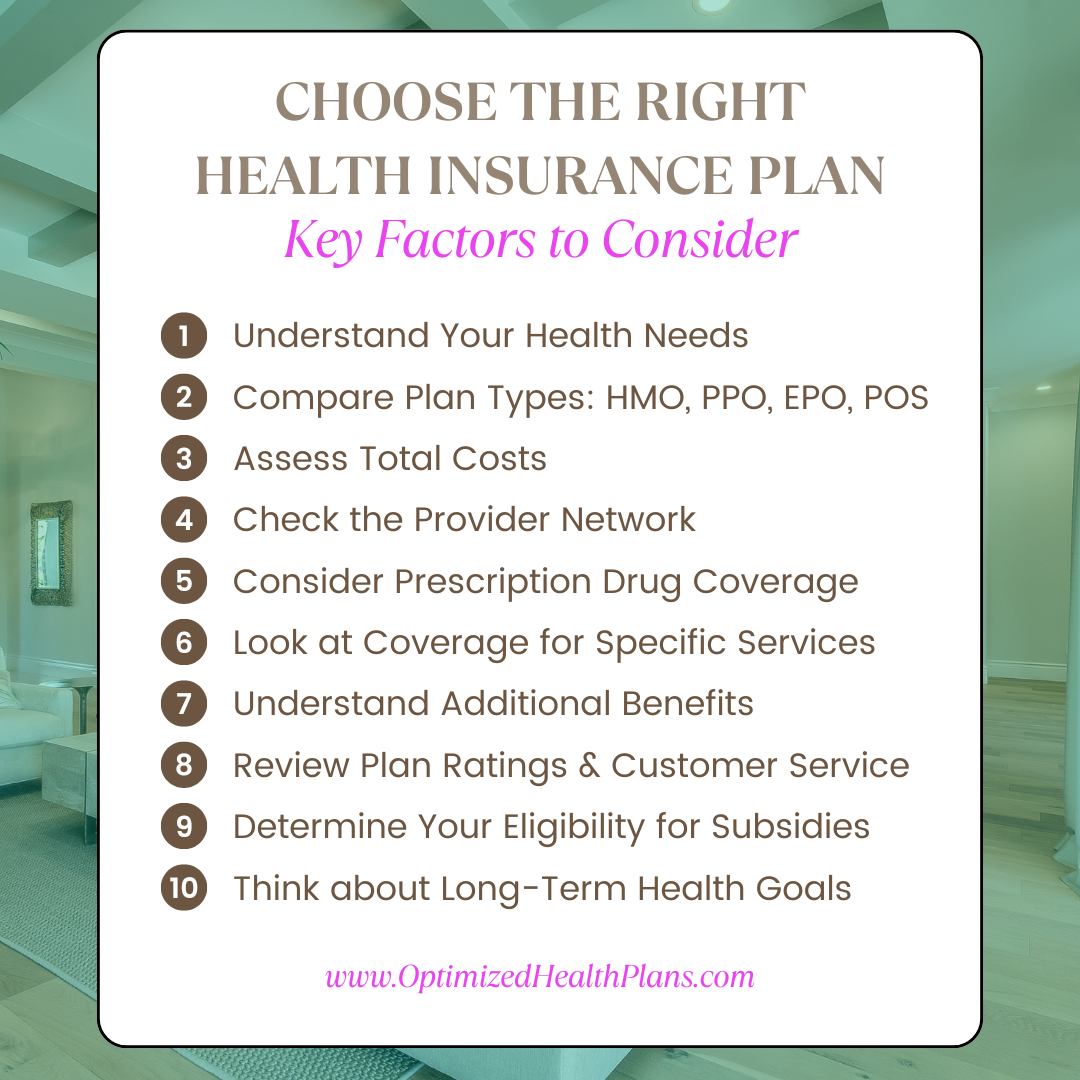

How to Choose the Right Health Insurance Plan

Image source: Optimized Health Plans

Image source: Optimized Health Plans

Assess Your Personal Healthcare Needs

Choosing the right health insurance plan starts with a thorough assessment of your personal healthcare needs. Consider the following factors:

- Current Health Status: Are you generally healthy, or do you have ongoing medical conditions? Understanding your health status will guide you in selecting a plan that covers necessary treatments and medications.

- Frequency of Medical Visits: How often do you typically visit healthcare providers? If you rely on frequent check-ups or specialist visits, you should prioritize plans with lower co-payments and extensive networks.

- Future Health Considerations: Are you planning to start a family, or do you anticipate needing specific medical services in the near future? Anticipating these needs can help ensure your plan accommodates potential changes in your healthcare usage.

To dive deeper into assessing your healthcare needs, you can refer to HealthCare.gov, which provides various tools and resources.

Understand Key Insurance Terms (Premiums, Deductible, etc.)

To navigate the complexities of health insurance, it’s essential to understand key insurance terms:

- Premium: This is the amount you pay for your health insurance coverage, typically billed monthly. It’s crucial to choose a premium that fits within your budget without compromising necessary coverage.

- Deductible: This is the amount you’ll need to pay for your healthcare before your insurance begins to cover costs. Plans with lower deductibles often have higher premiums, and vice versa.

- Co-payments and Co-insurance: Co-payments are fixed amounts you pay for specific services (like doctor visits), while co-insurance is a percentage of the cost of care that you pay after meeting your deductible.

- Out-of-Pocket Maximum: This is the highest amount you will pay in a plan year before your insurer covers 100% of your healthcare expenses. Understanding this term can help you limit your financial risk.

Being clear on these terms can help you compare plans effectively and choose one that aligns with your financial situation and healthcare needs.

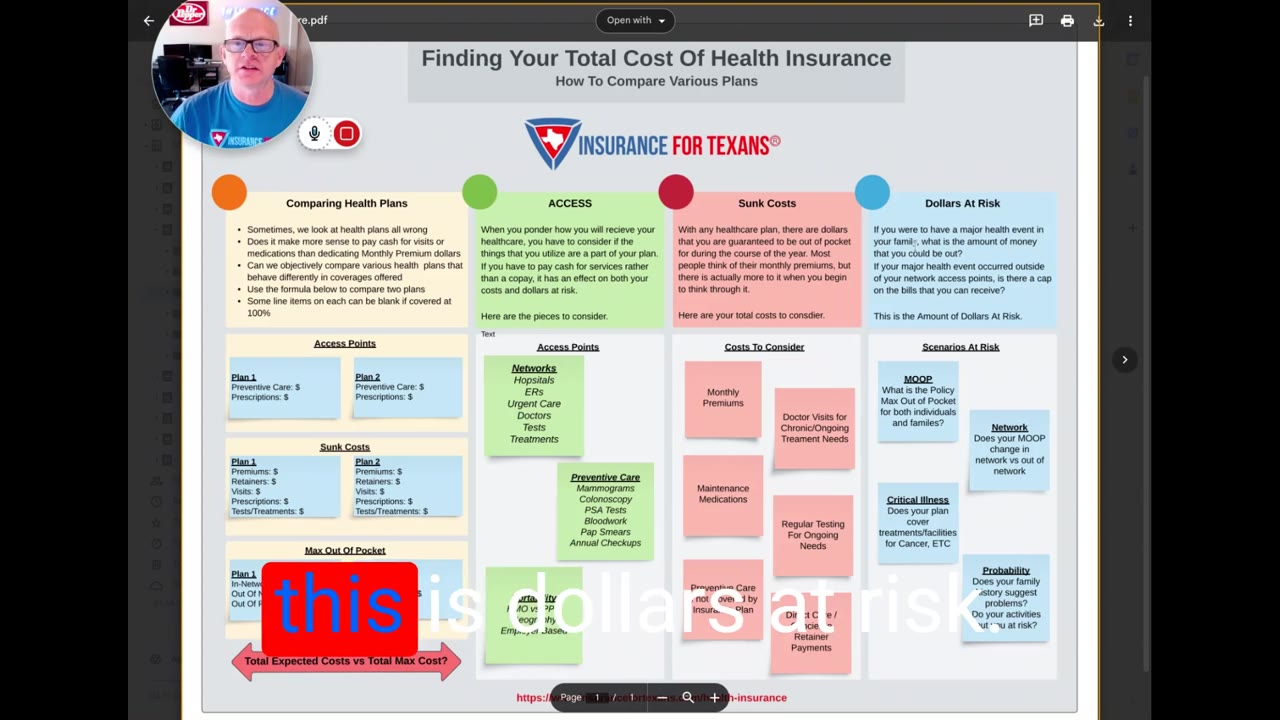

Compare Plans Based on Coverage and Network

Once you assess your healthcare needs and understand key insurance terms, it’s time to compare health insurance plans based on coverage and network:

- Coverage Options: Evaluate what services are covered under each plan. Look for essential services like preventive care, hospitalization, mental health services, and prescription medications. Ensure the plan meets your specific health needs.

- Provider Network: Investigate whether your preferred doctors and specialists are within the plan’s network. Going out of network can lead to higher costs, so it’s crucial to select a plan that features a broad range of providers that meet your needs.

- Additional Benefits: Some plans may offer extra perks such as wellness programs, fitness memberships, or telehealth services, which can be valuable as you consider your long-term health and lifestyle.

Image source: Insurance For Texans

Image source: Insurance For Texans

By taking the time to analyze these factors, you’ll be well on your way to choosing the health insurance plan that best fits your lifestyle and needs. Consider utilizing online comparison tools to streamline this process for easier decision-making.

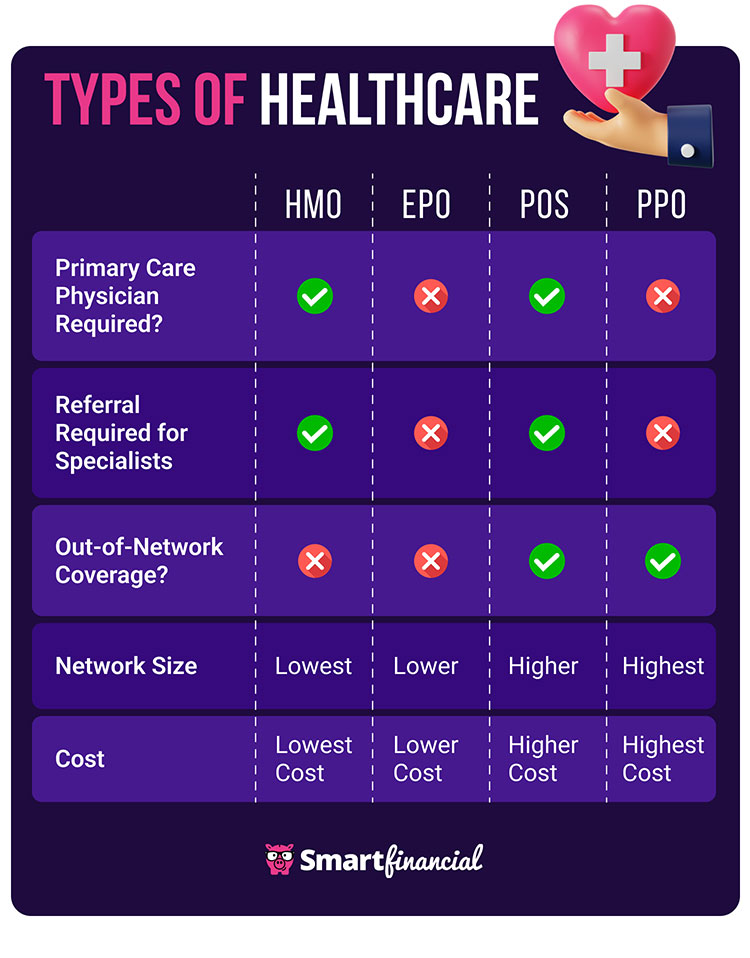

Different Types of Health Insurance Plans

Image source: SmartFinancial

Image source: SmartFinancial

Employer-Sponsored Insurance Plans

Employer-sponsored insurance plans are a common health coverage option for many young adults. Typically part of an employee benefits package, these plans are often more affordable due to employer contributions towards premiums. An employer-sponsored plan might offer various coverage levels, including health, dental, and vision insurance.

The key advantage of these plans is the lower cost, thanks to shared contributions, plus the convenience of payroll deductions for premium payments. However, the coverage specifics can vary greatly depending on the employer. It’s essential for young adults to review the plan options, including premiums, deductibles, and the available network of providers, to ensure they meet their healthcare needs. For further insights on understanding employer-sponsored insurance, visit Healthcare.gov.

Individual and Marketplace Insurance Plans

Individual and marketplace insurance plans provide an alternative for those who are self-employed, part-time workers, or simply seeking coverage outside of employer-sponsored options. The Health Insurance Marketplace, established by the Affordable Care Act, allows individuals to compare plans and choose one that fits their needs and budget.

Marketplace plans come in various categories—Bronze, Silver, Gold, and Platinum—each representing different levels of coverage and costs. It’s crucial to consider factors such as monthly premiums, out-of-pocket costs, and provider networks when selecting a marketplace plan. These plans often include financial assistance options, such as tax credits, to help lower the costs. For more details on finding individual health insurance, check out the resources on NerdWallet.

Medicaid and Low-Income Options

Medicaid and other low-income options are vital resources for eligible individuals, especially young adults who may not have sufficient income to afford private health insurance. Medicaid provides comprehensive coverage, including preventive services, hospital stays, and mental health services, with minimal to no cost to the insured.

To qualify for Medicaid, individuals must meet specific income requirements, which can vary by state. In addition to Medicaid, there are various state and community programs designed to support young adults in need of healthcare coverage. It’s important to explore these options to ensure you access necessary health services without incurring crippling debt. For information about Medicaid eligibility and benefits in your state, visit CMS.gov.

In summary, understanding the different types of health insurance plans—from employer-sponsored to individual marketplace and Medicaid options—empowers young adults to make informed decisions about their health coverage. By evaluating personal needs and available resources, they can secure health insurance that fits their lifestyle and financial situation.

Tips for Finding Affordable Health Insurance

Take Advantage of Tax Credits and Subsidies

When searching for affordable health insurance, one of the most beneficial steps is to take advantage of tax credits and subsidies offered through the Affordable Care Act (ACA). These financial aids can significantly reduce your premiums based on your income and household size. The ACA provides subsidies for individuals and families who earn between 100% and 400% of the federal poverty level, making health insurance more accessible and affordable.

To determine your eligibility for these tax credits, consider using the Health Insurance Marketplace. This platform allows you to compare different plans and see how much financial assistance you may qualify for. You can access the Marketplace and learn more here Image source: Healthcare.gov.

Key tip: When you fill out your application, be accurate with your income details, as subsidies are calculated based on the projected annual income. This strategy can help optimize your savings and ensure you get the best coverage at the lowest possible cost.

Look for Preventive Care Coverage

Another vital strategy to find affordable health insurance is to look for plans that offer comprehensive coverage for preventive care. These services — which typically include vaccinations, screenings, and annual check-ups — are often available at no additional cost to the insured. Access to preventive care not only helps you maintain your health, but it can also prevent more expensive treatments down the line.

Select plans that emphasize wellness and preventive services. Research indicates that early detection through screenings can save considerable costs in treatments over time, making it a financially sound option. According to the CDC, preventive healthcare significantly decreases the burden of chronic diseases, ultimately benefiting both individual health and overall healthcare costs.

Inquire specifically about the types of preventive services covered under a potential plan and make sure to include these aspects in your cost analysis when comparing different policies.

Stay informed about the importance of preventive care and the available benefits by visiting trusted healthcare sources like CDC.gov Image source: CDC.

By utilizing tax credits and selecting insurance plans that prioritize preventive services, you can secure affordable health insurance that not only meets your healthcare needs but also protects your financial future.

Frequently Asked Questions About Health Insurance for Young Adults

Can I Stay on My Parents’ Insurance Plan?

Yes, you can stay on your parents’ insurance plan until you turn 26 years old, according to the Affordable Care Act. This provision allows young adults to maintain coverage as they transition into adulthood, whether you’re living with your parents or away at college. It’s important to check the specifics of your parents’ plan, as some plans may have restrictions regarding out-of-state care or coverage types.

Staying on your parents’ plan can be a financially savvy choice, especially if you’re just starting your career and may not yet have access to employer-sponsored coverage. To learn more about this legislation, you can visit HealthCare.gov for comprehensive details regarding your options as a young adult.

What Happens If I Don’t Have Health Insurance?

Failing to have health insurance can have several significant consequences. First, without coverage, you not only risk high out-of-pocket costs for medical expenses but may also incur a penalty if your country or state mandates insurance coverage. The penalties vary, but the financial strain can be substantial, leading to debt if emergencies arise.

Additionally, without insurance, you may have limited access to preventative care, increasing your risk of serious health issues down the line. Regular check-ups and screenings can catch problems early, ultimately influencing your long-term health and financial stability. Not to mention, employers often offer better job prospects and salaries to candidates who can show they can take care of their health.

To better assess the implications of lacking insurance, consider exploring resources like Kaiser Family Foundation for information on health insurance coverage and statistics related to uninsured individuals.

Image source: ISU Publications

Final Thoughts on Choosing Health Insurance as a Young Adult

Choosing the right health insurance as a young adult is a crucial step towards establishing a secure financial future and ensuring access to necessary medical care. As you navigate this pivotal stage of your life, it’s essential to keep the following considerations in mind:

- Assess Your Healthcare Needs: Your current lifestyle, family history, and potential health risks should guide your choice of coverage. For instance, if you are active in sports or have pre-existing conditions, plans with comprehensive coverage may serve you better.

- Understand Key Insurance Terms: Familiarize yourself with terms like premiums, deductibles, and co-pays. This knowledge will empower you to make informed decisions, ensuring you choose a plan that offers value for your specific healthcare needs.

- Explore Different Plan Types: Whether considering employer-sponsored insurance, individual marketplace plans, or Medicaid, understanding the various options and their benefits can greatly impact your healthcare experience. More information on these can be found at HealthCare.gov.

- Utilize Available Resources: Young adults often qualify for tax credits and subsidies, making health insurance more affordable. Leverage these tools to minimize out-of-pocket expenses while gaining extensive coverage.

- Prioritize Preventive Care: Emphasize plans that cover preventive care services without additional costs. This focus can contribute significantly to your long-term health, allowing you to catch potential issues early.

In conclusion, making an informed choice about health insurance now can set the stage for a healthier future. Take the time to research, compare plans, and understand your options, ensuring you prioritize both your health and financial well-being in the process. Remember, your health is an investment in your future, and the right insurance plan is a vital component of that investment.