Estate Planning: Securing Your Legacy

Estate planning is an essential process that involves preparing for the transfer of your assets upon your death or incapacity. It ensures that your wishes are carried out and that your loved ones are cared for according to your desires. This comprehensive guide will cover the fundamental aspects of estate planning, the importance of having a plan, and the steps to create one.

What is Estate Planning?

Definition of Estate Planning

Estate planning refers to the legal process of arranging for the disposal of your assets after you pass away. This can include your home, bank accounts, investments, personal belongings, and any business interests you may have. An effective estate plan helps minimize taxes and legal fees, ensuring that your beneficiaries receive their inheritance promptly and without unnecessary complications.

Importance of Estate Planning

The significance of estate planning cannot be overstated. Here are several key reasons why you should consider creating an estate plan:

- Control Over Your Assets: Without a plan, the state will dictate how your assets are distributed. An estate plan allows you to choose your beneficiaries.

- Minimizing Taxes: Proper estate planning can help reduce estate and inheritance taxes, allowing more of your wealth to go to your loved ones.

- Healthcare Decisions: Estate planning also includes provisions for healthcare decisions in case you become incapacitated, ensuring that your medical wishes are respected.

- Protecting Your Children: If you have minor children, an estate plan can designate guardianship and provide for their financial needs.

For more information on the importance of estate planning, visit The Importance of Estate Planning.

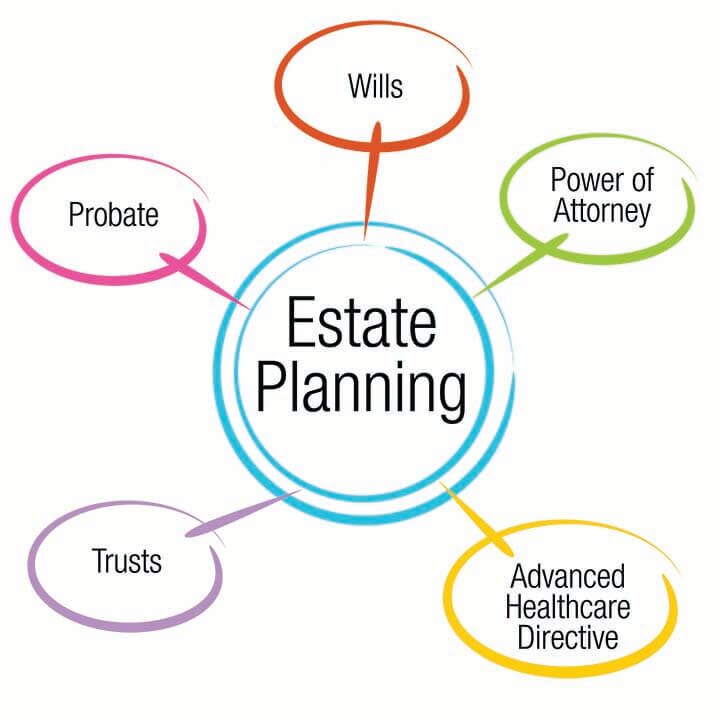

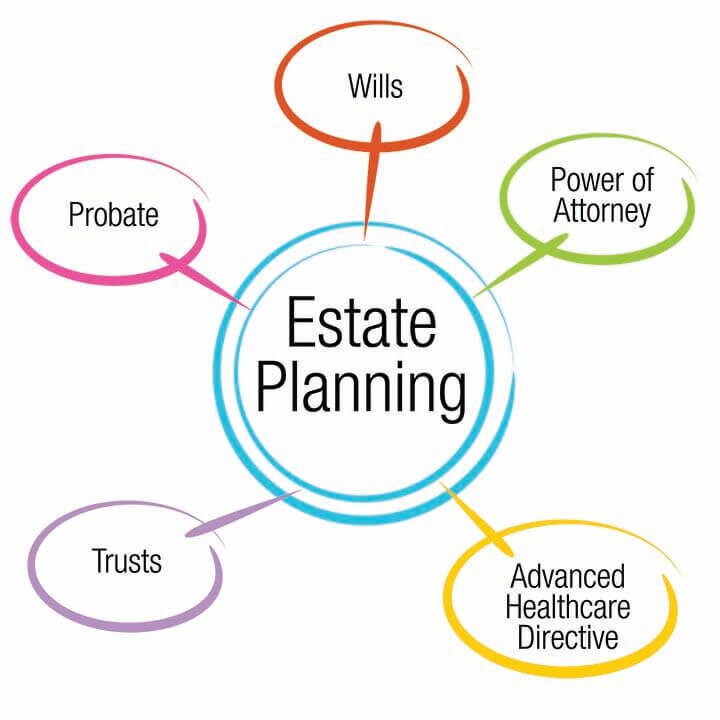

Key Components of an Estate Plan

Creating a comprehensive estate plan involves several critical components. Here’s an overview of the essential elements:

Wills and Trusts

A will is a legal document that specifies how your assets will be distributed after your death. A trust, on the other hand, is a fiduciary arrangement that allows a third party (the trustee) to hold assets on behalf of beneficiaries. Both serve unique purposes and can complement each other in an estate plan.

Difference Between a Will and a Trust

| Feature | Will | Trust |

|---|---|---|

| Effective Upon Death | Takes effect only after death | Can take effect during your lifetime |

| Probate Process | Requires probate | Avoids probate, offering privacy |

| Control | Limited control over assets after death | Ongoing control over assets |

Powers of Attorney

A power of attorney (POA) allows you to designate someone to act on your behalf in financial or legal matters. This document is crucial in the event you become incapacitated and are unable to make decisions for yourself.

Types of Powers of Attorney

- Durable Power of Attorney: Remains effective even if you become incapacitated.

- Springing Power of Attorney: Becomes effective only when a specified event occurs, such as incapacitation.

Advance Healthcare Directives

An advance healthcare directive outlines your medical treatment preferences in case you are unable to communicate them. This can include decisions about life support, surgery, and end-of-life care. This document ensures that your healthcare wishes are honored, providing peace of mind for both you and your loved ones.

Beneficiary Designations

Many financial accounts allow you to name beneficiaries, which means those assets can bypass probate and go directly to your designated individuals. It’s important to regularly review and update these designations, especially after major life events like marriage, divorce, or the birth of a child.

Steps to Create an Effective Estate Plan

Creating an estate plan can seem daunting, but breaking it down into manageable steps can simplify the process. Here are the key actions to take:

Assessing Your Assets

Start by making a comprehensive list of your assets, including:

- Real estate

- Bank accounts

- Investments

- Personal property (vehicles, jewelry, etc.)

- Business interests

Knowing what you have will help you decide how you want to distribute your assets.

Choosing Your Executor and Trustees

An executor is responsible for carrying out the terms of your will, while a trustee manages assets held in trust. Choose individuals you trust to handle these responsibilities, as they will have a significant role in executing your estate plan.

Drafting Your Will or Trust

Engage a qualified estate planning attorney to draft your will or trust. A professional can ensure that your documents meet legal requirements and reflect your wishes accurately.

Regularly Reviewing and Updating Your Plan

Life is constantly changing, and so should your estate plan. Major events like marriage, divorce, the birth of a child, or significant changes in assets may necessitate updates to your estate plan.

Common Estate Planning Mistakes to Avoid

While estate planning is crucial, many people make common mistakes that can lead to complications. Here are some pitfalls to avoid:

- Not Having an Estate Plan: Many people believe that estate planning is only for the wealthy. However, everyone can benefit from having a plan.

- Not Updating Your Estate Plan: Failing to review and update your plan can lead to outdated information and unintended distributions.

- Ignoring Tax Implications: Estate taxes can significantly reduce the amount your heirs receive. Planning for tax liabilities can help mitigate this issue.

By understanding these mistakes, you can take proactive steps to ensure your estate plan is effective and reflects your current wishes.

Frequently Asked Questions (FAQs)

What is the difference between probate and non-probate assets?

Probate assets go through a court process after death, while non-probate assets transfer directly to beneficiaries without court involvement. Examples of non-probate assets include life insurance policies and retirement accounts with designated beneficiaries.

Can I create an estate plan without an attorney?

While it’s possible to create an estate plan using online resources or DIY templates, consulting with an attorney is highly recommended. An experienced attorney can help ensure that your documents are legally sound and tailored to your specific situation.

How often should I review my estate plan?

It’s advisable to review your estate plan at least every three to five years, or sooner if significant life changes occur, such as marriage, divorce, or the birth of a child.

As we continue to explore estate planning, we’ll cover additional details in the second half of this article, including strategies for enhancing your estate plan, more FAQs, and final thoughts on taking control of your legacy. Stay tuned!

Strategies for Enhancing Your Estate Plan

To ensure that your estate plan effectively serves your needs and those of your beneficiaries, consider the following strategies:

Utilize Life Insurance

Life insurance can be a powerful tool in estate planning. It provides your beneficiaries with financial support when you pass away, helping to cover immediate expenses such as funeral costs and outstanding debts. Furthermore, the proceeds from a life insurance policy are typically tax-free, providing a significant financial benefit to your heirs.

- Term Life Insurance: This type of policy covers you for a specific term (e.g., 10, 20, or 30 years) and pays a benefit only if you pass away during that period.

- Whole Life Insurance: This policy lasts your entire life and can accumulate cash value, which you can borrow against if necessary.

Establish a Revocable Living Trust

A revocable living trust allows you to maintain control over your assets while you’re alive and ensure that they are distributed according to your wishes after your death. Unlike a will, a trust can help avoid the probate process, saving time and reducing costs for your beneficiaries.

- Benefits of a Revocable Living Trust:

- Avoids probate

- Maintains privacy regarding your assets

- Allows for the management of assets if you become incapacitated

Plan for Digital Assets

In today’s digital age, it’s crucial to include your digital assets in your estate plan. This can include online bank accounts, social media accounts, digital currencies, and more. Create a comprehensive list of your digital assets, including login credentials and instructions for your heirs on how to access and manage them.

Charitable Giving

Incorporating charitable giving into your estate plan can not only benefit the causes you care about but can also provide tax advantages. You can designate a portion of your estate to charity, which may help reduce your estate taxes.

Regular Updates and Reviews

As previously mentioned, regularly updating your estate plan is essential. Changes in your life circumstances, such as marriage, divorce, or the birth of a child, should prompt a review of your estate documents. Additionally, changes in laws regarding estate and tax may impact your plan, so staying informed is crucial.

Frequently Asked Questions (FAQs)

How do I choose an executor for my estate?

Selecting an executor requires careful consideration. Choose someone who is responsible, trustworthy, and capable of handling the financial and legal responsibilities of executing your estate plan. It’s also wise to discuss this decision with the individual beforehand to ensure they are willing to take on the role.

What if I have a blended family?

Creating an estate plan for a blended family can be more complex, as there may be multiple stakeholders involved. Open communication with all parties is essential to ensure that everyone understands your intentions. Consulting with an estate planning attorney experienced in blended families can also help navigate this process.

Can estate planning help with long-term care?

Yes, estate planning can help you prepare for long-term care. You can include provisions for long-term care insurance in your plan to cover potential future medical expenses. Additionally, incorporating medical directives can ensure that your healthcare wishes are followed.

What should I do if I don’t have a lot of assets?

Even if you feel you don’t have significant assets, an estate plan is still important. It allows you to express your wishes regarding medical decisions and guardianship of dependents. Additionally, an estate plan can help your loved ones avoid complications and uncertainties in the event of your passing.

Final Thoughts

Creating an estate plan is an important step in securing your legacy and ensuring that your wishes are respected after you’re gone. By taking the time to understand the various components of estate planning and implementing effective strategies, you can protect your loved ones and provide them with peace of mind.

If you haven’t started your estate planning journey yet, now is the time to take action. Consult with an experienced estate planning attorney to guide you through the process and tailor a plan that fits your unique needs. Remember, an estate plan is not just about distributing assets; it’s about ensuring your values and wishes are honored.

For more resources and guidance on estate planning, visit Estate Planning Resources.

Call to Action

Are you ready to secure your legacy? Start your estate planning today to protect what matters most. Consult with a professional and create a plan that meets your needs and those of your loved ones. Your future and their peace of mind are worth it.