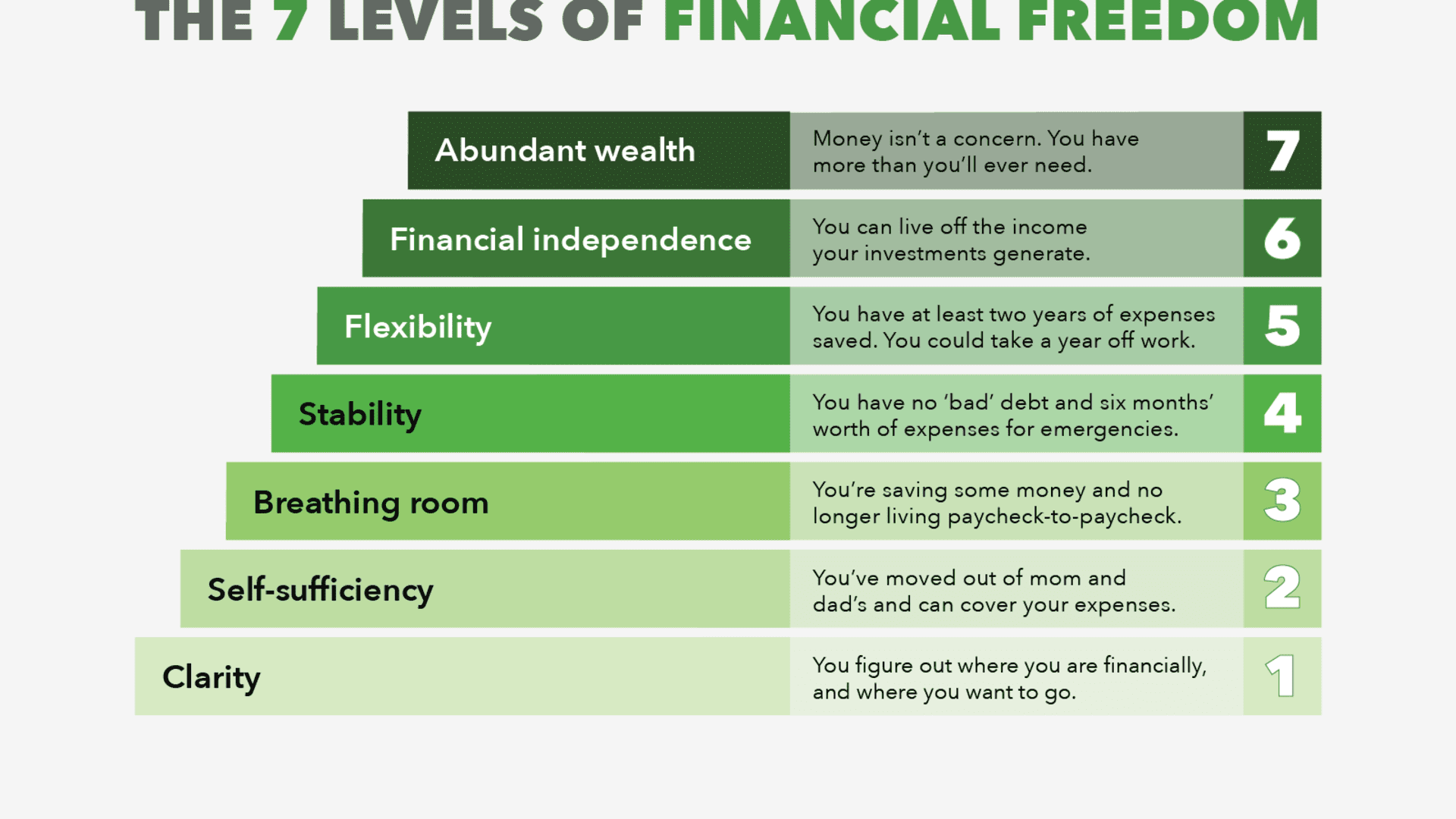

Financial Independence: A Path to Freedom

Achieving financial independence is a goal that resonates with many. It symbolizes a state of being where you have sufficient personal wealth to live without the need for earned income. This article will delve into the fundamental concepts of financial independence, outlining its benefits, strategies for achievement, and the tools and resources available to assist you on this transformative journey.

What is Financial Independence?

Definition and Importance

Financial independence refers to a state where your investments generate enough income to cover your living expenses, allowing you to live without having to rely on a job for income. This concept is crucial in today’s fast-paced world, where job security is increasingly uncertain. Achieving financial independence means taking control of your financial future and reducing your stress regarding money.

The Benefits of Being Financially Independent

- Freedom of Choice: You can choose how to spend your time without the constraints of a paycheck.

- Reduced Stress: Financial independence alleviates the anxiety related to financial insecurity, enabling you to focus on what truly matters in life.

- Improved Lifestyle: With financial security, you can pursue hobbies, travel, and spend time with loved ones without worrying about finances.

- Legacy Building: Financial independence allows you to allocate resources toward causes and charities you care about, building a legacy that reflects your values.

The Pillars of Financial Independence

Achieving financial independence isn’t just about having a lot of money. It encompasses several key components that work together to build a stable financial future.

Budgeting: Your First Step

Budgeting is the foundation of financial independence. It allows you to track your income and expenses, helping you identify areas where you can save more.

- Create a Monthly Budget: List all your sources of income and expenses. Make sure to include fixed costs (like rent and utilities) and variable costs (like groceries and entertainment).

- Identify Savings Opportunities: Look for expenses you can cut back on, such as dining out or subscription services.

Saving: Building Your Safety Net

Saving is crucial for financial security. An emergency fund serves as a financial buffer against unexpected expenses, such as medical emergencies or car repairs.

- Aim for Three to Six Months’ Worth of Expenses: This cushion will help you avoid debt when emergencies arise.

- Use High-Interest Savings Accounts: Consider opening a high-yield savings account to earn more on your savings.

Investing: Growing Your Wealth

Investing is essential for financial independence. By putting your money to work, you can increase your wealth over time.

- Start Early: The earlier you start investing, the more time your money has to grow through compound interest.

- Diversify Your Portfolio: Spread your investments across various asset classes (stocks, bonds, real estate) to mitigate risk.

Income Diversification: Beyond a 9-to-5 Job

Relying solely on a paycheck can be risky. Income diversification involves creating multiple streams of income to enhance your financial stability.

- Consider Side Hustles: Explore freelance work, consulting, or starting a small business based on your skills and interests.

- Invest in Passive Income Sources: Look into real estate or dividend-paying stocks to create ongoing revenue without active work.

Strategies for Achieving Financial Independence

Embarking on the journey toward financial independence requires strategic planning and discipline.

Create a Financial Plan

A comprehensive financial plan outlines your goals, income, expenses, savings, and investment strategies. This roadmap will help you stay focused and accountable.

Automate Your Savings

Automation simplifies the savings process. Set up automatic transfers to your savings and investment accounts each month to ensure you’re consistently saving.

Reduce Debt and Avoid Lifestyle Inflation

Managing debt effectively is crucial to achieving financial independence. Prioritize paying down high-interest debts and avoid accumulating new debt. Additionally, be mindful of lifestyle inflation, where increased income leads to higher spending. Instead, maintain your current lifestyle as your income grows.

Tools and Resources for Financial Independence

Numerous tools and resources are available to assist you in your journey toward financial independence.

Financial Independence Calculators

Online calculators can help you assess your current financial situation and project your path to financial independence. Websites like SmartAsset offer a range of calculators to get you started.

Recommended Books and Podcasts

- Books: Consider reading “The Millionaire Next Door” by Thomas J. Stanley and William D. Danko for insights on wealth-building habits.

- Podcasts: Tune into “The Financial Independence Podcast” for expert tips and success stories.

Online Courses and Workshops

Various platforms offer courses on budgeting, investing, and financial planning. Websites like Coursera and Udemy provide valuable resources to enhance your financial literacy.

In the next section, we will explore how to overcome common obstacles to financial independence and share inspiring real-life success stories. Stay tuned!

Overcoming Obstacles to Financial Independence

Achieving financial independence can be a challenging journey, often filled with obstacles and setbacks. However, with the right strategies and mindset, you can overcome these challenges and stay on track. Here are some common obstacles and how to navigate them:

1. Lack of Financial Literacy

Many people struggle with financial concepts, which can hinder their ability to make informed decisions. Increasing your financial literacy is essential.

- Educate Yourself: Take advantage of resources like books, online courses, and workshops. Websites such as Investopedia and Khan Academy offer valuable educational content.

- Join Financial Groups: Consider joining community groups or online forums to learn from others and share experiences.

2. Emotional Spending

Emotional spending can derail your financial goals. It’s important to recognize when you’re shopping out of boredom, stress, or anxiety.

- Identify Triggers: Keep a journal to track your spending habits and identify emotional triggers that lead to impulsive purchases.

- Find Alternatives: When you feel the urge to spend, engage in alternative activities such as exercising, reading, or spending time with friends.

3. Procrastination

Delaying financial decisions or actions can prevent you from reaching your goals. Combat procrastination with a structured approach.

- Set Clear Goals: Define specific, measurable, achievable, relevant, and time-bound (SMART) goals for your financial independence journey.

- Create a Timeline: Break down your goals into smaller tasks and set deadlines to keep yourself accountable.

4. Unforeseen Expenses

Unexpected expenses can jeopardize your progress. Building a robust emergency fund can help mitigate this risk.

- Budget for the Unexpected: Include a buffer in your budget for unforeseen costs, such as medical bills or car repairs.

- Review and Adjust Regularly: Revisit your budget frequently to ensure it aligns with your current financial situation and priorities.

5. Peer Pressure and Lifestyle Inflation

Keeping up with friends or social circles can lead to unnecessary spending. It’s essential to stay focused on your own goals.

- Create a Supportive Network: Surround yourself with like-minded individuals who share your financial independence aspirations.

- Practice Mindful Spending: Prioritize experiences and relationships over material possessions to minimize the desire for lifestyle inflation.

Real-Life Success Stories

Inspiration can be a powerful motivator. Here are a few examples of individuals who have achieved financial independence against the odds:

1. The Early Retirees

Sarah and Mark, a couple from Seattle, achieved financial independence by living frugally and investing wisely. They focused on maximizing their contributions to retirement accounts and minimizing unnecessary expenses.

“By living on one income and saving the other, we were able to retire early and travel the world without financial worries.” – Sarah

2. The Single Parent

Lisa, a single mother of two, faced significant financial challenges after her divorce. Through budgeting and side hustles, she managed to pay off debt and build a healthy emergency fund.

“It was tough at first, but every small step I took brought me closer to my financial goals.” – Lisa

3. The Debt-Free Journey

Tom, a former teacher, and his wife eliminated over $100,000 in student loan debt. They created a strict budget, cut unnecessary expenses, and took on additional work to accelerate their debt repayment.

“It wasn’t easy, but staying focused on our goal of financial independence made all the difference.” – Tom

Frequently Asked Questions (FAQs)

What is the first step to financial independence?

The first step is to create a budget that tracks your income and expenses. This will help you identify areas where you can save and invest.

How much money do I need to be financially independent?

The amount varies based on your lifestyle and expenses. A common rule of thumb is to aim for 25 times your annual expenses to ensure financial independence.

Can I achieve financial independence on a low income?

Yes, financial independence is achievable on any income level. It requires discipline, a solid budget, and a focus on saving and investing.

What are the best investment options for beginners?

Consider starting with index funds or ETFs, as they offer diversification and typically lower fees. Additionally, explore retirement accounts like 401(k)s and IRAs.

Conclusion: Your Journey to Financial Independence

Embarking on the journey to financial independence may seem daunting, but with determination and the right strategies, it is entirely achievable. Start by taking small steps, educating yourself, and building a supportive network. Remember that every financial decision you make today brings you one step closer to a future where you have the freedom to live life on your own terms.

Stay committed, stay informed, and embrace the path to financial independence!