Future Trends in Insurance Models: Navigating the Changing Landscape

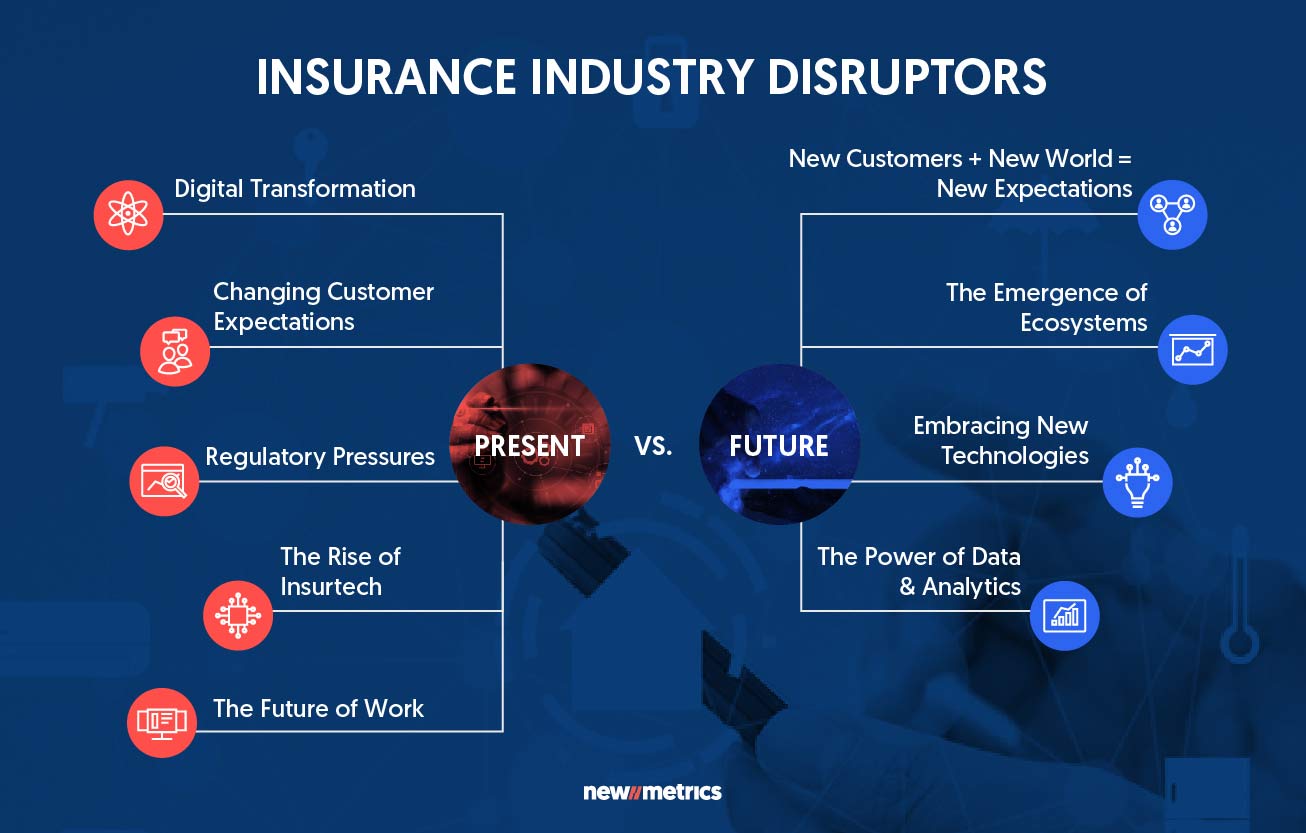

The insurance industry is undergoing a significant transformation, fueled by technological innovation, evolving customer expectations, and the broader digitalization of business practices. As new challenges emerge, insurance companies must adapt and innovate to stay competitive. The future of insurance models promises to be dynamic, with several emerging trends shaping how policies are underwritten, sold, and managed.

In this article, we explore some of the most critical future trends in insurance models, focusing on digital transformation, usage-based models, AI integration, and the evolving relationship between insurers and their customers.

The Shift Towards Digital-First Insurance Models

The insurance industry, traditionally slow to adopt new technologies, is now experiencing a rapid shift toward digital-first models. The pandemic accelerated the need for online platforms, and insurers are now embracing digital tools to enhance customer experiences, streamline operations, and expand reach. Here’s what this shift involves:

1. Cloud-Based Solutions

One of the cornerstones of digital transformation in insurance is the use of cloud computing. By leveraging cloud platforms, insurers can manage large volumes of data, reduce operational costs, and improve scalability. Cloud solutions enable real-time data processing, which is crucial for delivering instant quotes, processing claims, and assessing risks more accurately.

2. Omnichannel Engagement

In a world dominated by mobile and web applications, insurers are developing omnichannel platforms that allow customers to interact through multiple touchpoints. Whether through smartphone apps, web portals, or chatbots, insurers aim to provide a seamless experience across all digital channels. This model is essential for meeting the evolving demands of the tech-savvy consumer.

3. Self-Service Portals

Customers are increasingly expecting the ability to manage their insurance policies independently. Self-service portals that allow customers to update policies, pay premiums, file claims, and track their coverage status are becoming more prevalent. These portals not only enhance customer satisfaction but also reduce the need for human intervention, resulting in cost savings for insurers.

Usage-Based Insurance (UBI): The Rise of Pay-As-You-Go Models

Usage-based insurance (UBI) is a significant trend that is gaining momentum in the insurance space. This model ties insurance premiums to the actual usage of the insured asset, rather than traditional factors such as age or gender.

For example, in auto insurance, insurers can install telematics devices in vehicles to monitor driving behavior and adjust premiums based on factors like speed, braking patterns, and mileage. Safe drivers are rewarded with lower premiums, while high-risk drivers are charged more.

The pay-as-you-go model is also making waves in other sectors, such as health insurance and homeowners insurance, where policyholders are charged based on their actual health or property risk metrics.

1. Telematics in Auto Insurance

Telematics is at the forefront of the UBI revolution, especially in the auto insurance sector. The use of GPS and other sensors allows insurers to track driving behavior in real time, offering dynamic pricing based on how, when, and where the vehicle is driven.

2. Pay-How-You-Drive and Pay-Per-Mile Models

Two of the most popular models within UBI are Pay-How-You-Drive (PHYD) and Pay-Per-Mile (PPM). PHYD bases premiums on individual driving behaviors, while PPM charges policyholders based on how many miles they drive, providing a cost-effective solution for low-mileage drivers.

Artificial Intelligence (AI) and Machine Learning in Insurance

The integration of artificial intelligence (AI) and machine learning (ML) is reshaping the insurance landscape, allowing companies to optimize decision-making, reduce costs, and improve customer experiences. AI is being used to enhance various aspects of the insurance process, from claims processing to underwriting.

1. Automated Claims Processing

AI-powered tools are making claims processing faster and more accurate. By using natural language processing (NLP) and image recognition, AI can assess the validity of claims, identify fraudulent activity, and even estimate repair costs. This automation reduces manual intervention and speeds up the entire process, leading to quicker payouts and better customer satisfaction.

2. AI for Personalized Pricing

Insurers are leveraging AI to offer personalized pricing models. By analyzing vast amounts of data—such as driving behavior, health metrics, and purchase history—AI can help insurers assess risk more accurately and tailor premiums to individual customers. This is a shift away from the traditional broad demographic models, where all customers in a similar category (e.g., age or gender) received the same rates.

3. Chatbots and Customer Service Automation

AI-driven chatbots are transforming customer service by providing 24/7 assistance. These chatbots can answer queries, guide customers through the claims process, and even help with policy renewals. By automating routine tasks, insurers can improve operational efficiency and provide customers with instant support.

The Emergence of Blockchain in Insurance

Blockchain technology is increasingly being explored in the insurance industry to enhance transparency, security, and efficiency. Blockchain allows for the secure storage of data and facilitates faster, fraud-resistant transactions.

1. Smart Contracts

Blockchain’s smart contracts feature allows insurance companies to automate and enforce agreements without the need for intermediaries. These contracts can automatically execute when predefined conditions are met, such as triggering a payment after a claim is approved. This reduces the potential for disputes and speeds up the claims process.

2. Enhanced Fraud Prevention

Insurance fraud is a significant problem, but blockchain’s immutable ledger system makes it nearly impossible for fraudulent claims to go unnoticed. Every transaction is recorded in a secure and transparent manner, allowing insurers to verify the authenticity of claims with a high level of certainty.

Customer-Centric Insurance: The Power of Personalization

The future of insurance is not just about technology—it’s also about putting the customer at the center. Insurers are increasingly focusing on personalized services that cater to the specific needs and preferences of each policyholder.

1. Customer Data and Insights

By collecting and analyzing customer data, insurers can create more tailored insurance products that fit individual lifestyles. This could include dynamic policies that adjust based on life events, such as marriage, the birth of a child, or the purchase of a new home.

2. On-Demand Insurance

The rise of the gig economy and the increasing desire for flexibility is driving the growth of on-demand insurance. With on-demand policies, customers can activate and deactivate coverage as needed, whether it’s for a short-term trip, rental car, or temporary health coverage. This flexibility allows consumers to pay only for the insurance they need, when they need it.

The Role of Big Data and Predictive Analytics

As more data is generated by connected devices, insurers are leveraging big data and predictive analytics to gain deeper insights into risk management. By analyzing large datasets, insurance companies can predict future claims more accurately, assess risk better, and develop proactive strategies.

1. Predictive Underwriting

Insurers are using predictive models to assess risk at the underwriting stage. By analyzing historical data, such as accident records, weather patterns, and even social media behavior, insurers can predict future claims and adjust premiums accordingly.

2. Customer Retention Strategies

Big data allows insurers to develop retention strategies that are tailored to individual customers. For example, by analyzing customer behavior and engagement levels, insurers can send targeted offers, discounts, or alerts to encourage policy renewals or cross-selling.

Frequently Asked Questions (FAQs)

1. What are the main trends in the insurance industry for the future?

Key trends include digital transformation, usage-based insurance, AI-powered underwriting, personalized pricing, blockchain, and on-demand insurance.

2. How will AI impact the future of insurance?

AI will enable faster claims processing, more accurate risk assessments, and enhanced customer experiences through automated chatbots and personalized pricing models.

3. What is blockchain’s role in insurance?

Blockchain can enhance fraud prevention, streamline claims processing, and enable smart contracts, which automate and enforce agreements.

4. How does telematics affect insurance pricing?

Telematics-based insurance models use data from connected devices to adjust premiums based on driving behavior, rewarding safe drivers with lower premiums.

Conclusion

The future of insurance models is exciting, driven by technology, innovation, and a more customer-centric approach. As digital transformation continues to shape the industry, insurers must remain adaptable and embrace new technologies like AI, blockchain, and telematics. This will allow them to offer more personalized, efficient, and affordable insurance solutions for the modern consumer.

As the industry evolves, staying ahead of these trends will be key to maintaining a competitive edge and meeting the needs of today’s digital-first, value-driven customers.

By embracing these trends, insurers can unlock new opportunities and deliver exceptional value in the years to come.