Peer-to-Peer Insurance: Revolutionizing the Insurance Industry

Peer-to-peer insurance (P2P insurance) is redefining the traditional insurance landscape by emphasizing collaboration, transparency, and shared risk. With its potential to enhance efficiency and reduce costs, it’s no wonder this innovative model is gaining traction globally. But what exactly is P2P insurance, and why is it poised to become a game-changer?

What is Peer-to-Peer Insurance?

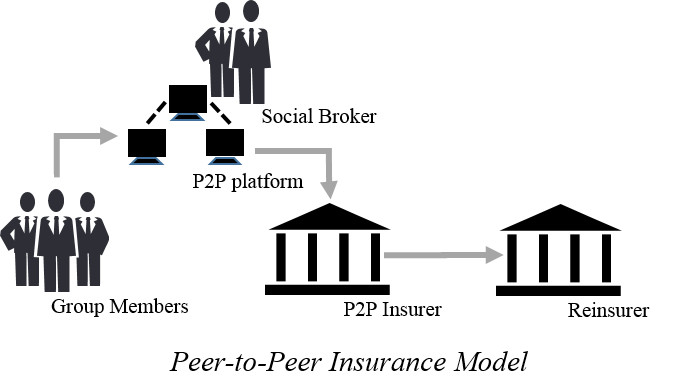

At its core, peer-to-peer insurance involves pooling resources among a group of individuals to insure against shared risks. Unlike traditional insurance, which relies on large corporations to underwrite policies, P2P insurance creates a network of like-minded people who contribute premiums into a shared pool. When a claim arises, the funds are drawn from this pool to compensate the policyholder.

This system minimizes the reliance on intermediaries, potentially reducing costs and ensuring that unused premiums benefit the group instead of generating corporate profit.

How Peer-to-Peer Insurance Works

The mechanics of P2P insurance are relatively simple:

- Formation of Groups: Policyholders join a group with shared interests or risk profiles.

- Pooling of Funds: Members contribute premiums to a communal fund.

- Claim Resolution: When a claim arises, it is assessed and, if valid, paid out from the group’s pool.

- Refund or Reallocation: At the end of a policy term, any unused funds may be refunded or rolled over.

“Think of it as a digital version of an age-old concept: communities helping each other in times of need.”

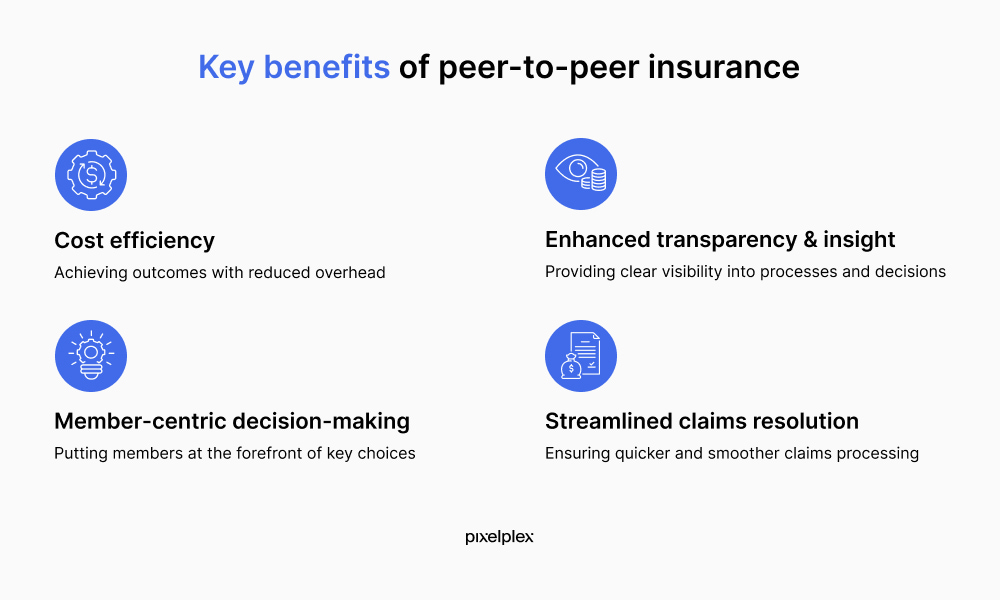

Key Benefits of Peer-to-Peer Insurance

1. Lower Costs

Traditional insurance often involves high administrative costs, commissions, and profit margins. P2P insurance eliminates many of these overheads, making it a more cost-effective option for policyholders.

2. Increased Transparency

P2P models leverage blockchain technology and digital platforms to provide real-time tracking of contributions and claims, ensuring greater trust and transparency.

3. Reduced Fraud

Because funds belong to a peer group, there is a natural deterrent against fraudulent claims, as they directly impact the group’s resources.

4. Shared Rewards

Unused premiums are often redistributed among members, creating a tangible incentive for responsible behavior.

5. Personalized Coverage

P2P insurance allows for more customized policies, tailored to the specific needs of niche groups or communities.

Challenges Facing Peer-to-Peer Insurance

While the benefits are significant, P2P insurance also faces hurdles:

- Regulatory Compliance: Varying laws across jurisdictions can make it challenging to scale operations.

- Risk of Insolvency: Smaller pools may struggle to cover catastrophic losses.

- Adoption Barrier: Educating consumers about this new model and gaining their trust requires effort.

Nonetheless, with advancements in technology and growing consumer demand, these challenges are surmountable.

Peer-to-Peer Insurance in Action

Several companies are pioneering the P2P insurance space:

1. Lemonade

Lemonade operates on a peer-to-peer insurance model, using AI to streamline processes and donating unclaimed premiums to charity.

2. Friendsurance

A German company that connects small groups of people to share deductibles and reduce individual insurance costs.

3. Teambrella

A blockchain-based platform allowing users to form teams and manage claims democratically.

Why the Future Looks Bright for Peer-to-Peer Insurance

The digital transformation of the insurance sector, coupled with the rise of collaborative consumption, positions P2P insurance as a sustainable and innovative solution. Its alignment with consumer preferences for transparency, personalization, and cost-efficiency makes it a formidable competitor to traditional models.

Industry Trends Driving Growth

- Increased Smartphone Penetration

Digital platforms are the backbone of P2P insurance, and widespread smartphone usage facilitates seamless participation. -

Blockchain Integration

Blockchain ensures secure, transparent transactions and records, reducing disputes. -

Demand for Fairness

Consumers are increasingly questioning the ethics of traditional insurers, driving interest in alternatives like P2P insurance.

How to Get Started with Peer-to-Peer Insurance

- Identify Your Needs: Assess your coverage requirements.

- Research Providers: Look for reputable P2P platforms with strong reviews.

- Read the Terms: Understand how funds are managed, claims processed, and refunds handled.

- Join a Group: Choose a pool that aligns with your risk profile and values.

FAQs About Peer-to-Peer Insurance

1. Is P2P insurance safe?

Yes, provided you choose a reputable provider with adequate risk management mechanisms.

2. How does it differ from traditional insurance?

P2P insurance eliminates intermediaries and redistributes unused premiums, offering a more transparent and cost-effective model.

3. Can P2P insurance cover all types of risks?

While it’s versatile, some risks (like large-scale disasters) may still require traditional reinsurance support.

Conclusion

Peer-to-peer insurance represents a paradigm shift in the insurance industry. By fostering collaboration, transparency, and fairness, it addresses many of the inefficiencies of traditional models. As technology continues to evolve, the adoption of P2P insurance is likely to accelerate, offering individuals and businesses an affordable, ethical, and innovative solution to managing risk.

Whether you’re tired of the complexities of conventional insurance or simply looking for a more community-driven approach, P2P insurance is a trend worth exploring.