Directors and Officers (D&O) Insurance: A Crucial Protection for Business Leaders

In the fast-paced world of business, directors and officers face many challenges, from legal risks to financial obligations. The decisions they make can shape the future of their company, but they also expose them to personal liability. This is where Directors and Officers (D&O) Insurance comes into play.

D&O insurance is essential for protecting the personal assets of executives and board members in the event of legal claims against them for actions taken within the scope of their roles. In this article, we will delve into what D&O insurance is, why it’s important, how it works, and why it should be a priority for businesses of all sizes.

:max_bytes(150000):strip_icc()/terms_d_directors-and-officers-liability-insurance.asp-FINAL-77a4fb8300e24793819279f4c8878bd4.jpg)

What is Directors and Officers (D&O) Insurance?

Directors and Officers (D&O) insurance is a liability insurance policy that protects the personal assets of individuals in managerial positions, such as directors and officers of a corporation. It provides coverage for defense costs, settlements, and judgments arising from claims made against them while performing their duties.

D&O insurance covers a wide range of scenarios, from allegations of financial mismanagement and wrongful acts to employment disputes and regulatory investigations. In essence, it helps shield business leaders from personal financial loss that could arise from actions they take in their official capacity.

Why is D&O Insurance Important?

In today’s litigious environment, the risk of facing a lawsuit is very real for directors and officers. Whether the company is publicly traded or privately held, business leaders are exposed to potential claims from shareholders, employees, customers, competitors, and government agencies.

Here are several reasons why D&O insurance is critical for businesses:

1. Protection from Legal Risks

Directors and officers can be sued for a wide variety of reasons, including alleged breaches of fiduciary duty, misrepresentation of financial information, or failure to comply with regulatory requirements. D&O insurance helps cover the costs of defending against such claims and any financial settlements or judgments that may arise.

2. Attract and Retain Top Talent

Highly skilled executives and board members may hesitate to join a company if they believe their personal assets could be at risk due to potential legal claims. By offering D&O insurance, companies can ensure that top talent feels secure in their roles, knowing they are protected from personal liability.

3. Business Continuity

A legal dispute can drain a company’s resources and distract its leadership from focusing on growth and profitability. With D&O insurance, businesses can handle legal issues efficiently, ensuring that leadership can continue running the company without excessive disruption.

4. Safeguarding Corporate Reputation

Legal disputes, especially those involving high-ranking executives, can harm a company’s reputation. D&O insurance helps minimize reputational damage by addressing claims quickly and helping to resolve disputes before they escalate into major public controversies.

How Does D&O Insurance Work?

D&O insurance is designed to cover legal fees, settlements, and damages that arise from lawsuits against the directors and officers of a company. However, it doesn’t cover all types of claims. Typically, D&O insurance will cover:

- Defense costs: Expenses related to defending the director or officer in court, including lawyer fees, expert witness costs, and court costs.

- Settlements and judgments: If the case is settled or a judgment is made against the individual, D&O insurance will cover the payment, up to the policy limit.

- Allegations of wrongful acts: This includes accusations of breaches of fiduciary duty, errors in judgment, failure to act in good faith, and failure to comply with laws and regulations.

Types of D&O Insurance Policies

There are several types of D&O insurance policies, each with different coverage options:

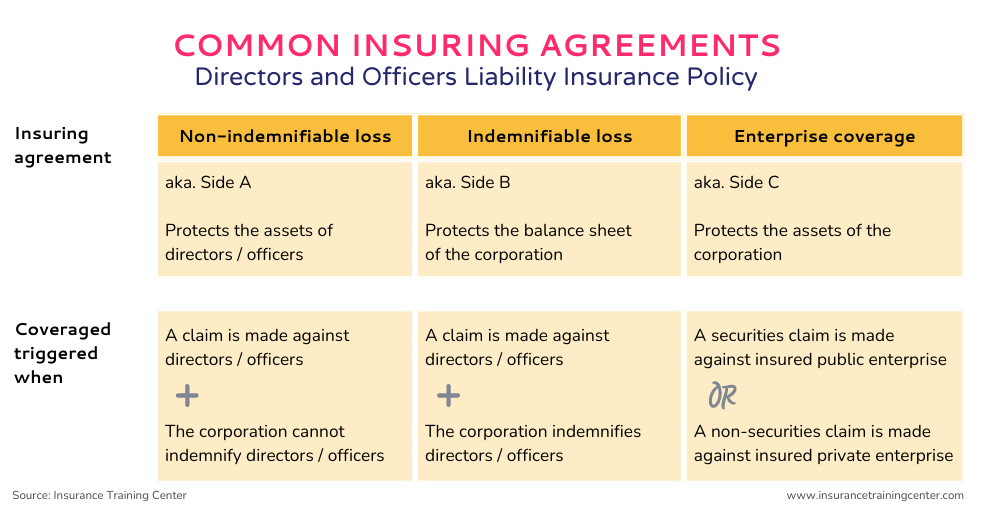

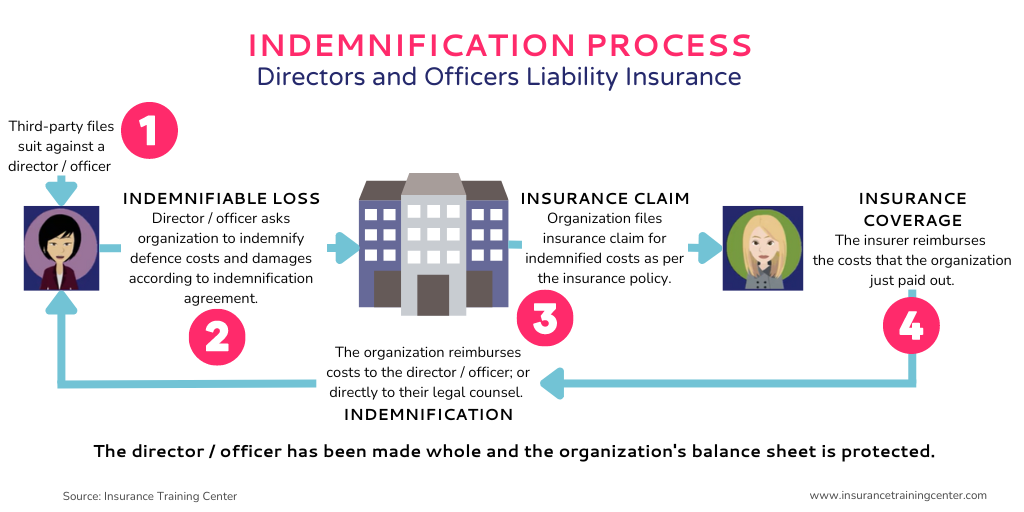

- Side A Coverage: This covers directors and officers personally when the company is unable or unwilling to indemnify them.

- Side B Coverage: This reimburses the company for costs incurred in covering the legal fees and judgments for its directors and officers.

- Side C Coverage: Also known as “entity coverage,” this protects the company itself in the event that it is named in a lawsuit involving its directors and officers.

What D&O Insurance Does Not Cover

While D&O insurance provides robust protection, it does not cover everything. Some exclusions include:

- Fraud and criminal acts: If a director or officer is accused of fraud or intentional misconduct, they are not covered by D&O insurance.

- Personal lawsuits: Claims that arise from personal matters unrelated to the individual’s role in the company are not covered.

- Fines and penalties: Government-imposed fines and penalties are generally excluded from D&O coverage, though some policies may cover regulatory investigations.

Key Benefits of D&O Insurance

Here are the key benefits of purchasing D&O insurance for your business:

- Protection for business leaders: D&O insurance shields executives from personal financial risk, providing peace of mind that their personal assets are protected in case of legal action.

- Legal defense funding: Even if the claims against directors and officers are groundless, legal defense costs can be substantial. D&O insurance ensures that the company or individual is covered.

- Corporate stability: By offering D&O insurance, companies can maintain stability, even in the face of complex legal disputes. This ensures continuity in leadership and avoids unnecessary distractions.

Factors That Affect the Cost of D&O Insurance

The cost of D&O insurance varies significantly based on several factors. Some of the primary considerations include:

- Size of the company: Larger companies tend to face higher premiums due to the greater exposure to potential claims.

- Industry: Companies in industries with higher regulatory scrutiny (such as finance or healthcare) may pay more for coverage.

- Claims history: A company with a history of legal claims may face higher premiums due to the increased risk.

- Coverage limits: The higher the coverage limit, the more expensive the policy.

- Risk profile: Companies that engage in high-risk activities, such as mergers and acquisitions, may face higher premiums.

Key Considerations When Choosing D&O Insurance

Choosing the right D&O insurance policy requires careful consideration. Here are a few important factors to keep in mind:

1. Coverage Limits

Determine the amount of coverage your company needs based on the size of the company, the risk exposure, and the financial assets of its directors and officers.

2. Claims Process

Understand how the insurance company handles claims. Do they have a fast, efficient claims process? Are they known for supporting their policyholders in times of crisis?

3. Exclusions and Limitations

Carefully review the policy to understand what is and isn’t covered. This will help you avoid surprises down the line.

4. Reputation of the Insurer

Work with a reputable insurance provider that specializes in D&O insurance. Check reviews, industry ratings, and customer feedback to ensure you’re getting reliable coverage.

5. Industry-Specific Coverage

Some insurers offer specialized D&O insurance for specific industries, such as healthcare, tech, or financial services. If your business operates in a high-risk sector, look for an insurer that understands your unique needs.

Frequently Asked Questions (FAQs)

1. What is the difference between D&O insurance and general liability insurance?

D&O insurance specifically covers the personal liability of directors and officers, while general liability insurance covers bodily injury, property damage, and other risks unrelated to executive decisions.

2. Who should purchase D&O insurance?

Any company with directors and officers, particularly those in leadership positions, should consider purchasing D&O insurance. This includes private, public, and nonprofit organizations.

3. Is D&O insurance mandatory?

While D&O insurance is not legally required, it is highly recommended for companies to protect their leadership from potential financial risks.

4. How much D&O insurance do I need?

The amount of coverage depends on the size and nature of your business, the leadership structure, and the potential risks your company faces. A qualified insurance broker can help assess your needs.

5. Does D&O insurance cover employment-related lawsuits?

Yes, D&O insurance can cover employment-related claims, such as wrongful termination, harassment, and discrimination, as long as they are within the scope of the officer’s or director’s duties.

Conclusion

Directors and Officers (D&O) Insurance is a critical component of risk management for businesses, particularly in today’s complex and litigious environment. By offering protection against legal claims, ensuring business continuity, and attracting top talent, D&O insurance helps safeguard your company’s leadership and financial health.

If you are a business owner or executive, ensure that your D&O insurance policy covers all necessary risks. Consulting with an insurance broker who specializes in this area can help you find the right coverage to protect your leadership team and your business’s future.