Business Owners Policy (BOP): The Ultimate Insurance Coverage for Your Business

In today’s competitive business landscape, protecting your company from unforeseen risks is more crucial than ever. Whether you’re running a small startup or managing a growing enterprise, a Business Owners Policy (BOP) can provide comprehensive coverage to safeguard your assets, employees, and overall business operations.

In this article, we’ll dive deep into what a Business Owners Policy is, the types of coverage it includes, and why it is essential for businesses of all sizes. By the end, you’ll understand the benefits of having a BOP and how it can offer peace of mind in an unpredictable world.

:max_bytes(150000):strip_icc()/Business-owners-policy-4200047-recirc-FINAL-c3a378349eb64c66931b367a06aef1e7.png)

What is a Business Owners Policy (BOP)?

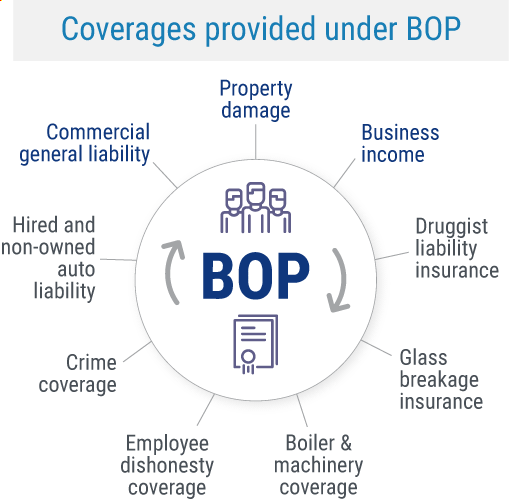

A Business Owners Policy (BOP) is a comprehensive insurance package that combines several essential coverages into one policy. It is specifically designed for small to medium-sized businesses, providing affordable protection against common business risks. A BOP typically combines three major types of insurance:

- Property Insurance: Covers damage to your business property, including buildings, inventory, and equipment.

- Liability Insurance: Protects your business against claims of bodily injury, property damage, or personal injury caused by your products, services, or operations.

- Business Interruption Insurance: Covers lost income and operating expenses if your business is temporarily shut down due to a covered event.

By bundling these coverages into a single policy, a BOP makes it easier and more cost-effective for business owners to manage their insurance needs.

Why Do You Need a Business Owners Policy?

A Business Owners Policy offers numerous advantages for entrepreneurs, including:

- Affordable and Comprehensive Protection

A BOP bundles essential insurance coverages at a discounted rate, which is typically cheaper than purchasing each coverage separately. -

Convenience and Simplicity

With a BOP, you only need to manage one policy, rather than multiple separate ones, streamlining your insurance process. -

Customizable Options

While BOPs come with essential coverages, they can also be tailored to meet the specific needs of your business. You can add additional coverages, such as cyber liability, to fit your unique requirements. -

Protection Against Common Risks

Business owners face various risks daily—whether from accidents, property damage, or legal claims. A BOP ensures that you have a safety net to protect your business in case of unexpected events.

What Does a Business Owners Policy Cover?

The key benefit of a Business Owners Policy is that it combines several important insurance coverages into one package. Here’s a detailed breakdown of the coverages typically included in a BOP:

1. Property Insurance

This coverage protects your business property, such as your office building, equipment, inventory, and furniture, in case of damage or loss. Common causes of damage covered by property insurance include:

- Fire

- Theft

- Vandalism

- Natural disasters (depending on the policy)

In addition, property insurance may cover business-owned personal property and equipment that are essential for daily operations. For example, if your business relies on expensive machinery or technology, this coverage can help pay for repairs or replacement if something goes wrong.

2. Liability Insurance

Liability insurance is one of the most critical components of a Business Owners Policy. It covers your business against claims of bodily injury or property damage caused by your products, services, or business operations. There are two main types of liability coverage:

- General Liability Insurance: Protects against claims made by third parties (such as customers, vendors, or contractors) for bodily injury or property damage.

- Product Liability Insurance: Specifically protects against claims related to defects or hazards in the products your business manufactures, distributes, or sells.

For example, if a customer gets injured using a product you sell, or if a visitor slips and falls in your store, general liability insurance will cover medical costs, legal fees, and damages.

3. Business Interruption Insurance

If a disaster, such as a fire or flood, forces your business to close temporarily, business interruption insurance helps cover lost income during the shutdown period. This coverage can help pay for ongoing expenses, such as rent, utilities, and employee salaries, until you are able to resume normal operations.

For instance, if your business is unable to operate due to a natural disaster or vandalism, business interruption insurance helps mitigate the financial impact of those disruptions, ensuring that your business can continue to pay bills and employees.

4. Optional Coverages (Add-ons)

While a Business Owners Policy includes the essential coverages, you can often add more coverage based on your business’s needs. Some optional add-ons include:

- Cyber Liability Insurance: Protects against data breaches, cyberattacks, and other online risks.

- Workers’ Compensation Insurance: Covers medical expenses and lost wages for employees injured on the job.

- Commercial Auto Insurance: Provides coverage for vehicles used for business purposes.

- Employee Dishonesty Insurance: Protects against losses due to employee theft or fraud.

5. Equipment Breakdown Insurance

If your business relies on expensive machinery or equipment, equipment breakdown insurance can help cover the repair or replacement costs if a piece of equipment malfunctions. This is particularly important for manufacturing businesses, restaurants, or any business that depends on machinery for day-to-day operations.

How Much Does a Business Owners Policy Cost?

The cost of a Business Owners Policy varies depending on several factors, such as:

- Business Size and Location: Larger businesses with higher revenues or those located in high-risk areas typically pay higher premiums.

- Industry: High-risk industries, such as construction or food service, may have higher BOP premiums due to the nature of the work.

- Coverage Limits: The more coverage you need, the higher your premium. However, you can adjust coverage limits to match your business’s budget and risk tolerance.

- Claims History: If your business has a history of claims, your premium may increase. On the other hand, businesses with a clean claims history may receive discounts.

On average, a Business Owners Policy can cost anywhere from $500 to $3,000 per year, depending on the factors mentioned above. However, when you compare this to the potential costs of an uninsured claim, BOP coverage is an affordable investment for business protection.

How to Choose the Right Business Owners Policy for Your Business

Choosing the right Business Owners Policy depends on your business’s specific needs and risks. Here are some tips to help you select the right BOP:

- Assess Your Risks: Understand the risks your business faces, such as property damage, liability claims, and business interruption. This will help you determine the coverage you need.

- Shop Around: Get quotes from multiple insurers to compare premiums, coverage options, and customer service ratings. Work with an agent who understands your business and can recommend the right policy.

- Review Your Policy Annually: Your business’s needs may change over time, so it’s important to review your policy each year to ensure you’re still adequately covered.

Frequently Asked Questions (FAQs)

1. What’s the difference between a BOP and general liability insurance?

While general liability insurance protects against liability claims, a Business Owners Policy includes general liability insurance along with other coverages, such as property insurance and business interruption insurance, in one convenient package.

2. Can a business qualify for a BOP?

A BOP is typically available to small and medium-sized businesses that meet certain criteria. To qualify, your business usually needs to be in a low to moderate-risk industry, have a small number of employees, and generate a manageable amount of revenue.

3. Does a BOP cover employee injuries?

No, a Business Owners Policy does not typically cover employee injuries. To cover employees, you’ll need workers’ compensation insurance, which can be added to your BOP or purchased separately.

4. Is business interruption insurance included in a BOP?

Yes, most Business Owners Policies include business interruption insurance, which helps cover lost income if your business is temporarily shut down due to a covered event.

Conclusion

A Business Owners Policy (BOP) is an invaluable insurance solution for small to medium-sized businesses, offering essential protection against property damage, liability claims, and business interruption. By bundling multiple types of coverage into one affordable policy, a BOP can help safeguard your business from unexpected events, reduce financial risks, and provide peace of mind.

When selecting a BOP, make sure to assess your business’s unique needs and risks, and consult with an insurance expert to customize a policy that works for you. With the right coverage, you can focus on growing your business without constantly worrying about the unknown.