Blockchain in Insurance: Transforming the Industry with Innovation

The insurance industry, traditionally known for its conservative approach, is undergoing a revolution thanks to blockchain technology. By enhancing transparency, reducing fraud, and streamlining claims processing, blockchain has the potential to address longstanding inefficiencies and build trust between insurers and policyholders.

In this article, we’ll explore how blockchain is reshaping the insurance landscape, including its applications, benefits, challenges, and real-world examples of its use.

What is Blockchain Technology?

At its core, blockchain is a distributed ledger technology that records transactions in a secure, transparent, and immutable manner. Unlike centralized systems, blockchain operates on a decentralized network, ensuring that all participants have access to the same verified information.

Did you know? Blockchain reduces administrative costs in insurance by up to 30%, offering significant savings for insurers.

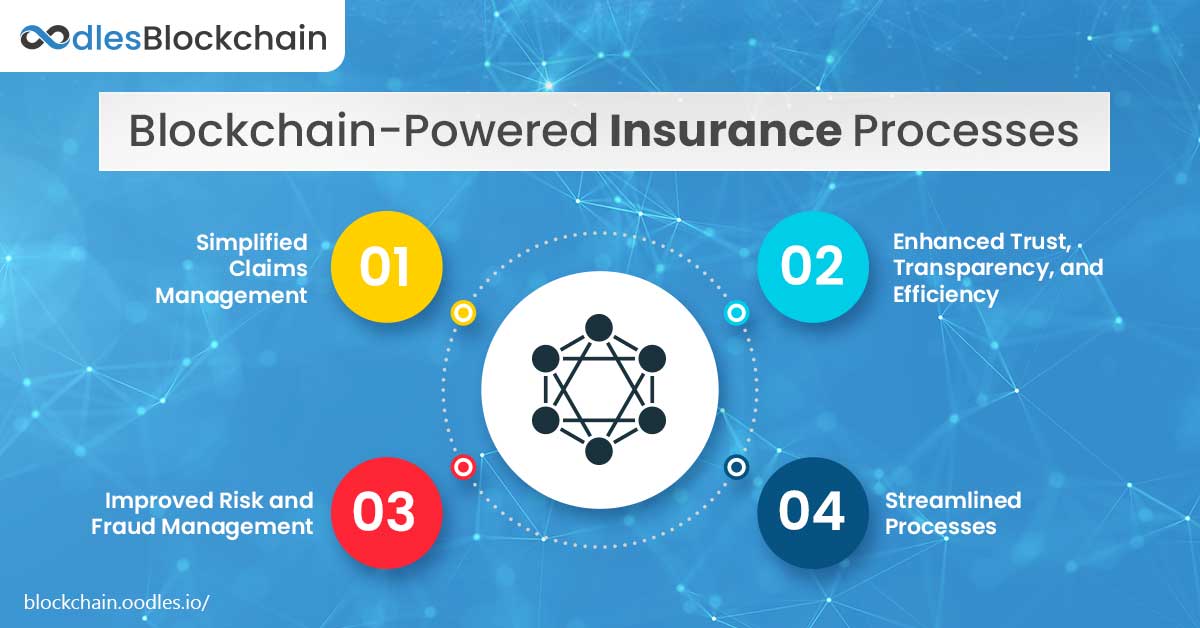

Why Blockchain Matters in Insurance

The insurance sector faces numerous challenges, including fraud, lengthy claims processing, and lack of transparency. Blockchain technology offers solutions to these problems by:

- Enhancing Transparency:

Blockchain’s decentralized ledger allows all stakeholders to access real-time, verified data, minimizing disputes. -

Reducing Fraud:

Blockchain creates an immutable record of transactions, making it easier to detect and prevent fraudulent claims. -

Improving Efficiency:

Automating processes such as policy issuance and claims verification reduces administrative costs and processing times. -

Increasing Trust:

With its transparent nature, blockchain builds confidence among customers and insurers, fostering stronger relationships.

Applications of Blockchain in Insurance

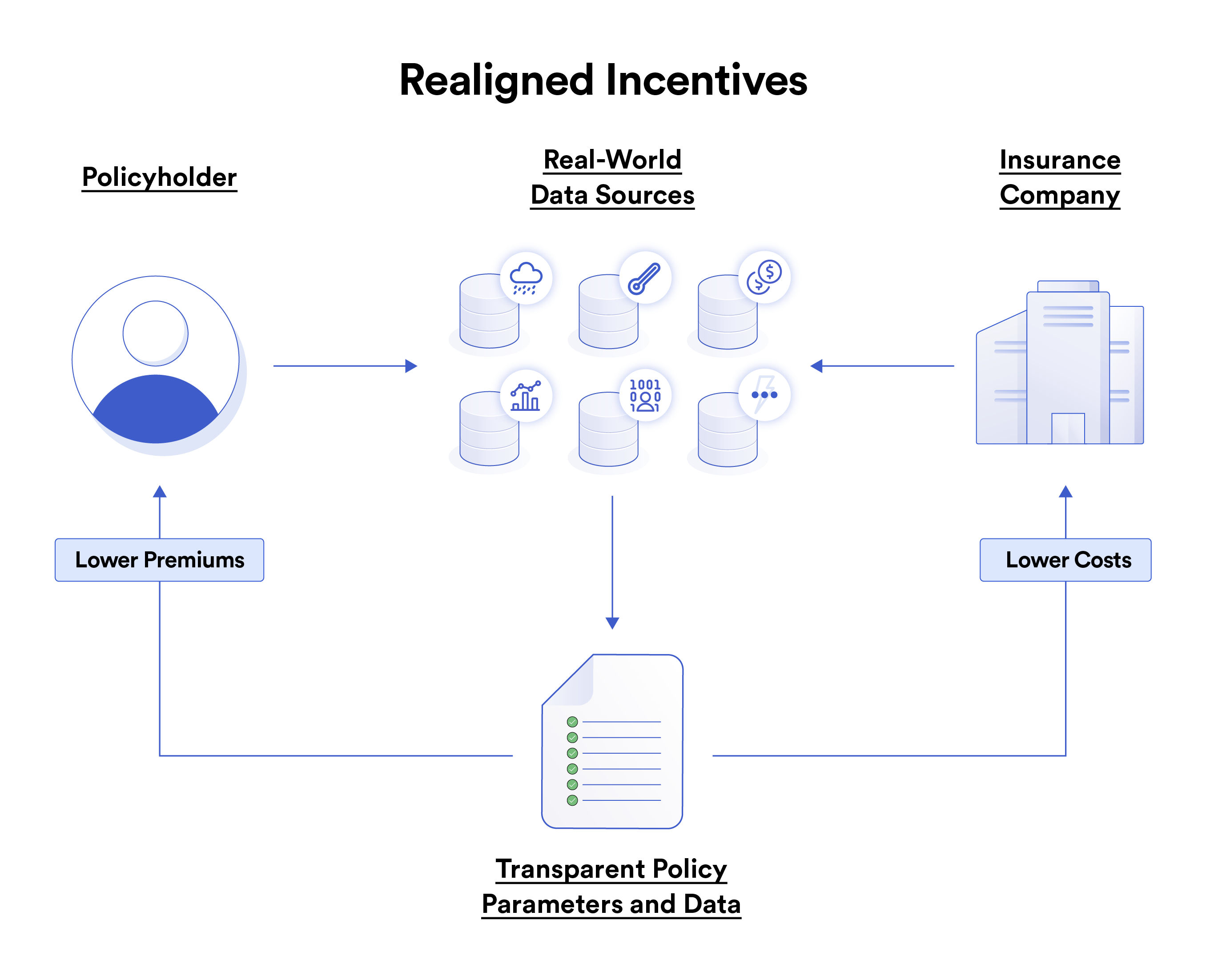

1. Smart Contracts for Claims Automation

One of the most significant innovations brought by blockchain is smart contracts. These self-executing contracts automate claims processing based on predefined conditions.

- Example:

In travel insurance, a smart contract can automatically trigger a payout if a flight is delayed, as verified by external data sources (oracles).

Benefits:

– Faster claim settlements.

– Reduced human intervention.

– Enhanced customer satisfaction.

Learn more about smart contracts and their role in transforming industries in this guide on blockchain applications.

2. Fraud Detection and Prevention

Insurance fraud costs the industry billions annually. Blockchain combats this by maintaining a tamper-proof record of claims and transactions.

- How it works:

Shared ledgers allow insurers to cross-check data and identify duplicate or suspicious claims.

Real-world Example:

The Blockchain Insurance Industry Initiative (B3i) is a global consortium using blockchain to combat fraud and enhance risk management.

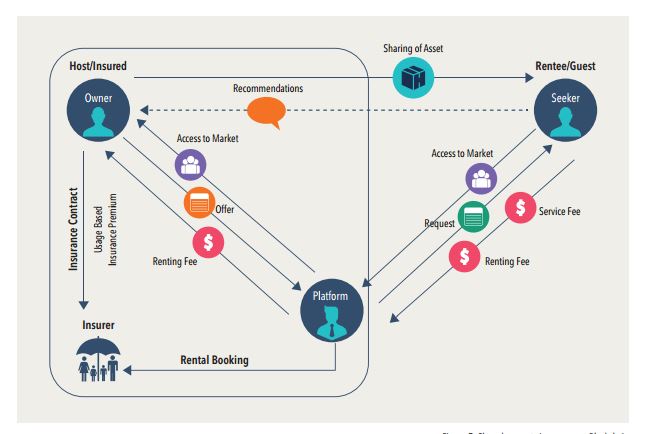

3. Peer-to-Peer (P2P) Insurance

Blockchain enables P2P insurance, where individuals pool resources to cover risks without relying on traditional insurers.

- Advantages:

- Lower premiums.

- Greater control for policyholders.

- Transparency in fund allocation.

This innovative model is gaining traction in areas like healthcare and property insurance, thanks to its community-driven approach.

4. Blockchain for Reinsurance

Reinsurance, the process of insurers transferring risk to other companies, is often complex and time-consuming. Blockchain simplifies this by creating a shared, real-time ledger for all parties involved.

- Key Benefits:

- Faster data exchange.

- Reduced administrative overheads.

- Enhanced risk assessment accuracy.

Example:

Aon and IBM have partnered to develop blockchain solutions for reinsurance contracts, making them more efficient and transparent.

Benefits of Blockchain in Insurance

- Cost Reduction

- Blockchain reduces overheads associated with claims processing, underwriting, and fraud management.

- Improved Customer Experience

- Faster settlements and increased transparency result in higher customer satisfaction.

- Data Security

- Blockchain’s encryption protocols protect sensitive customer information from cyber threats.

- Enhanced Collaboration

- Insurers, brokers, and regulators can share data seamlessly, fostering better coordination.

Challenges of Implementing Blockchain in Insurance

Despite its potential, adopting blockchain in insurance comes with challenges:

- High Initial Costs:

Developing and deploying blockchain systems require significant investment. -

Regulatory Hurdles:

Different jurisdictions have varying regulations, making it difficult to implement blockchain globally. -

Integration with Legacy Systems:

Insurers must integrate blockchain with their existing IT infrastructure, which can be complex. -

Scalability Issues:

As the volume of transactions grows, maintaining blockchain’s efficiency can become a challenge.

Solution:

Collaborative efforts between insurers, tech providers, and regulators are crucial to overcoming these challenges.

Real-World Examples

1. Etherisc

A blockchain-based platform offering parametric insurance products, including crop insurance for farmers.

2. AXA’s Fizzy

AXA’s Fizzy platform uses blockchain to provide automated travel insurance, issuing instant payouts for flight delays.

3. Lemonade

A digital insurance company leveraging blockchain for transparency and efficient claims processing.

FAQs

1. What is blockchain’s role in insurance?

Blockchain enhances transparency, efficiency, and security in insurance operations, enabling automated processes and reducing fraud.

2. Are there risks in adopting blockchain in insurance?

While blockchain offers numerous benefits, challenges like high costs and regulatory uncertainty must be addressed for widespread adoption.

3. How does blockchain improve customer experience?

By enabling faster claims processing and offering transparent operations, blockchain significantly enhances customer satisfaction.

Conclusion

Blockchain is no longer a futuristic concept but a practical tool that is revolutionizing the insurance industry. From streamlining claims processing to enhancing fraud prevention, its applications are reshaping traditional practices and paving the way for a more efficient, transparent, and customer-centric insurance ecosystem.

As blockchain adoption grows, insurers who embrace this technology early will have a competitive edge, setting new standards in innovation and customer trust.

For more insights on how blockchain is transforming industries, visit Blockchain Technology Trends.

End of Article