Understanding the Basics: Buying vs. Leasing a Car

Image source: Oregonians Credit Union

Image source: Oregonians Credit Union

What Does It Mean to Buy a Car?

Buying a car means you purchase the vehicle outright, either in a single payment or through financing options like a vehicle loan. Once you buy the car, you own it completely, which means you can modify or sell it whenever you choose. Here are some important points to consider:

- Ownership: As the owner, you bear all responsibilities, including maintenance costs and depreciation.

- Equity: Over time, your vehicle somewhat retains its value, allowing you to have trade-in or resale options.

- Customization: You can personalize the car as per your preferences, without restrictions.

- No Mileage Limits: You can drive as much as you like without worrying about penalties that leasing agreements often impose.

Most buyers finance their vehicles through loans, indicating they pay an initial down payment followed by monthly payments, which can vary based on loan terms and interest rates. According to a report from the Consumer Financial Protection Bureau, understanding loans can significantly impact your overall financial experience when buying a car.

What Does It Mean to Lease a Car?

Leasing a car involves entering a contract to use a vehicle for a specified term—usually between two to four years—without taking ownership. While leasing can be appealing for those who want lower payments and a new car every few years, it’s essential to understand its intricacies:

- Monthly Payments: Lease payments are generally lower than financing payments because you’re essentially paying for the vehicle’s depreciation during the lease period rather than the total value.

- Mileage Restrictions: Most leases have mileage limitations, usually between 10,000 to 15,000 miles per year. Exceeding these limits can result in hefty fees.

- Maintenance and Repairs: Leased vehicles often come with warranties that cover maintenance for the duration of the lease, making it less expensive for the lessee.

- End-of-Lease Options: At the end of your lease, you can either return the vehicle or buy it for a predetermined price.

While leasing can feel appealing with lower upfront costs and regular upgrades, it’s crucial to assess your personal driving habits and financial situation to determine if it is right for you. For detailed financial literacy on leasing versus buying, check resources available on the U.S. Department of Energy’s website.

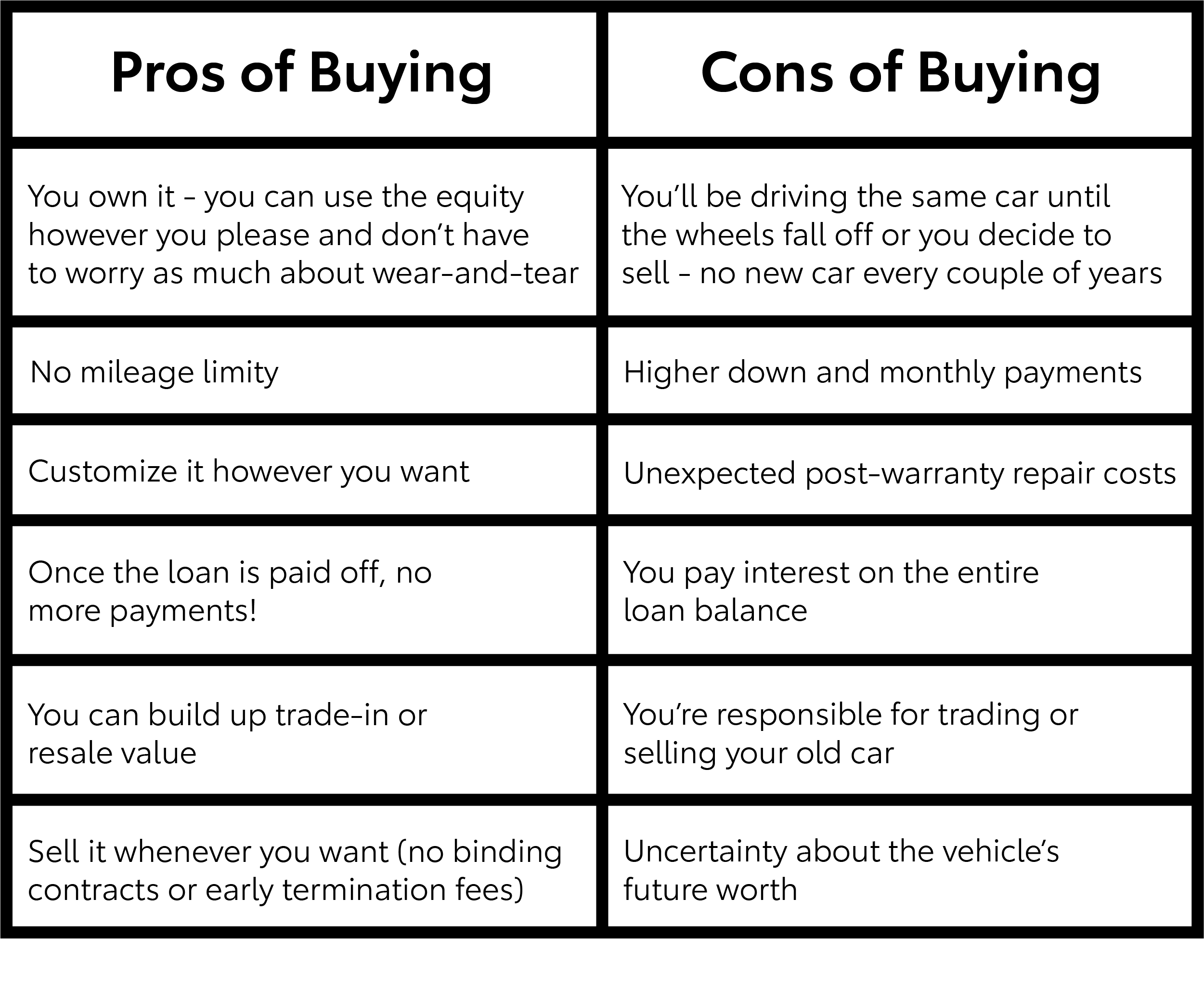

Pros and Cons of Buying a Car

Benefits of Buying a Car

Buying a car offers numerous benefits that make it an attractive option for many individuals and families. Here are some of the key advantages:

- Ownership: When you buy a car, you own it outright. This means you have the freedom to drive it as much as you want, customize it to your liking, and sell it whenever you choose. Ownership translates to no mileage limits or restrictions (learn more about this from Consumer Reports).

- Long-term Cost Savings: While the upfront cost of purchasing a vehicle can be significant, it often leads to greater savings over time. After your loan is paid off, all subsequent expenses are generally much lower, leading to substantial savings compared to leasing where monthly payments continue with no equity build-up.

- No Hidden Fees: Buying typically eliminates fees associated with leasing, such as disposition fees and excess mileage charges. With ownership, you only need to cover maintenance, insurance, and taxes.

- Potential Resale Value: If you maintain your vehicle well, you have the option to sell it later. A well-maintained car can retain a good portion of its value, providing you with a financial return when you decide to sell.

-

Emotional Satisfaction: Many drivers find a sense of pride and satisfaction in owning their vehicle. This emotional connection can enhance your overall driving experience.

Image source: Dealer

Image source: Dealer

Drawbacks of Buying a Car

While buying a car presents various advantages, it also has several drawbacks that should be carefully considered:

- High Upfront Costs: Purchasing a vehicle typically requires a substantial down payment, which can strain your finances. Also, auto loans may have higher interest rates, leading to increased monthly payments.

-

Depreciation: New cars depreciate quickly after purchase, with some estimates suggesting a reduction in value by as much as 20% to 30% within the first year alone. This can negatively impact your investment when you seek resale.

-

Maintenance Responsibility: As the owner, you bear the entire burden of maintenance and repairs once the warranty period ends. Cars can require significant investments for upkeep over time, impacting your budget.

-

Longer Commitment: Buying a car often entails a longer commitment than leasing, meaning you are liable for the vehicle until it is paid off or sold. This may limit your flexibility if your circumstances change.

-

Financing Risks: If financing the purchase, there’s a risk of going upside down on your loan (owing more than the car is worth), especially if you need to sell the car early. This can create financial strain if not managed properly.

In conclusion, while buying a car can provide benefits such as ownership and potential long-term savings, it’s crucial to be aware of the drawbacks, including high initial costs and ongoing maintenance responsibilities. Weighing these pros and cons will aid in making a well-informed decision aligned with your financial and personal goals.

Pros and Cons of Leasing a Car

Advantages of Leasing a Car

Leasing a car offers several advantages that can be particularly attractive for certain drivers. Here are some key benefits:

- Lower Monthly Payments: One of the most significant advantages of leasing is the lower monthly payments compared to purchasing a car. Since you are essentially renting the vehicle for a specific term (usually 2-3 years), you pay for the car’s depreciation instead of its total value. This makes leasing a more budget-friendly option for many.

-

Newer Vehicles More Often: Leasing allows you to drive a new car every few years. Many leases last around 2-3 years, giving you the chance to experience the latest models with the most recent technology, features, and safety updates without the long-term commitment of ownership.

-

Lower Repair Costs: Most lease agreements cover the vehicle’s warranty period, meaning that you are often protected against costly repairs. You may only need to cover routine maintenance, which further reduces the overall financial burden.

-

Flexibility: Leasing can offer more flexibility than buying. If your needs change, you can typically return the car at the end of the lease term without the hassle of selling it. This can be advantageous for people who prefer to change cars frequently or have varying mileage needs.

For more insights on leasing versus buying, check out this detailed guide from Edmunds: Leasing vs. Buying a Car.

Disadvantages of Leasing a Car

While leasing has numerous benefits, it also presents some disadvantages that potential lessees should consider:

- Mileage Limits: Lease agreements often come with mileage restrictions, typically between 10,000 to 15,000 miles per year. Exceeding these limits can result in costly fees at the end of the lease, which can significantly increase your overall expenses if you drive frequently.

-

No Ownership: At the end of a lease, you must return the car, and you do not own any equity in it. This means you won’t have an asset to sell or trade-in, which can be a downside for those looking to invest money into their vehicle.

-

Customization Limitations: Lease contracts usually restrict any personal modifications to the vehicle. If you’re someone who enjoys customizing your ride, leasing may not be the best choice.

-

Long-term Cost: Although monthly payments are lower, leasing can end up costing you more in the long run if you continuously lease cars. Over time, a buyer may benefit from ownership and reduced payments after the loan is paid off.

In conclusion, when weighing the pros and cons of leasing a car, it’s essential to evaluate your personal situation and preferences to determine if leasing aligns with your lifestyle and financial goals.

Key Factors to Consider Before Deciding

Your Driving Habits and Lifestyle

When it comes to buying vs. leasing a car, your driving habits and lifestyle play a pivotal role in guiding your decision. If you frequently embark on long road trips or have a daily commute exceeding 15,000 miles, purchasing a vehicle may be the more practical choice. Ownership allows for unrestricted mileage, providing peace of mind without the worry of exceeding lease limits.

Conversely, if your driving is mainly around town and you value the latest models, leasing can be beneficial. It allows you to drive a new car every few years with minimal maintenance costs, as the vehicle is typically under warranty throughout the lease period. Assessing your personal driving habits will help you identify which option aligns with your lifestyle.

Financial Implications: Upfront Costs vs. Long-term Expenses

Understanding the financial implications is crucial when deciding whether to buy or lease a car. Upfront costs are typically lower when leasing; you may only need to cover the first month’s payment, a security deposit, and some taxes and fees. In contrast, buying a car usually requires a larger down payment, which can range from 10% to 20% of the vehicle’s price.

Nonetheless, it’s important to evaluate long-term expenses. Owning a car means you’ll eventually pay off the vehicle, potentially leading to years of no payments, which could be financially liberating. According to Investopedia, owning a car often incurs ongoing costs like insurance and maintenance, but over time, this can often be less than leasing, especially if you keep the vehicle for many years.

Mileage Limits and Restrictions

A crucial factor to consider is the mileage limits and restrictions associated with leasing. Most leases come with annual mileage limits—typically between 10,000 and 15,000 miles—and exceeding these limits can lead to hefty fees at the end of your lease term. If you find yourself needing to drive more than these limits frequently, leasing may not be the ideal option for you.

In contrast, when you buy a car, you’re free to drive as much as you like without worrying about penalties. Be honest about your typical driving patterns to ensure you choose a solution that won’t lead to surprise costs later.

Resale Value vs. Ownership Flexibility

Lastly, consider the balance between resale value and ownership flexibility. Cars typically depreciate rapidly, and when you buy, you’re often left navigating the resale market when it’s time to sell. This aspect can yield significant financial gain or loss depending on the condition and demand for your vehicle at time of sale.

Leasing, on the other hand, simplifies this equation by allowing you to return the vehicle at the end of the lease term without worrying about depreciation or selling the car. This is particularly appealing for those who don’t want the hassle of determining a vehicle’s worth in the future. However, the trade-off is that you won’t build any equity in a leased vehicle. Weigh these factors carefully to determine what aligns best with your financial goals.

In each of these areas—driving habits, financial obligations, mileage restrictions, and resale considerations—take time to reflect and assess your unique situation. Making an informed decision can lead to years of satisfaction with your car choice.

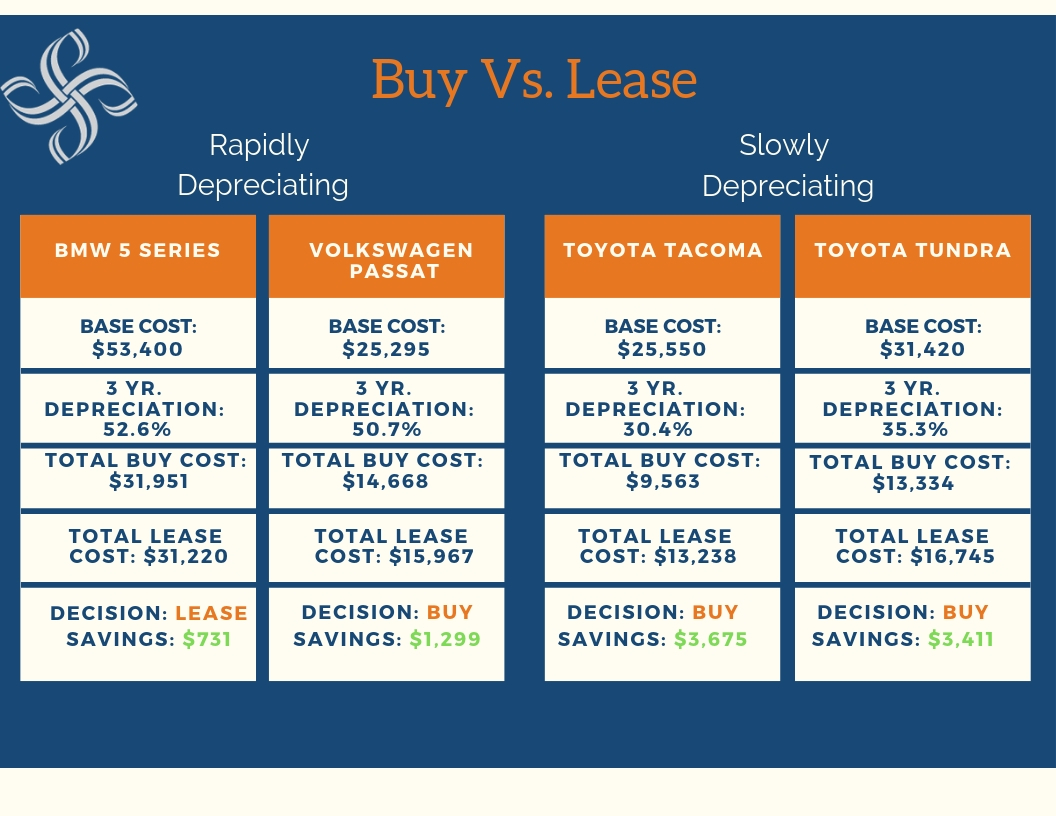

Comparing Costs: Leasing vs. Buying a Car

Monthly Payments: How They Differ

When it comes to managing your budget for a vehicle, monthly payments are a critical factor to consider. Generally, leasing a car results in lower monthly payments compared to buying. This is primarily because, in a leasing agreement, you’re essentially paying for the vehicle’s depreciation during the lease term, plus interest and fees, rather than the full purchase price. For instance, while the typical lease might ask for payments that range between $200 to $400 a month, monthly financing payments for purchasing a car can often be notably higher, usually falling between $300 to $600 depending on the vehicle price and loan terms.

Leasing agreements may also have lower requirements for down payments, often ranging between $0 and $2,000, compared to purchasing a vehicle where down payments can typically be 20% of the car’s price. The lower upfront costs and payments associated with leasing make it a more attractive option for many budget-conscious consumers.

Image source: Smith Partners Wealth

Image source: Smith Partners Wealth

However, it’s essential to keep in mind that, at the end of a leasing term, you do not own the vehicle, and thus, you have no equity to show for your payments. On the contrary, when buying a car, every monthly payment contributes towards the overall ownership of the vehicle, which can be advantageous if you plan on keeping the car long term.

Long-term Financial Impact of Each Option

The long-term financial impacts of leasing versus buying a car can reveal significant differences over time. When you lease, you cover the vehicle’s depreciation, leaving you without a tangible asset at the end of the lease term—typically three years. Each leasing cycle might tempt you into a new vehicle with the latest technology but will keep you in a cycle of payments. Essentially, you are continuously paying to access a car without accruing any equity.

In contrast, purchasing a car allows you to build equity over time. Once the car loan is paid off, you own the vehicle outright, which can lead to significant savings in the long run. For instance, if you choose to keep the car for several years post-loan payment, your ongoing costs may only include maintenance, insurance, and fuel, compared to a leasing scenario where you pay perpetually for the use of a vehicle.

Furthermore, the decision to buy or lease can also influence your long-term financial health based on factors such as interest rates, maintenance costs, and depreciation. Generally, leased vehicles fall under warranty, minimizing repair costs, while new car owners will face depreciation. According to a study by Edmunds, new cars lose roughly 20% of their value in the first year alone.

Choosing between leasing and buying ultimately boils down to individual financial situations and goals. If you seek long-term savings and are willing to commit to a vehicle, buying may be your well-trodden path. However, if you prefer lower payments and flexibility, leasing could cater to your lifestyle. To dive deeper into leasing and buying costs, check out Car and Driver.

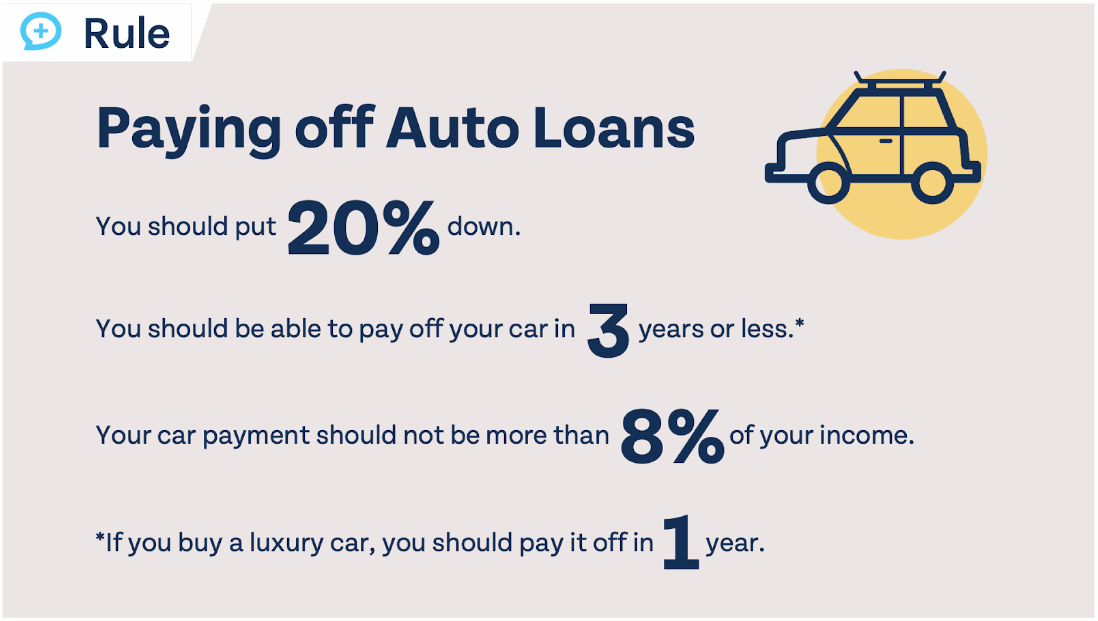

Who Should Buy a Car?

Deciding whether to buy a car is a significant financial decision that requires careful consideration. Understanding the factors that contribute to making such a choice is essential for various types of car buyers. Below are the key demographics and situations for which purchasing a vehicle may be the most beneficial option.

1. Frequent Drivers

Individuals or families who drive frequently for work or personal activities typically benefit from owning a car. Buying is ideal for those who put high mileage on their vehicle, as ownership eliminates restrictions imposed by leasing agreements, such as mileage limits. Additionally, owning a car allows you to customize it according to your preferences and needs without worrying about penalties.

2. Long-Term Commitment

If you envision keeping your vehicle for several years, purchasing may be the right choice. Buying a car results in eventual ownership, leading to financial benefits as the vehicle ages. Once the loan is paid off, you can enjoy years of use without monthly payments. This scenario is often more financially viable in the long run, especially if you intend to drive the car until it has significant mileage.

3. Budget-Conscious Buyers

Individuals who prefer not to deal with ongoing monthly payments may find buying more attractive. Buying a car means the ability to save for a future purchase without the pressure of regular leasing costs. According to the Consumer Financial Protection Bureau, buyers can negotiate the total price rather than worrying about lower initial monthly payments typically associated with leasing.

4. People Who Value Flexibility

When you buy a car, you gain freedom regarding ownership. This flexibility may appeal to buyers who dislike the limitations imposed by leasing agreements, such as mileage caps and required insurance coverage. Owning a vehicle allows for adjustments – whether it’s altering the vehicle, repairs, or even selling the car at your discretion.

5. Families or Those Needing Larger Vehicles

For those who require larger vehicles, such as SUVs or vans typically used for family purposes or active lifestyles, buying can be advantageous. The extra room and durability of larger vehicles are usually essential for family road trips, outings, or transporting goods.

6. Those Looking for Resale Value

Buying a car may be an ideal option for individuals who understand how to maximize a vehicle’s resale value. When you buy, you can retain the value of the vehicle, sell it, and potentially purchase another vehicle without dealing with leasing penalties or restrictions.

In summary, buying a car is an excellent option for frequent drivers, those looking for a long-term commitment, budget-conscious buyers, individuals valuing flexibility, larger families needing specific vehicles, and those interested in leveraging resale value.

Image source: Money Guy

Image source: Money Guy

If you fit one or more of these profiles, it might be worth considering purchasing a car as your primary mode of transportation. Always assess your individual circumstances and consult with financial advisors if unsure about the best options for your situation.

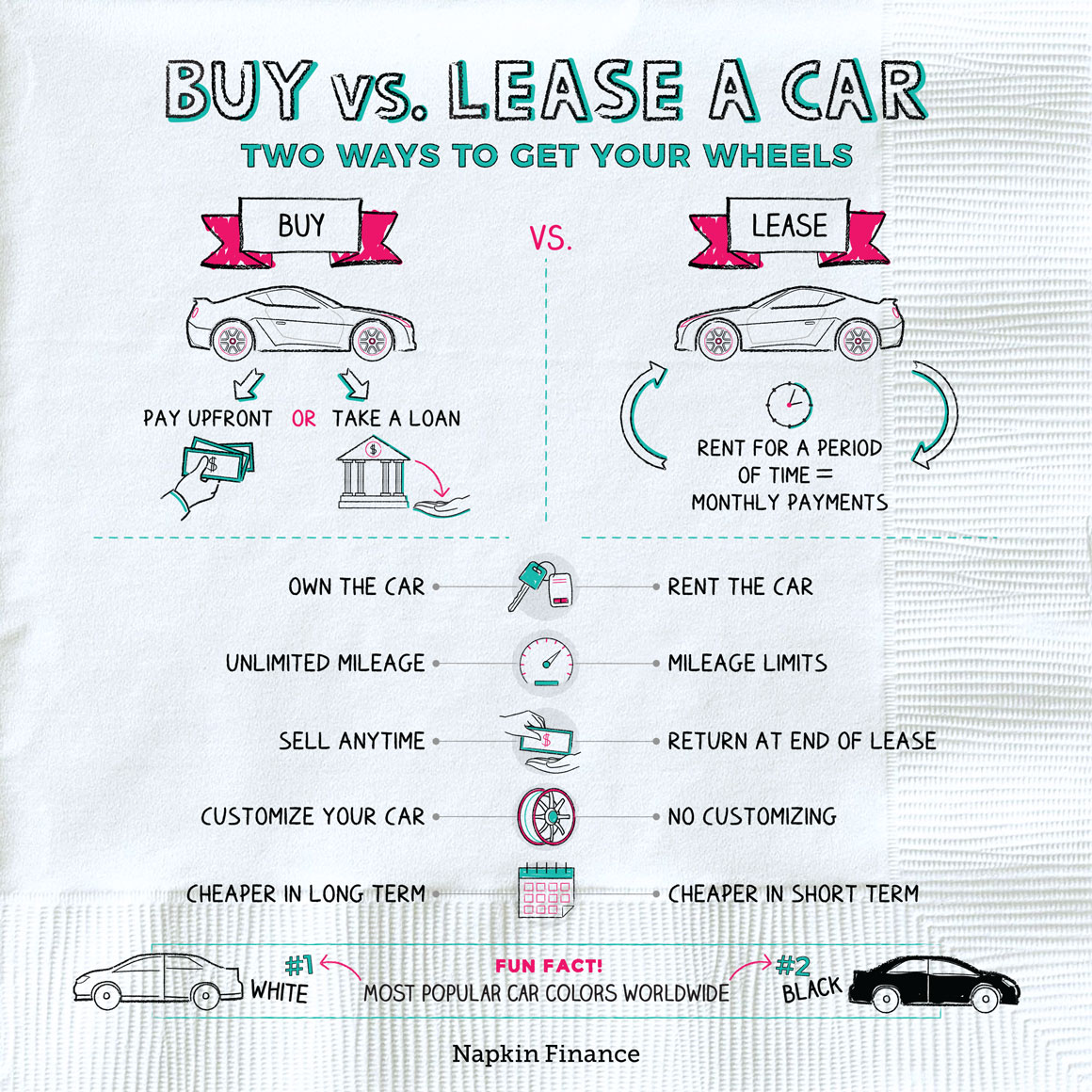

Who Should Lease a Car?

Leasing a car can be an attractive option for many individuals, but it isn’t for everyone. Understanding who should lease a car involves evaluating your lifestyle, financial situation, and preferences. Here are several key factors to consider:

1. Frequent Vehicle Updates

Leasing is ideal for individuals who enjoy driving new cars every few years. With typical lease terms ranging from two to four years, lessees can easily switch to the latest models equipped with the latest technology, safety features, and fuel efficiency. If you appreciate having access to cutting-edge vehicles without the long-term commitment, leasing may be the right choice for you.

2. Lower Monthly Payments

Most leases come with lower monthly payments compared to buying a car outright. If you have a constrained budget but still want to drive a desirable and reliable vehicle, leasing can help you get a vehicle that might be out of your price range if you were to purchase it. This can be especially beneficial for young professionals or college graduates who are just starting their careers.

3. Limited Annual Mileage

If you have predictable driving habits and do not exceed the average annual mileage, leasing can be a good fit. Most leases come with mileage limits (typically between 10,000 to 15,000 miles per year). If your daily commute and driving pattern fit within these limits, leasing might be a practical choice. However, if you frequently take long trips or have a job that requires extensive travel, owning a vehicle could be more suitable.

4. Business Use

Leasing can offer significant tax advantages for business owners. If you use your vehicle primarily for business purposes, leasing can provide tax deductions and help manage cash flow while avoiding depreciation issues. Consult with a tax professional to understand the benefits that may be available to you.

5. Maintenance and Repair Costs

Another factor to consider is maintenance. Leased vehicles often remain under the manufacturer’s warranty for the duration of the lease, meaning that major repairs are typically covered. If you prefer hassle-free vehicle maintenance without unexpected repair costs, leasing ensures you drive a vehicle that’s usually still under warranty.

Conclusion

In summary, leasing a car may be ideal for someone who values flexibility, lower monthly payments, and keeping up-to-date with the latest automotive technologies. It can also be beneficial for those who drive moderate miles each year and want to minimize maintenance costs. By thoroughly considering these factors, you can better determine if leasing aligns with your lifestyle and financial goals.

For further details on the implications of leasing, you can visit Edmunds’ Guide to Leasing a Car.

Image source: Napkin Finance

Image source: Napkin Finance

Final Thoughts: Choosing the Option Right for You

Deciding whether to buy or lease a car is a monumental choice that can influence your finances, driving experience, and lifestyle for years to come. Each option presents unique advantages and disadvantages that align differently depending on individual circumstances and preferences.

- Evaluate Your Financial Situation: Take a close look at your budget and financial goals. Buying a car often involves higher upfront costs, such as a down payment, taxes, and registration fees, while leasing typically requires less initial expenditure. However, consider the long-term impact—owning a car can lead to financial savings over time, especially if you drive a lot and keep the vehicle for several years.

-

Assess Your Driving Habits: Reflect on your typical driving patterns. If you frequently take long trips or have a commuting routine that exceeds standard mileage limits (usually around 12,000-15,000 miles per year), purchasing may be more beneficial. Leasing usually comes with mileage restrictions, which can incur additional charges if exceeded.

-

Consider Your Preference for New Technology: If you enjoy driving the latest models and technology, leasing can be appealing. This option allows you to drive a new car every few years without the hassle of selling or trading in a vehicle. However, if you prefer stability and a long-term investment, buying may suit you better.

-

Ownership Flexibility: With a leased vehicle, you’ll never own the car, and this can be a deterrent for some. If you’re looking for long-term ownership, where you have the freedom to modify, customize, or simply enjoy a car without ongoing payments, buying is the way to go.

-

Evaluate Depreciation Rates: When buying, remember that the vehicle will depreciate over time. Understanding the resale value of the vehicle you are considering is crucial. While leasing doesn’t expose you to depreciation risks, owning a car means you can leverage any remaining value down the line when you’re ready to sell.

In conclusion, the choice between buying and leasing hinges on your individual financial circumstances, driving habits, and personal priorities. Carefully assess your situation against the factors discussed to make an informed decision that aligns best with your current and future needs. For more detailed insights on car buying and leasing, consider visiting Edmunds, a well-respected resource in the automotive space.